VantagePoint: Artificial Intelligence Investing After the First Wave

A year ago, in our three-part series Navigating the AI Revolution, the central question for investors was where artificial intelligence’s (AI’s) disruptive potential would translate into meaningful economic and market change. That question now has a clearer answer. AI is already reshaping parts of the economy and market as capabilities improve rapidly, enterprise adoption broadens, and revenue growth becomes more visible across the ecosystem. Disruption is no longer a distant possibility. It is beginning to show up in software and labor-intensive functions such as customer service.

The investment question has changed with it. The first phase of AI investing was led by hyperscalers, advanced semiconductors, and large language model developers. The current phase has been driven by infrastructure buildout, and markets have already recognized much of that trade. Over the next few years, we expect the most attractive opportunities to center on more persistent bottlenecks, particularly around power, and on companies that control workflow, own the customer relationship, bring domain expertise, and turn AI output into business action. That includes the software infrastructure and applications that will shape how AI is deployed and managed. As companies integrate AI into workflows, adopters across industries should benefit. We expect much of the next phase of value creation to come from emerging AI-native companies and disruptive business models, though at this early stage, even today’s disruptors may be displaced.

In this edition of VantagePoint, we focus on three questions:

- Which bottlenecks are durable?

- Can rising revenues justify the capital required to sustain leadership?

- Where can value persist as AI becomes cheaper, more capable, and more widely available?

The broader consequences for labor and society may prove profound, but they remain harder to observe clearly and are progressing slower than the technology itself. Regulation and sovereignty risk considerations clearly matter, as does society’s willingness to absorb the pace of change and its consequences. Those forces will shape AI’s development, but they are not the focus of this paper. We focus instead on where the evidence is strongest today and where the investment implications are becoming harder to ignore.

Tech is still early, moving fast

AI capabilities continue to improve at breakneck speed. The leading labs remain in a tight race, and each major release raises the bar while increasing disruption risk for incumbents and start-ups alike. Leadership among US models continues to oscillate. Chinese models have narrowed the gap on several technical measures despite US export controls on advanced chips. The open-model ecosystem, much of it coming from China, has also become a credible lower-cost option for use cases outside of mission-critical workflows that still demand premium US tools.

Frontier intelligence is becoming more capable, more available, and less exclusive. That should expand adoption, but it also makes raw model access a less reliable source of durable advantage and shifts value toward the assets and capabilities that make intelligence useful, governable, and hard to replace.

AI is shifting from a tool that generates responses to a tool that performs useful work. Recent model releases have improved reasoning, reliability, memory, and the ability to work across different types of data. Anthropic’s AI model, Claude, helped accelerate the move from coding assistant to autonomous coding agent through Claude Code, then extended that logic into broader knowledge work. While this is a major disruptive theme and a central focus of this paper, it is only one part of a broader transformation. Specialist models in mathematics, biology, and other fields are proliferating, while researchers continue to experiment with non-transformer architectures such as world models designed for physical AI. Smaller models are improving as well, pushing more inference to run on local systems instead of keeping them entirely in centralized cloud environments.

These advances are beginning to make disruption more visible. In software, faster model improvement is compressing product cycles, narrowing functional differentiation, and pressuring application-level moats that once appeared durable. In labor-intensive workflows such as customer service, the effects are already showing up in shorter handle times, lower staffing needs, and greater pressure to automate routine work. Much of the broader disruption still lies ahead, but the direction is clearer.

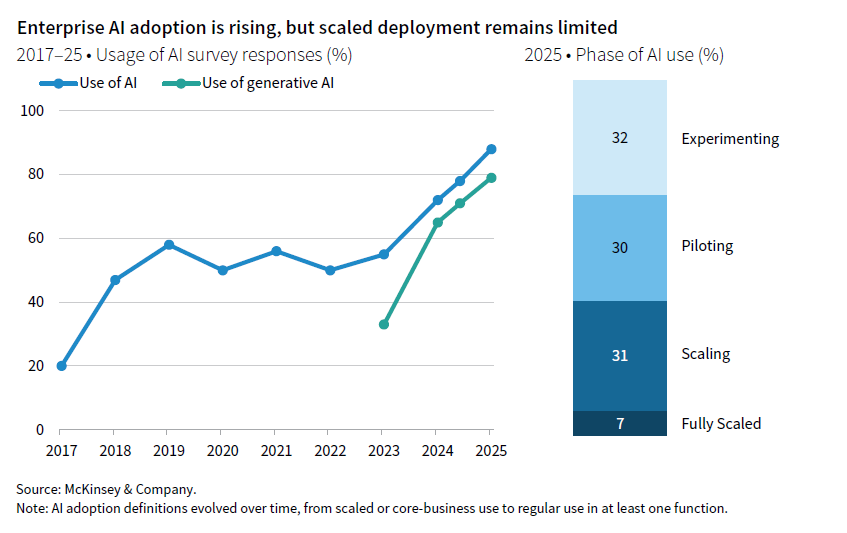

Enterprise AI adoption is rising, but scaled deployment remains limited

The pace of enterprise adoption is becoming increasingly apparent, even if scaled deployment remains limited and difficult to track in real time. McKinsey survey data captures the key point for investors: adoption is rising, but much of it still reflects experimentation, piloting, and limited deployment rather than full integration across core workflows.

Coding remains the clearest use case, though productivity gains are still early and uneven. Deployment inside real organizations will be challenging, requiring integration, oversight, and governance as much as good model performance. Usage will evolve as service models change. For example, firms are still enjoying subsidized model pricing, internal controls are weak, and many firms are still learning to use these tools effectively while keeping token costs under control.

As AI advances rapidly, the need for stronger corporate governance is becoming more urgent, even if progress is moving at a more human pace. Some early adopters are pulling ahead in part because they addressed governance, access controls, and oversight sooner, making scaled deployment in sensitive workflows easier. Others may appear to be moving faster precisely because they are deferring those disciplines and accumulating a governance backlog that has not yet surfaced in operating results. Recent events also show how quickly regulatory and security concerns can affect commercialization. Anthropic’s temporary withdrawal of Fable 5 and Mythos 5 following a US government directive serves as a reminder that deployment risk may increasingly hinge on security, liability, and policy judgments. Public backlash is also growing, which could make regulation more political over time. As AI use broadens, questions of data provenance, auditability, security, and liability are likely to matter even more.

This shift from experimentation to scaled use is changing the investment question. Technical progress and broader adoption are making AI more commercially relevant, but they do not by themselves determine where durable returns will accrue. That depends increasingly on the economics of deployment and on which firms can turn AI capability into repeatable business action.

How AI economics are evolving

In our last edition of VantagePoint: The Rearview Mirror Problem, we argued that investors often mistake recent winners for future return drivers. That risk is especially acute in AI. The first-wave beneficiaries are well known, and the infrastructure buildout has become the market’s central focus. The harder question now is how the economics are evolving beneath that narrative, and which parts of the opportunity set can still deliver durable returns. We think investors should focus on three underwriting questions: Which bottlenecks are durable? Can rising revenues justify the capital required to sustain leadership? Where can value persist as AI becomes cheaper, more capable, and more widely available?

The economics are changing along with the technology. Constraints have shifted from training toward inference, usage, and deployment, and value capture is broadening with them. The relevant opportunity set now extends beyond frontier-training hardware to a broader mix of inference and data infrastructure, deployment software, workflow and permission layers, governance tools, and applications that shape how AI is embedded in business processes.

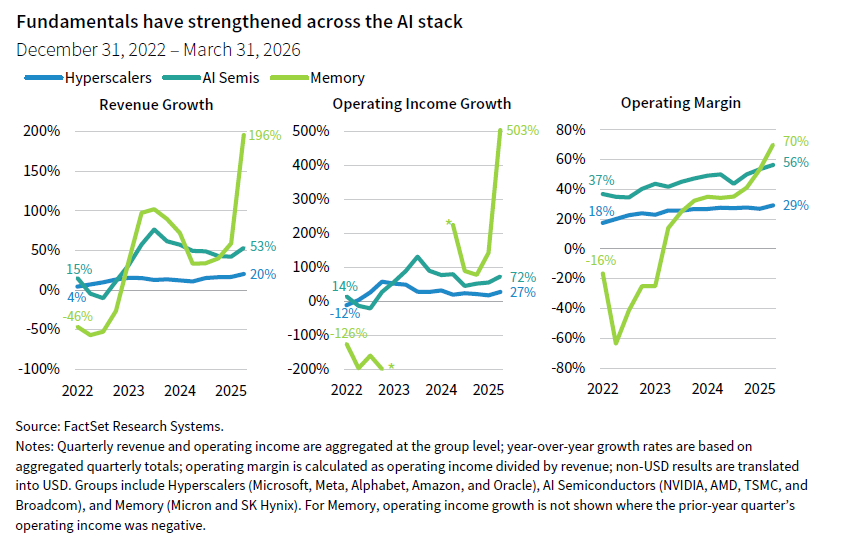

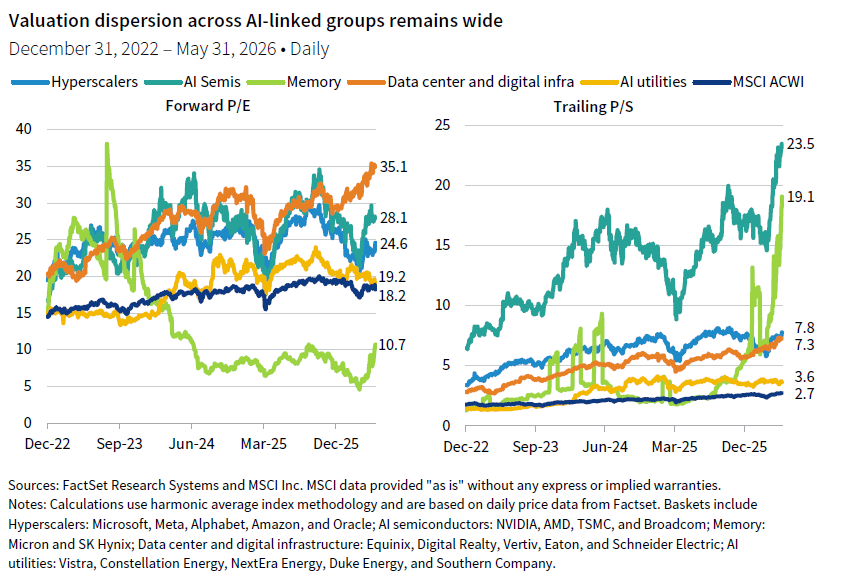

Earnings have begun to catch up with enthusiasm in parts of the AI ecosystem. Recent gains in AI-linked equities no longer rest on expectations alone. Several leading firms have reported strong revenue growth tied to AI demand, especially in semiconductors, cloud, and selected infrastructure segments. Private model providers, such as Anthropic, appear to be seeing similar momentum, though their economics remain less transparent. Stronger fundamentals validate part of the move. They do not settle the harder question of whether revenue growth will prove durable enough to justify the operating and capital costs required to sustain it.

Which bottlenecks are durable?

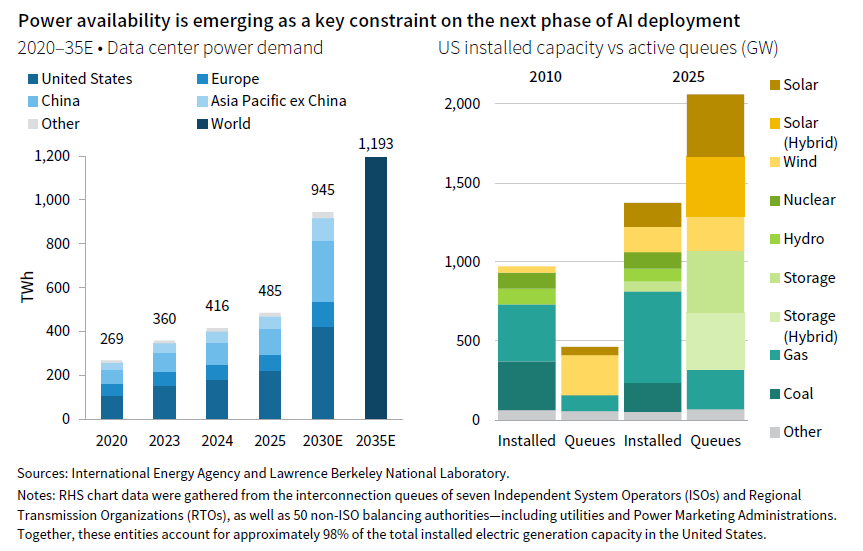

This first question deals with whether bottlenecks are persistent or simply reflect temporary undersupply. Early in the cycle, scarcity centered on training compute and raw GPU capacity. That is no longer the full story. As AI deployment scales, the tighter constraints are becoming more physical. Data center infrastructure, memory, and advanced packaging remain important, but power is emerging as the clearest hurdle. Reliable electricity, cooling, transmission, and the ability to bring new capacity online increasingly matter as much as access to chips. 1

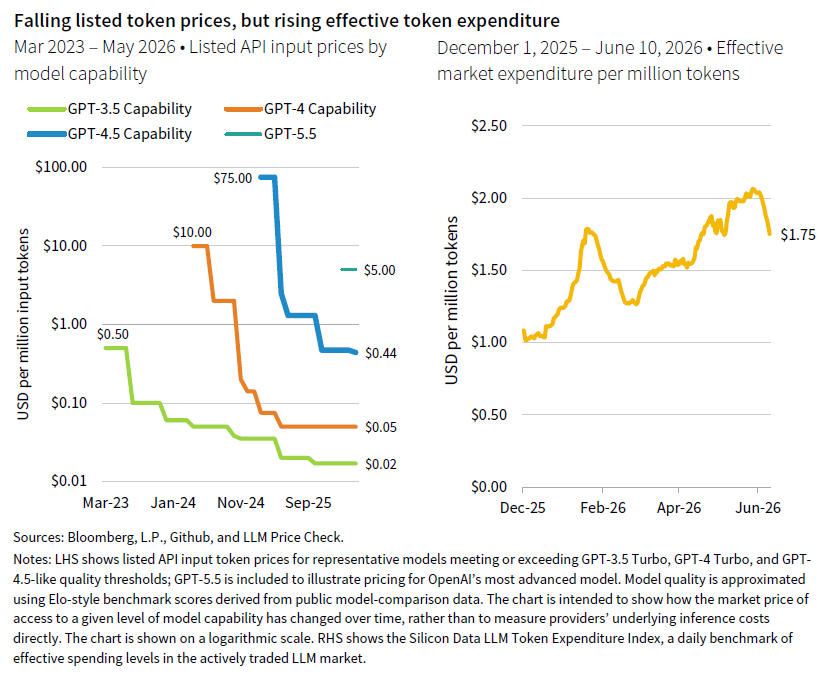

Falling prices in one layer of the stack do not remove constraints in another. Listed token prices have fallen sharply, which should broaden adoption. But lower prices do not mean lower compute demand. As models have become more capable and AI systems take on more complex tasks, the compute required to complete useful work has continued to rise. More autonomous and always-on systems will reinforce that trend by increasing token consumption and placing greater strain on the physical stack.

Power deserves particular attention because it is increasingly one of the hardest constraints to relieve. Utilities, grid equipment, cooling, and related enabling infrastructure can be difficult to replicate quickly because they depend on permitting, transmission access, engineering capacity, and time to build. Those are more durable barriers than the temporary scarcity that can emerge in parts of the hardware stack early in a buildout.

Memory and advanced packaging also remain important choke points, supporting stronger pricing and earnings across parts of the semiconductor ecosystem. The key investment question, however, is not whether these areas are constrained today, but whether those rents are likely to persist. Some supply bottlenecks may prove temporary as capacity expands. Others may reflect capabilities that are harder to replicate quickly.

In some parts of the market, security, compliance, and regulatory approval may also function as bottlenecks. Where customers need trusted systems for sensitive workflows, firms that can meet higher standards for resilience, auditability, and control may accrue durable advantage.

Not every bottleneck supports durable economics. Some stem from short-lived pricing power. Others are tied to assets, regulation, siting, expertise, or customer relationships that are harder to reproduce. Open and lower-cost models reinforce that point. They may broaden adoption and accelerate experimentation, but they also challenge the idea that frontier capabilities alone guarantee durable pricing power. In areas where customers do not require frontier performance or tightly integrated proprietary systems, improving open models are compressing economics at both the model and software layer.

Can rising revenues justify the capital required to sustain leadership?

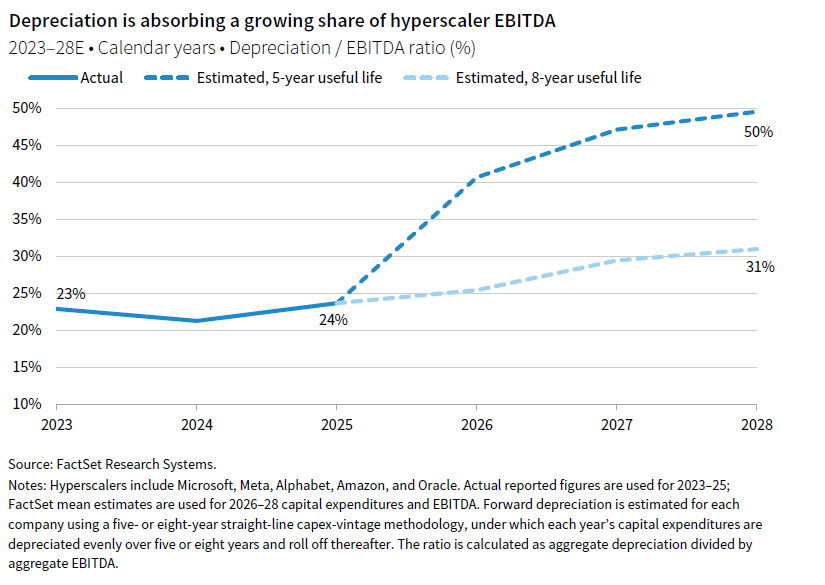

The second question asks whether rising revenues and earnings can justify the capital required to sustain AI leadership. That issue is now most visible in the capex cycle. For current spending to earn attractive returns, revenue growth must continue to catch up with investment, usage must remain high, enterprise monetization must deepen, and margins must hold up despite a much larger capital base.

Consensus expectations for the five major hyperscalers call for combined revenue to increase 54% while EBITDA is expected to increase about 111% from year-end 2025 through 2028. Over the same period, depreciation is expected to rise much faster. Depending on assumed asset lives, it could increase by roughly 175% to more than 340%. That drag is large enough to matter. At the low end of those estimates, 2028 depreciation would come close to the group’s 2025 net income of $405 billion.

AI is making important parts of technology more capital intensive. Some parts of the market may still be valued as if AI were reinforcing capital-light software economics, when in fact it is making important parts of the stack more asset-heavy and operationally demanding. Investors should place more weight on depreciation, reinvestment needs, financing conditions, and the durability of pricing power on these more asset-heavy companies.

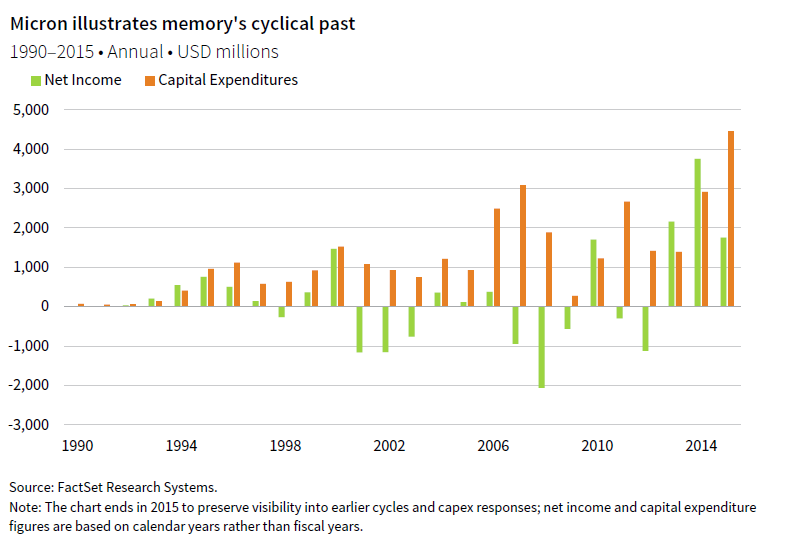

Memory is not a direct analogue for hyperscalers, and the current AI cycle has different drivers. Still, its history is a useful reminder that periods of tight supply, strong pricing, and high margins can look more durable than they prove to be once capacity expands. Shortages have repeatedly lifted margins and encouraged new investment, only to erode those same margins as supply caught up. AI may not follow that path exactly, but the lesson is familiar. Strong demand does not by itself protect returns when supply can respond and pricing power is not well defended.

Indeed, Micron and SK Hynix—two of the memory companies most directly exposed to advanced AI demand—have increased capex by a combined 70% in each of the last two years, and consensus expects another roughly 55% increase in 2026. Investors should be careful not to assume that today’s strong pricing and profitability will persist unchanged as capital spending rises and supply responds.

The quality of demand matters as well. Investors should distinguish between durable end demand and demand supported by ecosystem-linked commercial arrangements, strategic subsidy, or circular deal structures that make near-term economics look stronger than they are. As the system matures, leverage and structured financing also deserve more attention. Risk rises when capital assumptions become aggressive ahead of proven cash flows. After rising by roughly $900 billion since the start of this year, gross supply of investment-grade credit is expected to increase by about 17% over the full year to a record $2.1 trillion, with much of the increase coming from hyperscalers and related infrastructure. Structured credit markets are expected to see data center securitizations rise by nearly 50% in 2026 to $30 billion.

Stronger fundamentals have made the buildout more credible, but not necessarily more durable. High depreciation expense creates a demanding hurdle for hyperscalers that are increasingly competing with one another for business. Capital-intensive businesses facing rising competition may struggle even if the addressable market continues to grow. Not all participants will fare well. Semiconductors and advanced memory should benefit from tight supply and, in some cases, multi-year contracts, but supply is likely to catch up over time as capacity expands and technology becomes more efficient. Investors should be cautious about extrapolating today’s pricing and profitability too far into the future.

Where can value persist as AI becomes cheaper, more capable, and more widely available?

The final question considers where durable value can persist. Access to models alone will not remain enough. As intelligence diffuses, we expect more defensible positions to belong to firms that control how it is used: who owns the workflow, governs permissions, controls distribution, and connects output to execution. Hyperscalers and other large platforms are trying to capture value across multiple layers of the stack through vertical integration, from compute and cloud infrastructure to model access, routing, deployment, and enterprise tooling.

The most important shift is in what software and adjacent systems actually do. As agentic systems begin to perform economically meaningful work rather than simply assist users, part of the addressable market shifts from software budgets to labor budgets, which are much larger. That may expand revenue pools, deepen integration, and create stronger business models. It may also intensify disruption across software, services, and selected consumer sectors.

Software and adjacent control layers may still be where much of the value ultimately accrues, but they also pose the hardest underwriting questions. AI may expand revenue pools even as it weakens traditional moats. Customers may expect broader functionality without proportional price increases, while model, compute, orchestration, and support costs remain material. We expect the stronger positions belong to firms that are deeply embedded in a workflow, possess privileged task-specific context, and can convert AI output into completed work rather than simply sell access to a feature.

That distinction matters because control over the workflow is different from access to the model. A firm that helps generate an answer may be easy to displace. In an agent-driven environment, durable advantage should rest increasingly on control over permissions, approvals, and execution rather than on data alone. Systems that determine what autonomous software can access, trigger, and complete could have a competitive upper hand over systems of record alone.

This logic extends beyond enterprise software. In consumer markets, such as commerce, education, and travel, AI is likely to reshape discovery, service, and execution. New products and business models should emerge. But these same layers may also face the greatest pressure from improving models and larger platforms, especially where functionality is easy to replicate, customer relationships are weak, or distribution is controlled by someone else.

The same logic also shapes investment underwriting. Strong adoption and fast top-line growth may not be enough if a company with limited bargaining powers depends heavily on a single model provider, hyperscaler, or distribution platform. Downstream growth may prove real without translating into durable economics. Strategic acquisition may become a common end state for promising firms, supporting investment outcomes alongside a select group of independent long-duration compounders. For private equity and venture investors, underwriting should place more weight on customer ownership, monetization after model and compute costs, governance quality, likely end states, and the durability of economics if acquisition interest fades.

Investment implications

AI should be treated as a system-wide set of exposures rather than a narrow thematic trade. We see the stronger opportunities ahead in harder-to-relieve bottlenecks—especially power and related infrastructure—alongside the software and application layers that govern deployment in real workflows and emerging AI-native businesses that can reshape industry economics. The same shift should benefit adopters that use AI to improve their own economics while increasing disruption risk for incumbents that fail to adapt or are displaced by new business models.

This shift argues for more caution toward parts of the AI ecosystem where expectations, capital spending, and competition have all risen sharply at once. Large hyperscalers remain central to the buildout and may continue to benefit from scale, distribution, and enterprise integration. But they are also engaged in an increasingly costly race to secure compute, power, and physical infrastructure, and the associated depreciation burden is becoming harder to ignore. We therefore lean away from the most crowded first-wave winners, particularly where valuations still leave limited room for disappointment. The same caution applies to parts of semiconductors and memory, where recent earnings strength has been real, but history suggests investors should be careful not to mistake tight supply and current pricing power for durable advantage.

By contrast, we are more constructive on select infrastructure and real assets tied to harder-to-relieve constraints, particularly electricity infrastructure, grid access, and related enabling assets. These areas appear better positioned to benefit as AI deployment scales and physical bottlenecks become more binding.

The widening opportunity set also creates room for emerging disruptors, many of which were inconceivable before recent AI advances. As AI becomes cheaper, more capable, and more widely available, value will migrate toward firms that control workflows, permissions, customer relationships, and operational integration rather than those relying on thin wrappers or temporary model arbitrage. In software, the more durable positions are likely to belong to companies that can embed AI into economically meaningful tasks, govern it effectively, and monetize completed work rather than simple access. Private equity may benefit where businesses need capital, operational support, and technology investment to adapt successfully to AI-driven changes in cost structure and competition.

Venture capital remains the key channel for accessing emerging AI-native companies and disruptive business models, and investors seeking that upside likely need some participation in private markets. But this technology cycle is still early and, as in past cycles, a few winners are likely to emerge alongside many losers as innovation advances faster than commercial adoption. In that environment, exposure to AI is not the same as access to strong investment returns. Because private commitments are long-lived, pacing matters as much as manager selection. Investors should continue to allocate selectively, with discipline on timing and valuation rather than rushing to add exposure simply because the theme is compelling. As a new wave of highly anticipated technology IPOs comes to market this year, investors should be thoughtful about redeploying capital to venture capital, balancing those opportunities against other market segments with more attractive valuations and differentiated return potential.

The same framework should also be applied defensively. AI is not only a source of new opportunity. It is also a source of disruption risk in existing holdings. Businesses with weak differentiation, labor-intensive models, or information-heavy processes may be more vulnerable than they appear, even if they sit outside any obvious AI category. Equity long/short hedge funds may be well positioned to benefit from rising dispersion as AI creates clearer winners and losers across software, services, and other information-intensive industries. As disrupted companies—especially ones that took on private debt during the period of zero interest rates and high valuation from 2021 to early 2022—struggle to refinance over the next few years, stressed and distressed opportunities may emerge.

AI remains an important area of exposure. From here, we expect the best opportunities to come from identifying durable bottlenecks, defensible control points, and the businesses most likely to benefit from disruption rather than suffer from it. Active management across public and private markets will be central to success.

Graham Landrith and Justin Hopfer also contributed to this publication.

Index Disclosure

MSCI All Country World Index (ACWI)

The MSCI ACWI captures large- and mid-cap representation across 23 developed markets (DM) and 24 emerging markets (EM) countries. With 2,558 constituents, the index covers approximately 85% of the global investable equity opportunity set. DM countries include Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom, and the United States. EM countries include Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Kuwait, Malaysia, Mexico, Peru, the Philippines, Poland, Qatar, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey, and the United Arab Emirates.

Footnotes

Celia Dallas - Celia Dallas is the Chief Investment Strategist and a Partner at Cambridge Associates.

Katharine Campbell - Katharine Campbell is a Partner for the Endowment & Foundation Practice at Cambridge Associates.

Theresa Sorrentino Hajer - Theresa Hajer is Head of US Venture Capital Research and a Partner at Cambridge Associates.

About Cambridge Associates

Cambridge Associates is a global investment firm with 50+ years of institutional investing experience. The firm aims to help pension plans, endowments & foundations, healthcare systems, and private clients achieve their investment goals and maximize their impact on the world. Cambridge Associates delivers a range of services, including outsourced CIO, non-discretionary portfolio management, staff extension and alternative asset class mandates. Contact us today.