GRAT Expectations: Extra Opportunity in the Current Environment

Grantor retained annuity trusts (GRATs) have been a popular and effective wealth transfer strategy for US families in recent decades. This has been true across various market conditions, because their potential upside is so high and downside so low—and GRATs are even more compelling in the current market environment, due to low Treasury yields, potentially reduced valuations, and increased volatility. Yet despite their advantages, GRATs cannot achieve their full potential without careful analysis of multiple factors, including structuring and investment considerations. This paper summarizes the mechanics and treatment of GRATs, their heightened appeal right now, and the key tax, legal, and investment considerations to explore before implementing this strategy.

The Basics

GRATs aim to transfer wealth to the next generation during a donor’s lifetime free of gift tax consequences. A donor contributes assets to an irrevocable trust, which must have a fixed term and be funded entirely at inception, and then receives payments back from the trust over the fixed term. These payment amounts must be explicitly specified or otherwise ascertainable as of the GRAT’s inception, and they can either be constant throughout the GRAT term or increase by up to 20% each year.

At the end of the GRAT term, following the final payment back to the donor, any remaining trust assets pass to, or may continue in trust for, children or other non-charitable beneficiaries (the “remainder beneficiaries”).

Tax Treatment

For income tax purposes, the donor is treated as the owner of the GRAT under the “grantor trust” rules during the GRAT term (and possibly thereafter, if a continuing trust is incorporated). This means all the GRAT’s income, gain, deduction, and loss is treated as the donor’s, and the donor is liable for any tax otherwise attributable to the GRAT’s assets.

One benefit of grantor trust status is that the GRAT need not be depleted by taxes on its income and gains, leaving more assets passing to the remainder beneficiaries. Also, because the GRAT is indistinct from the donor for income tax purposes, transactions between the donor and the GRAT are not taxable events; therefore, the donor may substitute property in or out of the GRAT, so long as it has equal fair market value at the time.

For gift tax purposes, the gift to the remainder beneficiaries is determined (and potentially taxed) only at the inception of the GRAT, regardless of whatever assets and amounts ultimately pass to or in further trust for the remainder beneficiaries at the end of the GRAT term. 1 That aggregate present value of payments back to the donor is computed under a prescribed method using the so-called “Section 7520 rate” as the discount rate, which is favorable to a donor in two respects. First, the Section 7520 rate is typically lower than the expected returns on most risk assets. Second, the prescribed method allows for the gift tax value of the GRAT remainder interest to be “zeroed out” as described below, with no gift tax or use of gift tax exemption.

Opportunity Knocks

The Section 7520 rate is published monthly and is based solely on three- to nine-year Treasury yields multiplied by 120%. As noted above, this is the rate used to discount the value of payments back to the donor during the GRAT term, which in turn determines the gift tax value of the GRAT remainder interest—regardless of what assets are contributed to or held in the GRAT over time and regardless of what the GRAT’s expected or actual returns might be.

Where the actual return on GRAT assets exceeds the relevant Section 7520 rate on a dollar-weighted basis, the value of the assets remaining for beneficiaries at the end of the GRAT term will exceed what was assumed for gift tax purposes. So long as the donor survives to the end of the term, that excess will pass to the remainder beneficiaries free of any further gift tax or estate tax. 2 The value of the remainder interest for gift tax purposes is not revised retroactively.

Accordingly, one can think of the Section 7520 rate as a hurdle rate for success. Fortunately, across market conditions, most risk assets will have expected returns higher than the Section 7520 rate, even though actual returns might prove lower from time to time.

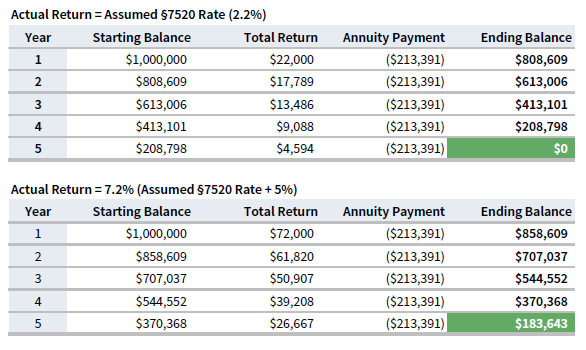

Even better, a GRAT remainder may be zeroed out and result in no gift tax or use of gift tax exemption. In other words, the specified payments back to the donor may be structured so that their aggregate present value (using the Section 7520 rate) equals the value of the property contributed to the GRAT, resulting in zero present value—and zero taxable gift—for the remainder interest. 3 Figure 1 illustrates these dynamics with the returns, annuity flows, and remainder amounts (highlighted in green) for a zeroed-out five-year GRAT funded with $1,000,000; one earns investment returns equal to an assumed Section 7520 rate of 2.2% (the approximate mean rate over the past ten years), and the other exceeds that hurdle rate by 5%.

FIGURE 1 GRATS WITH INVESTMENT RETURNS AT AND ABOVE SECTION 7520 RATE

Source: Cambridge Associates LLC.

If a GRAT is zeroed out but the realized rate of return in the GRAT falls short of the Section 7520 hurdle rate, the GRAT will simply exhaust itself through payments back to the donor at or before the end of the GRAT term. Nothing will be left for the remainder beneficiaries, yet no gift tax will have been paid nor any gift tax exemption wasted. The only costs in this scenario will be the relatively low transaction costs of establishing, reporting, and administering the GRAT and possibly the opportunity cost of not using other wealth transfer strategies instead of the GRAT.

Opportunity Knocks Harder in the Current Environment

The potential upside of a GRAT increases with the prospects of exceeding the Section 7520 hurdle rate. Thus, GRATs can be especially powerful when Section 7520 rates are lower or when expected returns are higher—or best of all, when both occur.

Current Section 7520 rates are at historic lows. In the 30+ years since the Section 7520 rate was introduced, its mean and median have both been approximately 5%. However, with the striking recent rally in Treasuries, the rate has reached all-time lows of just 0.8% for May 2020 and 0.6% for June and July 2020. These extraordinarily low rates improve the chances that a GRAT will succeed in transferring assets to remainder beneficiaries without gift tax consequences.

Moreover, since market downturns result in reduced valuations, they may afford more attractive entry points to achieve returns exceeding the Section 7520 hurdle rate, whether broadly or for specific assets or asset classes.

Higher volatility, like that occurring in the current environment, can provide greater opportunity as well, since the benefits versus costs of a GRAT’s success or failure are asymmetrical. Volatility can increase not just the potential outperformance in a successful GRAT, but also the ability to capture and retain that outperformance (as described in more detail below), or recover from any underperformance, before the GRAT term ends.

Implementation

This is an excellent time to consider GRATs but, as always, a number of considerations should be taken into account and discussed with one’s tax, legal, and investment advisors to ensure that the GRAT achieves its end goal most effectively for each individual donor.

Structuring Considerations

Payment Structures. Where fixed payments are required from a pool over a period of time, the front-end investment returns and payment amounts are most important in determining what is left (or even whether anything is left) at the end of that period. While payments from a GRAT may be constant over the GRAT term, it is also permissible for them to increase by up to 20% each year. This structure is generally preferable, at least from a tax and investment standpoint, because it reduces the payment amounts required in the early years to zero out the GRAT. This in turn reduces the risks that underperformance in early years will be crystallized with those early payments, such that the GRAT fails. It also allows greater compounding of any outperformance over the Section 7520 hurdle rate in those early years.

GRAT Term Length and Rolling GRATs. A longer GRAT term allows the donor to lock in a low Section 7520 hurdle rate for a longer period of time and enables the greater compounding of any returns exceeding the Section 7520 hurdle rate. However, a longer GRAT term also increases the mortality risk of the donor dying during that term, which will defeat the purpose of the GRAT.

Since the downside of a GRAT failing is relatively low, one common approach to the term-length dilemma is to use a series of rolling GRATs over time. For example, a donor could establish one or more two-year GRATs, and the annual payments (each being slightly more than 50% of the initial funding amount) could then be recycled into new two-year GRATs—and this cycle could be extended over any number of years. This approach can maximize the capture of any outperformance for remainder beneficiaries, provide greater optionality for the donor in deciding whether to deploy payments into new GRATs or use them for other purposes as they are received, and reduce the mortality risk.

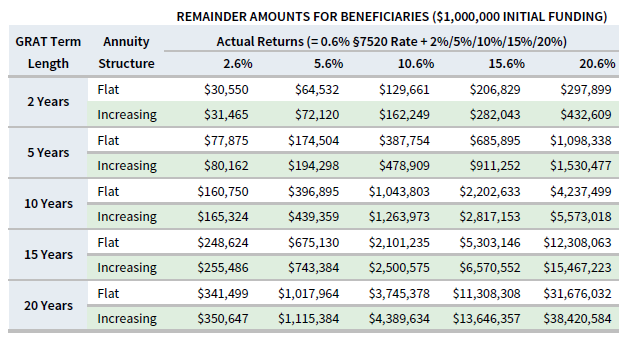

However, a shorter GRAT term also entails the risk of increases in the Section 7520 rate for any future GRATs. Thus, since Section 7520 rates are at record lows, it might be preferable to lock in these low hurdle rates for longer periods while they are available. 4 One could also hedge with a blended approach, using multiple GRATs and a range of GRAT term lengths—a “laddered” approach of sorts, as seen with bonds. Figure 2 illustrates the remainder values for $1,000,000 zeroed-out GRATs with the specified investment returns, term lengths, and payment structures (i.e., flat annuities or annuities increasing by 20% each year) under the 0.6% Section 7520 rate for June 2020. 5

FIGURE 2 GRAT REMAINDER AMOUNTS BASED ON TERM LENGTH, ANNUITY STRUCTURE, AND INVESTMENT RETURN

Source: Cambridge Associates LLC.

Administration and Compliance. Given their asymmetrical cost/benefit profiles, GRATs have often been described as a “free lunch” for those who use them. Indeed, from time to time, concerns arise that the use of GRATs will eventually be prohibited or at least subjected to more restrictions and greater downside tax risk. Even if that does not happen, it is important for a GRAT to be structured, drafted, and funded properly and then administered over time in accordance with its terms and applicable tax rules to secure its benefits without challenge from the IRS.

Investment Considerations

Locking in Outperformance. If a GRAT significantly outperforms its Section 7520 hurdle rate before the end of its term, that surplus return can be locked in for the remainder beneficiaries by selling the outperforming assets and holding cash, short-term fixed income, or other lower risk assets.

If it is not feasible or desirable for the outperforming asset(s) to be sold (e.g., because the asset is illiquid or the donor does not want to realize taxable gain at that time), the outperformance may still be locked in for the GRAT if the donor substitutes other assets of equal fair market value. Since the GRAT is a grantor trust, this substitution will not be a realization event for tax purposes. However, if any of the assets are illiquid or not readily valued, an appraisal may be necessary, and there could be some tax risk if the IRS were to dispute the asserted value.

Concentration and Diversification. Diversification can actually be bad for GRATs. If one asset in a GRAT outperforms the Section 7520 hurdle rate but another underperforms it enough that the aggregate return is close to or short of the hurdle rate, then there will be little or nothing left for the remainder beneficiaries. If instead the two assets were held in separate GRATs, the GRAT with the outperforming asset would have a surplus for the remainder beneficiaries, while the GRAT with the underperforming asset would simply fail at limited cost.

Accordingly, to reduce potential washouts from diversification, one approach is to establish multiple separate GRATs for different asset classes, strategies, or even individual assets (in some cases down to single stocks or other holdings). 6 This method is sometimes combined with the use of short-term rolling GRATs, as described above. Regardless, multiple GRATs require increased costs and resources for administration and compliance.

Selection and Management of Assets. Thoughtful analysis and planning are necessary for the sound investment management of any pool, and even more so for the selection and management of assets contributed to or subsequently held in a GRAT. Asset selection and management considerations that are important during the life cycle of a GRAT may include:

- Selection of initial funding assets, including expected returns relative to the Section 7520 rate;

- Separation or combination of initial funding assets among one or more GRATs;

- Retention or delegation of investment authority;

- Investment-related provisions under the GRAT instrument and/or applicable state law;

- Incorporation of any illiquid assets, including potential valuation requirements and discounts;

- Satisfaction of required payments back to the donor, in cash or in kind; 7

- Distribution or continued retention of assets at the end of the GRAT term; and

- Integration of GRAT assets and flows into the broader investment ecosystem and reporting.

In light of the foregoing, it can be important and helpful to include one’s investment advisors in the consideration and implementation of GRATs, alongside tax and legal advisors.

Conclusion

While recent events and market conditions have created a myriad of challenges for investors, they may nonetheless yield tax, planning, and wealth transfer opportunities in the short term. Key among these is the potential use of GRATs to transfer wealth to the next generation in a tax-advantaged manner. Although this strategy may be compelling, the effective implementation of GRATs is not without complexity. Consideration of these issues as they apply to each unique situation, along with thoughtful orchestration between legal, tax, and investment advisors, is important. In this way, a program can be devised that takes full advantage of the current opportunity while avoiding unintended consequences down the road.

Footnotes

- Unfortunately for donors, this treatment (i.e., determination at inception, regardless of outcome) does not apply for generation- skipping transfer tax purposes. Accordingly, in most cases, a GRAT is less effective and even inadvisable for passing assets to grandchildren and more remote beneficiaries.

- If the donor dies during the GRAT term, the value of any GRAT assets at that time is includible in the donor’s estate and taxable for estate tax purposes, on account of the donor’s retained interest in the GRAT. This essentially nullifies the gift tax benefits of establishing the GRAT and increases the potential opportunity cost of not using other wealth transfer strategies instead of the GRAT.

- Some practitioners advise structuring a GRAT to produce a nominal gift tax value for the remainder, even just a few dollars, to ensure it will be considered a valid gift required to be reported for gift tax purposes in the first place. However, because the ability to zero out a GRAT limits its gift tax downside if assets underperform the Section 7520 rate, it is generally unnecessary and inadvisable to structure a GRAT with a greater than nominal gift tax value for the remainder.

- In some sense, this strategy learns from those fixed income investors in the early 1980s who eventually wished they had acquired more long-term Treasuries, even though short-term rates were significantly higher at the time.

- These illustrations are not meant to suggest that a diversified portfolio or broad asset class will necessarily achieve returns at the higher levels shown, especially over longer time periods. (If only one could reliably achieve a 20.6% annual return over 20 years!) However, some specific assets or asset subclasses could achieve those higher returns, especially over the shorter-term lengths. This underscores the case for concentration in GRATs and the use of multiple GRATs, which is discussed in the Implementation section of this paper.

- Aside from mitigating the potential downside of diversification, holding a single stock or other asset in a GRAT can also be an attractive approach for business owners and others holding concentrated positions.

- There are limits to how long any payment back to the donor may be deferred, and while a GRAT may borrow funds from a third party at arm’s length, it is not permissible for a GRAT to borrow from the donor or to issue a promissory note or other “IOU” to satisfy a required payment.

Chris Houston - Footnotes Unfortunately for donors, this treatment (i.e., determination at inception, regardless of outcome) does not apply for generation- skipping transfer tax purposes. Accordingly, in most cases, a GRAT is less effective and even inadvisable for passing assets to grandchildren and more remote beneficiaries. If the donor dies during the GRAT term, the value of any […]

About Cambridge Associates

Cambridge Associates is a global investment firm with 50+ years of institutional investing experience. The firm aims to help pension plans, endowments & foundations, healthcare systems, and private clients achieve their investment goals and maximize their impact on the world. Cambridge Associates delivers a range of services, including outsourced CIO, non-discretionary portfolio management, staff extension and alternative asset class mandates. Contact us today.