Outlook 2021: A Year of Healing

Introduction

Wade O’Brien, Managing Director, Capital Markets Research

When we suggested that 2020 was “unlikely to be dull” in last year’s outlook, little did we realize just how eventful the last 12 months would turn out to be. COVID-19 upended global financial markets to a greater degree than at any point since the global financial crisis, forcing central banks and governments to take unprecedented actions to shore up economies and accelerate the development of a vaccine. Against this backdrop, our 2020 outlook had a mixed hit rate. As examples, sovereign bonds did provide ballast to portfolios despite low yields, and liquid credit returns were hampered by a starting point of low yields and spreads, but a recommendation to lean into value stocks was another matter.

Looking ahead to 2021, we expect markets and economies to continue their recent healing, and the potential for some of this year’s most significant market moves to decelerate or even reverse causes us to tweak our advice. Central banks around the globe may be unwilling or unable to cut benchmark interest rates further, reducing the upside for sovereign bonds and their diversification benefits. Exact substitutes are not easy to find, but we suggest alternatives like inflation-linked bonds as inflation is likely to rebound off this year’s depressed levels. In liquid credit, we again bemoan the lack of yield and spread on offer and focus again on less-trafficked areas like collateralized loan obligation (CLO) debt.

In equity markets, the outperformance of growth in 2020 has been stunning. However, earnings have not tracked this performance and valuations have risen to nose-bleed levels, creating risks for investors. Quality stocks seem a better option given their steady earnings performance and strong balance sheets. Investors should also not abandon value stocks. Their November 2020 outperformance following positive COVID-19 vaccine news hints at more potential upside if a recovery in global growth occurs in 2021, and either way rock-bottom prices offer downside protection. One exception to this rule is listed energy stocks, which we are not embracing because of concerns over secular changes underway in global energy consumption.

The opportunity set in some alternative strategies remains abundant. Hedge funds performed well in 2020 and certain strategies proved adept at managing the first quarter downturn. Allocators should focus on long/short equity managers for 2021, especially those with hybrid public/private mandates that focus on innovation in fields like life sciences. On the private equity side, we see an opportunity in European growth managers, which have successfully navigated lackluster economic growth in recent years. Finally, in credit we believe the rigorous underwriting standards of many senior direct lenders will continue to generate attractive returns for investors. Should markets again hit some turbulence, private credit opportunity strategies may also be well placed.

Allocators will likely need to navigate more uncertainty in 2021, particularly as it relates to vaccine distribution as well as prospects for additional fiscal stimulus. As the pandemic has underscored, sources of portfolio risk are not limited to traditional factors like valuations or economic growth. Our section on sustainable and impact investing discusses using a “systems lens” to help insulate portfolios from longer-term challenges like climate change and rising social inequality. Unfortunately, in these areas the healing is far from complete.

Fiscal Policy Will Drive Asset Performance in 2021

Sean Duffin, Investment Director, Capital Markets Research

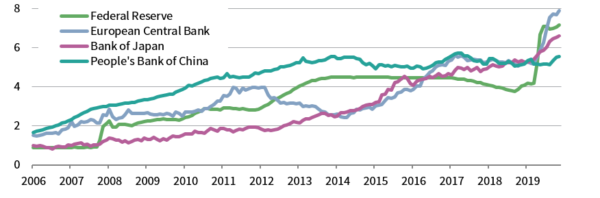

Policymakers took unprecedented actions to limit the economic fallout from the COVID-19 pandemic in 2020. Global rate cuts and massive fiscal spending packages flooded financial markets with liquidity, offering bullish cues to risk assets. While the recently announced trial results of three leading vaccine candidates are a welcome relief, central banks and governments will likely need to continue to provide economic support in 2021, given timelines associated with a vaccine’s distribution. The degree to which additional stimulus overshoots or undershoots expectations will likely be a key driver of asset performance next year.

But central banks have limited firepower left after deploying a full arsenal of tools, including engaging in an unprecedented level of asset purchases. As a result, central banks have pushed for additional government spending, despite nearly $12 trillion of fiscal support in 2020!

CENTRAL BANKS MADE UNPRECEDENTED LEVEL OF ASSET PURCHASES IN 2020

December 31, 2006 – October 31, 2020 • US$ Trillions • Total Assets

Source: Thomson Reuters Datastream.

Governments with economies under pressure will likely prioritize additional fiscal support in 2021, but the magnitude of such policies will hinge on fiscal space and politics. The United States is a primary example, as risk assets have been sensitive to fiscal stimulus negotiations in the latter half of 2020. With two runoff Senate elections scheduled for Jan 5, it looks likely that Congress will remain split, resulting in continued policy gridlock. Such an outcome could limit the size and scope of a future fiscal relief package. Political clashes are also distorting the path of fiscal policy in Europe. EU leaders agreed to a landmark recovery package in July, but member states continue to quarrel over the details. Risk assets will likely be reactive to further developments as member states work toward ratification of the bill.

Global risk assets have performed strongly amid the pandemic, buoyed by the “whatever it takes” attitude of governments and central banks. Still, the timing and scale of the global policy response to the COVID-19 pandemic will remain a key driver of risk appetite in 2021.

The Dollar May Decline, but a Collapse Is Not Imminent

Thomas O’Mahony, Investment Director, Capital Markets Research

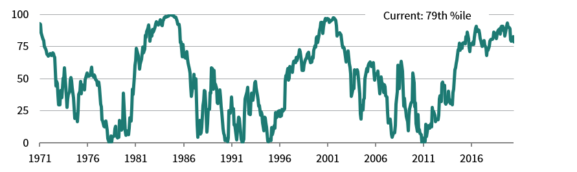

The US dollar has benefited from several tailwinds in recent years, which have seen its valuation reach extended levels. Foremost amongst these has been a widening interest rate spread versus its peers. It has also been aided by a flight-to-quality bid, resulting from the US-China trade spat initially and then the COVID-19 crisis. However, events after the onset of the crisis have seen the dollar weaken as 2020 has worn on, a trend we expect to continue into 2021 for several reasons.

THE DOLLAR WEAKENED AS 2020 WORE ON

June 30, 1971 – November 30, 2020 • Percentile (%)

Sources: Eurostat, MSCI Inc., OECD, Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Note: Real exchange rates are based on relative consumer prices.

Firstly, the currency’s safe-haven premium has eroded as we have moved past the most acute phase of the pandemic. There remains scope for further dollar weakness via this channel as economic activity normalizes and risk-seeking behavior increases. Secondly, the interest rate spread has ceased to be a major support, as the Fed was forced to cut interest rates to near zero, while other major central banks were more bounded in their rate cutting capacities. The carry advantage from long dollar positions is now much reduced, while conversely it is less costly for those wishing to underweight, or outright short, the currency. Finally, elevated US current account and fiscal deficits ensure there is a significant supply of exported dollars, which should exert a gradual depreciating force on the currency.

Nonetheless, talk in the media of an imminent collapse in the greenback is overstated. The dollar remains at the heart of the global financial system. This runs the gamut from having the largest and most liquid asset markets to the invoicing of a predominance of trade in the currency. The enormous stock of USD-denominated debt outside the United States virtually ensures that the dollar will appreciate in the event of further shocks, as deleveraging actors clamour for the currency. Though there is a nascent effort by certain nations to reduce the dollar’s centrality, this is a slow-moving effort that will be eclipsed in importance by cyclical factors. Although the confidence intervals around currency forecasts are necessarily wide, a gradual depreciation of the dollar is our central expectation.

US-China Relations Won’t Improve, but Capital Will Continue to Flow to China

Aaron Costello, Managing Director, Capital Markets Research

US-China relations are unlikely to improve in 2021. Indeed, relations may further worsen under a Biden administration that seeks to readopt a multilateral approach to confronting global issues, particularly human rights issues. Furthermore, given bipartisan hostility to China, the administration will want to maintain a tough stance on China to deflect criticisms from across the aisle. Thus, while the tone and tenor of US rhetoric toward China may become more civil, the underlying tensions will not dissipate in January.

Yet, foreign capital is likely to flow into China in 2021 regardless of the political climate, given China’s recovering domestic economy and high interest rates. Year-to-date through October, foreign holdings of onshore Chinese equities and bonds increased by $13B and $133B (or 9% and 42%), respectively. Indeed, despite the downward spiral in global sentiment toward China, Chinese equities outperformed global markets in 2020, while the renminbi (RMB) appreciated. With ten-year government bonds in China yielding 3.28% versus 0.84% for US Treasuries (and negative yields in Europe), China will continue to attract capital.

CHINA WILL CONTINUE TO ATTRACT CAPITAL

November 30, 2014 – October 31, 2020 • USD Billions

Sources: Bloomberg L.P., Bond Connect Company Limited, China Central Depository & Clearing Co., Ltd., and Shanghai Clearing House.

Notes: Data for foreign holdings of onshore bonds begin June 30, 2017, and represent the total foreign holdings in the depository of the China Central Depository & Clearing Co., Ltd. (CCDC) and the Shanghai Clearing House. Data for foreign holdings of onshore stocks are represented by the Stock Connect Northbound cumulative inflows.

As argued in last year’s outlook, US policies may continue to drive capital away from the United States. The Trump administration’s attempts to force the delisting of US-listed Chinese companies have caused a flurry of secondary listings in Hong Kong and have ironically accelerated reforms that have made China’s domestic IPO market more attractive. The more hostile the United States and the rest of the world becomes to Chinese capital, the more likely Chinese capital will stay at home or return home, helping to support the RMB and domestic asset prices. Thus, we continue to overweight Chinese equities and bonds relative to global benchmarks.

Worsening relations will not necessarily increase risks for investors in China. China wants to reduce its dependence on the US dollar and internationalize the RMB, which is why, despite tensions steadily increasing since 2018, China has not retaliated against foreign investors and continues to open its capital markets. This stance is likely to continue in 2021.

Investors Should Consider Complements to Low-Yielding Sovereign Bonds

TJ Scavone, Investment Director, Capital Markets Research

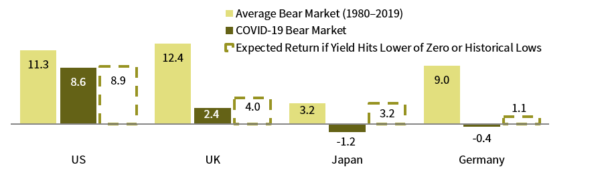

As we head into 2021, ten-year US Treasuries are yielding just 0.84%, while yields in Europe and Japan are stuck near or below zero. While there is considerable uncertainty about the direction of yields during normal times, let alone during a pandemic, we view risks as skewed for yields to rise in 2021. This view is linked to the better-than-expected rebound in economic activity, promising vaccine developments, and extraordinary policy measures. Also, yields tend to rise as economic activity normalizes following recessions—in the last seven US recessions, ten-year US Treasury yields rose by an average of 184 basis points within the 12-month period following their recessionary lows.

Expensive assets can get more expensive, but even if yields decline in 2021 (prices rise when yields decline), the diversification benefits of sovereign bonds are limited given their low starting yields. During the equity sell-off in early 2020, ten-year sovereign bond returns were negative in markets with negative yields and were barely positive in markets with sub-1% yields. US Treasuries held up, but now they have less room to maneuver in a severe equity bear market unless yields fall to zero.

Sovereign bonds will likely still serve as a reliable liquidity reserve alongside cash, but we question the reliability of their other diversifying characteristics (e.g., reasonable expected returns, strong appreciation during equity bear markets, and negative correlations with equities). While there is no perfect substitute, there are a range of assets across the risk spectrum worth considering as complements to sovereign bonds. More traditional “safe” assets, such as gold and inflation-linked bonds, can help offset sharp equity market corrections across a wide range of market environments, but they may struggle as a stable source of liquidity. Investments further out the risk spectrum—including those that take credit, illiquidity, active management, or other uncorrelated market risks—may increase expected returns, but they may be less reliable diversifiers in periods of stress. Although, if yields do rise in 2021 as we suspect, some developed markets sovereign bonds may once again become the most reasonable hedge against equity risk. Ultimately, investors need to understand their liquidity requirements and volatility tolerance, and then evaluate the trade-offs for different diversification opportunities.

SOVEREIGN BONDS HAVE LESS UPSIDE IN FUTURE BEAR MARKETS

As of November 30, 2020 • 10-Yr Sovereign Bond Performance (%) • Local Currency

Sources: MSCI Inc., Ned Davis Research Inc., and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Notes: Average performance during global equity bear markets are based on the nine 20% price declines between 1980 and 2019 for the MSCI World Index prior to 1987 and the MSCI AC World Index thereafter. Performance during the COVID-19 bear market are based on the 2/19/2020–3/23/2020 MSCI AC World bear market. Japan data exclude the first global bear market. The expected return estimates the total nominal return an investor would earn from holding a market index over a specific time horizon and reinvesting the income, given assumptions about the movements in the risk-free rate and roll return. Each portfolio is assumed to have a constant maturity profile where a portfolio of newly issued bonds is purchased on Day 1, held for one year, and then sold at the end of Year 1.

Quality and Value May Outperform Growth

Kevin Ely, Managing Director, Public Equities

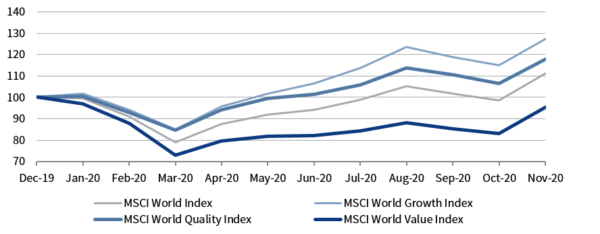

Caution is warranted for growth stocks in 2021. Many of these richly priced stocks look vulnerable if earnings do not deliver. Instead, investors should look to quality, which is more reasonably valued and may also benefit from continued disruption in technology. Investors should also consider value since the valuation disparity between growth and value is historically wide and that these equities have historically performed well following a recession. But given the uncertainty associated with value equities, we recommend a smaller position than quality.

With the expansion of technology’s influence across many industries and with the pandemic increasing demand for tech-enabled goods and services, it makes sense that growth stocks have performed well. In fact, growth has outperformed quality and value by 9.7 and 32.1 percentage points in 2020 through November, according to MSCI World indexes. This has led the price of growth to jump to 30.3x forward earnings whereas the price of quality trades at 23.0x forward earnings. Looking ahead, a preferable way to play the continuing innovation trade is through quality stocks with proven profitability, strong balance sheets, and better valuations. For those investors concerned about lofty tech valuations, quality strategies that are designed to have similar sector exposures as broad equities offer appeal.

GROWTH STOCKS OUTPERFORMED QUALITY AND VALUE IN 2020

December 31, 2019 – November 30, 2020 • December 31, 2019 = US$100

Sources: MSCI Inc. and Thomson Reuters Datastream. MSCI data provided “as is” without any express or implied warranties.

Note: Total return data for all MSCI Indexes are net of dividend taxes.

Investors do not have to pay much today for an option on a recovery for value. At 15.2x forward earnings as of the end of November 2020, value stocks are trading at less than half the multiple noted above for its growth index counterpart. It makes sense that value stocks have lagged in a period of substantial uncertainty where interest rates have been low, global economic growth has been subpar, and secular disruption appears underway in many industries. At some point, these challenges will abate, and a positive payoff seems likely. The timing is uncertain but continued positive news on vaccine developments and distribution may propel value equities in a positive direction.

Capital Flows to European Private Growth Accelerate

Dan Aylott, Managing Director, Private Equity

Peter Maher, Senior Investment Director, Private Equity

European venture capital and growth equity have long been in the shadow of US and Chinese counterparts. However, structural market changes and competitive dynamics in these private growth markets have expanded the opportunity set, which we expect will support the flow of capital in 2021.

The signs have been there for some time. Capital raised by European growth equity funds has nearly quadrupled in the last decade and almost tripled for European venture funds in the same period. As a result, capital invested into these asset classes has risen sharply. Although private fund managers are increasingly turning their attention to European growth opportunities, it remains an undercapitalized asset class. From 2010 to 2018, European companies attracted just 11% of capital invested by growth equity and venture capital funds, according to our data.

European private growth is attractive because many of the most innovative companies are not accessible through public markets. Also, when compared to global peers and European public markets, these companies have performed strongly over all time horizons. Relatedly, our data show that managers investing in European companies with more than 20% growth in sales achieved a greater than 2.0x gross multiple on invested capital (MOIC) 76% of the time. These returns are especially notable given that broader GDP growth in Europe has been lackluster for years. Lastly, many US firms are transitioning resources to Europe, anticipating greater demand for European companies.

Investors have multiple options for capturing European private market growth opportunities. Late-stage venture capital is appropriate for investors comfortable reaching out on the risk curve. Minority growth equity and growth buyout strategies are popular ways to access structural tailwinds in a post-COVID Europe that could see slower economic growth overall. Across all these strategies, healthcare and technology exposures feature strongly—even as part of a more generalist approach—and are two sectors that have proved the most resilient to the extraordinary circumstances of 2020.

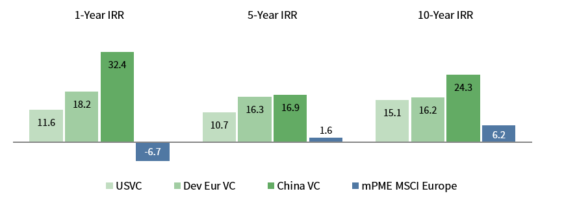

EUROPEAN VENTURE CAPITAL RETURNS STRENGTHENING OVER TIME

As of June 30, 2020 • Percent (%) • US Dollar

Sources: Cambridge Associates LLC and MSCI Inc. MSCI data provided “as is” without any express or implied warranties.

Notes: CA Modified Public Market Equivalent (mPME) replicates private investment performance under public market conditions. The public index’s shares are purchased and sold according to the private fund cash flow schedule, with distributions calculated in the same proportion as the private fund, and mPME NAV is a function of mPME cash flows and public index returns. MSCI Europe mPME returns reflect Dev Eur VC fund flows. MSCI returns are net of dividend taxes.

Credit Investors Should Avoid Index-Like Exposure in 2021

Wade O’Brien, Managing Director, Capital Markets Research

Credit investors face tough choices as 2021 approaches. Fundamentals have softened dramatically for some sectors, and their path to recovery could be prolonged. While many borrowers proved adept at tapping short-term sources of liquidity as the pandemic hit, fewer options may be available if prospects have not improved by the middle of next year. Against this backdrop, spreads for many assets are below historical averages, compressed by central bank intervention and a general thirst for yield. Investors need to be nimble and patient. Publicly traded assets are picked over, though prices for a few (like CLO liabilities) offer cushion if conditions deteriorate. Private markets offer richer opportunities, and any further dislocation should particularly benefit managers in the capital opportunity space.

The rapid recovery in credit markets has been extraordinary. US high-yield bond option-adjusted spreads peaked at 1,100 bps in March, but they have compressed to near 400 bps. This level is roughly 15% below their historical median, despite elevated default rates and rising corporate leverage. Current spreads could represent fair value if the current default cycle is near its peak. However, if recent COVID-related shutdowns are extended or if reduced demand for some companies becomes permanent, defaults could become more common across sectors (nearly 80% of year-to-date defaults involve energy and telecommunication companies). In contrast to high yield, CLO mezzanine debt remains attractive. Distributions have been maintained, and defaults in underlying CLO pools have been much lower than broad market averages.

But private credit strategies offer richer pickings than public. As discussed in greater detail in the accompanying section, senior direct lending strategies now offer higher spreads, better documentation, and lower leverage than they did pre-COVID. For investors seeking higher returns, capital opportunity strategies investing across the capital stack are well placed to capitalize on any further dislocation. Unlike traditional distressed-for-control strategies, which saw limited deal flow in 2020, capital opportunity funds were busy following the onset of the pandemic, investing in dislocation, rescue finance, liquidation, and other trades. The supportive Federal Reserve backdrop and accommodating public markets have pushed prices higher in recent months, and existing investors have helped shore up struggling firms. While the opportunity set has faded somewhat, a renewed dip in economic activity in 2021 or ongoing changes in consumption stemming from COVID-19 could spur returns for these strategies.

The uncertain outlook and low yields mean credit investors should not just focus on their home markets in 2021. Not all governments have had the same resources to support struggling companies that the United States and European countries have enjoyed. This is generating a variety of opportunities in emerging markets, including buying non-performing loans from local banks and stepping in to buy discounted claims from cash-starved companies. An additional benefit is that these markets see less competition for deals, raising the chances that returns will be higher.

Direct Lending Will Offer Solid Returns With Proven Seniority

Christine Farquhar, Managing Director, Global Head of Credit Investment Group

Senior direct lending may not look like the most obvious investment for 2021, but the private credit market is maturing as direct lenders step in for banks. Particularly among smaller cap borrowers, corporates are accepting stronger covenants and better financial redress for investors providing senior debt. Seasoned managers are well placed to capture the yield premia on offer and deliver attractive returns for the 2021 vintage investors.

While COVID-19 is having an uneven impact across sectors, businesses already in difficulty are facing added pressure. We are seeing upturns in both technical defaults (covenant breaches) and smaller scale delays in interest and capital repayments. But formal bankruptcies have been far fewer in direct lending portfolios than in the broadly syndicated loan (BSL) market, consistent with lower leverage multiples and better-quality underwriting. Direct lending portfolios have benefited from holding fewer cyclical names, including those in COVID-impacted sectors, such as airlines, hotels, and theme parks.

BUSINESSES ALREADY IN TROUBLE ARE FACING ADDED PRESSURE

As of November 30, 2020 • Percent (%)

Source: BofA Securities, Inc.

Notes: Chart shows percentage of high-yield bonds trading 1,000 or more basis points over the risk-free rate. Cable, food producers, and packaging/paper each had a ratio of 0.0.

Size matters, and it is possible that smaller borrowers outside of the BSL market have less access to rescue support from equity shareholders, including private equity sponsors. However, this has not been an obvious feature in past vintages, and direct lending managers are well positioned to step in via loan covenants to reset borrowing terms and help the businesses through near-term difficulties. We see evidence that the same is happening presently, but success is predicated on the original underwriting quality.

Senior debt, conservatively underwritten, is not offering much beyond single-digit net IRRs. Funds are typically locked up for four to eight years. These are not to be confused with opportunistic or distressed debt strategies seeking a 20%+ IRR. Security for direct lenders comes from the debt’s seniority and the fund manager’s skills, including using the lock-up period to call in the covenants and pre-empt or limit capital loss. While covenant breaches are technically defaults, skilled workouts can secure better results than bankruptcy proceedings. Seasoned teams with experience in sourcing, structuring, and credit workouts are well placed to deliver solid returns.

Emphasize Hedge Funds Focused on Technological Disruption

Eric Costa, Global Head of Hedge Funds

Tom Gormley, Managing Director, Hedge Funds

As COVID-19 spread around the world, many investors anticipated a prolonged opportunity in distressed investing. The opportunity set has yet to materialize, as fiscal and monetary policies have kept markets liquid and propped up asset values. Looking to 2021, we expect hedge fund strategies that exploit technological disruption across industries will fare better than those that rely on merger arbitrage spreads or economic distress.

The challenging environment for traditional distressed corporate credit is likely to persist, given we believe governments and central banks will continue to support economic activity. Some industries that were hardest hit by the pandemic, such as airlines and cruise operators, have been backstopped, while others, such as energy and retail, hold little interest for most distressed investors. The prospect of a meager opportunity set combined with a large amount of capital dedicated to strategies that pursue distressed assets may lead to another muted year.

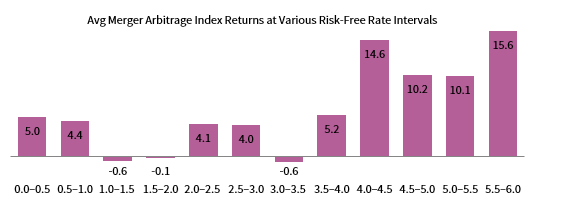

Absent a robust distressed cycle, event-driven managers will have to turn their attention to other types of corporate activity, such as mergers & acquisitions and special situations. Deal activity, which had screeched to a halt due to pandemic-related shutdowns globally, is showing signs of life. But with merger arbitrage returns broadly driven by high interest rates, profitable trades in merger arbitrage may also be limited.

PROFITABLE TRADES IN MERGER ARBITRAGE MAY BE LIMITED

December 31, 1993 – October 31, 2020 • Percent (%)

Sources: Credit Suisse, Hedge Fund Research, Inc., and Thomson Reuters Datastream.

Notes: Merger arbitrage returns are represented by an average of the returns to the HFRI Event Driven Merger Arbitrage Index and the Credit Suisse Event-Driven, Risk Arbitrage Index. The risk-free rate is represented by the US Treasury 91-Day Bill Yield. Hedge Fund Research data are preliminary for the preceding five months.

When plentiful, both merger arbitrage and distressed investing can absorb large amounts of capital. Since these strategies currently appear unattractive, we expect more niche event-driven investments, such as spin-offs, special purpose acquisition companies (SPACs), and activist campaigns will receive more attention. While smaller, nimbler managers may find interesting opportunities, larger event-driven managers may continue to find it challenging to deploy substantial capital at attractive rates of returns.

Therefore, we think talented long/short equity managers employing a hybrid public/private approach, as well as sector-specific strategies, are compelling. Innovation occurring in both the US and Chinese technology and life sciences sectors should persist and continue to produce significant disruption that creates considerable long and short opportunities.

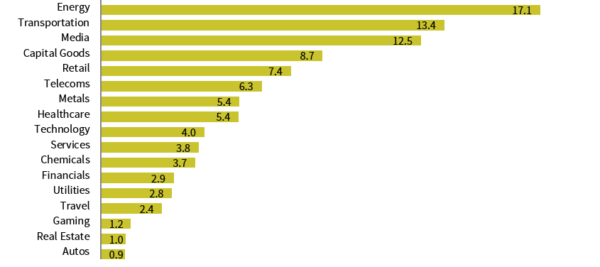

Energy’s Underperformance Continues

Kevin Rosenbaum, Global Head of Capital Markets Research

It is easy to hate energy investments. Overlooking their environmental impact, global listed energy companies have underperformed global broad equities by nearly 43 percentage points (ppts) in the first 11 months of 2020, according to MSCI indexes in USD terms. Of course, this floundering is nothing new. Looking at the last ten-year period, the magnitude of underperformance rises to a staggering 169 ppts. Normally, pessimism that excessive piques our interest. But some trends don’t easily revert. For us, sluggish earnings, a persistent valuation gap, and continued concern about the long-term prospects of hydrocarbons suggest disappointment continues next year.

Earnings of global listed energy companies fell dramatically in 2020. At an index level, earnings dropped from $15 a share at the start of the year to less than $1 at the time of publication. While analysts see growth in 2021, earnings are only expected to rebound to roughly 60% of their pre-pandemic level. But much depends on oil prices, which have been an increasingly important driver of earnings. Furthermore, that commodity market looks poised to remain under pressure, given global oil demand is likely to be structurally lower for some time and OPEC and its partner countries will struggle to extend their significant oil production cuts if oil prices rise.

We also doubt investors will value the earnings of energy companies at a materially higher level. Presently, developed energy companies trade at 3.9x cyclically adjusted cash earnings, which is sharply lower than the level of broad equities (15.3x). While progress in vaccine development and distribution may give a greater near-term valuation boost to energy equities than broad equities, we suspect it will be modest. This is partly because investors will not forget that energy companies have generally been poor stewards of capital. But, perhaps more importantly, investors will also not overlook the large threat renewable energy poses to the hydrocarbon-heavy energy sector.

RENEWABLE ENERGY USAGE POISED TO EXPAND RAPIDLY

As of January 2020 • US EIA Reference Case Forecasts • Percent (%) of Primary Energy Consumption

Source: US Energy Information Administration.

A challenge in thinking about the energy sector’s future performance is its higher levels of volatility. So, while we believe that energy will continue to struggle against the broad market next year, our conviction level is low.

Lean into Asset Class Connections to Drive Better Portfolio and Societal Outcomes

Liqian Ma, Global Head of Sustainable and Impact Investing Research

Heading into 2021, investors continue to face significant challenges involving the global pandemic, climate change, and structural social inequality. All three of these systemic risks have a sense of urgency that, if properly addressed through a sustainability lens, should enhance long-term portfolio resilience. Investors may find it natural, and even comforting, to stay narrowly focused on the near-term, actionable opportunities in specific asset classes. But doing so risks missing key causal connections and opportunity themes across asset classes.

Indeed, 2021 provides an opportunity for investors to navigate key sustainability trends by applying a systemic lens to intentionally and holistically redesign portfolios. Take climate change mitigation as one example. Investing in renewable energy infrastructure is one obvious and asset class–specific approach. But a systemic approach would combine several strategies across asset classes, including but not limited to: 1) investing in sustainable real assets; 2) pursuing venture and growth strategies that focus on digital solutions to accelerate a low-carbon transition; 3) engaging with all managers on how they are managing climate risk; and 4) using available tools to analyze the portfolio carbon exposure and managing down that carbon intensity over time toward a “net zero” target. Investors can then extend further into climate adaptation themes, such as affordable housing, equitable healthcare solutions, and physical risk data analytics. Without this systemic approach, one risks not appropriately addressing the underlying root cause of climate change.

Another example is digital infrastructure, which has implications for social equity and environmental sustainability. As remote work and learning continue into 2021, digital infrastructure investments in fiber, wireless networks, and middleware (accessed via real assets and private equity) and at the application layer (via venture capital) can help accelerate digitization and expand access, especially for underserved communities. At the same time, some of these infrastructure investments carry “smart city” applications, which can improve both the energy efficiency, as well as fiscal positions for municipalities. In a systemic approach, this one seemingly narrow theme of digital infrastructure can cut across venture capital, private equity, real assets, and credit all while playing a role in addressing social and environmental pain points.

To implement a systems-oriented approach, investors need to engage managers at a deep level to understand underlying themes and exposures. They also need to connect those themes across asset classes to form causality-driven theses, and then allocate capital to those connections where return-enhancing opportunities and impactful solutions intersect. While it is easier than ever to feel disconnected and siloed, investors that identify and build thematic connections across asset classes in 2021 will be positioned to drive better long-term portfolio and societal outcomes.

Conclusion

Celia Dallas, Chief Investment Strategist

As 2020 comes to a close, we expect some key investment drivers to persist in the new year. We believe that efforts to contain the spread of COVID-19 will continue to limit economic activity, and that fiscal and monetary policy will remain accommodative in an effort to offset the impact of the pandemic. While progress on vaccine development has been impressive, production and distribution will take time. As a result, countervailing forces are likely to impact markets next year, with risk assets outperforming if there’s more-than-expected stimulus and progress in combatting COVID-19 and defensive assets outperforming if economic activity and and vaccine distribution suffers setbacks.

Amid disappointment related to COVID-19 containment, tech-enabled disruptive companies have dominated, continuing a trend that predates the pandemic. In a world of ultra-low yields and slow growth, disruptive businesses are even more valuable. There are several ways to play growth, including via high-quality public equities, long/short hedge funds, and private investments (e.g., strategies targeting European companies). Conversely, value stocks have been held back by such conditions and offer a cheap means to benefit as the severity of the pandemic lessens.

In fixed income, we expect high-quality sovereign bonds to remain a reliable liquidity reserve, but low yields have pruned their diversification characteristics. While there is no substitute for such traditional safe havens, investors should carefully size allocations in the context of cash sources and uses and explore other complements for added diversification with less opportunity cost. Moving out the fixed income risk spectrum, investors should tread carefully in credit. Central bank support has enabled credit spreads to tighten as fundamentals have weakened. CLOs, other less liquid strategies, and private credit, particularly direct lending, offer appeal.

We also expect US-China tensions to persist with a Biden administration. But, like 2020, foreign capital is likely to continue to flow into China, supporting asset prices and the RMB. The newly opened Chinese government bond market is worth considering. The market offers an attractive source of diversification with a chunky yield premium over developed markets sovereign bonds. This is especially the case in USD terms, given that we expect pressures to continue to weigh down the greenback.

For us, the global pandemic and ongoing environmental and social equity challenges highlight the appeal of driving better portfolio outcomes and societal outcomes at the same time. A systems lens approach can be used to capitalize on appealing cross-asset connections throughout the portfolio. Such a lens points to the challenges associated with public oil & gas investments that are suffering under long-term disruptive trends as much of the world shifts to renewable energy.

Ultimately, we anticipate 2021 will be a year of healing for the global economy. While society will eventually join in on the healing, thanks to the exceptional progress on vaccines, conditions may worsen before they improve. Investors should remain diversified, maintaining exposure to tech and tech-enabled investments, as well as value investments, focusing on sustainability across the portfolio, and taking advantage of pockets of the credit markets that offer value.

Drew Boyer, Kristin Roesch, Vivian Gan, Caryn Slotsky, and Zack Barrett also contributed to this publication.

Index Disclosures

Credit Suisse Event Driven Risk Arbitrage Hedge Index

The Credit Suisse Event Driven Risk Arbitrage Hedge Fund Index is a subset of the Credit Suisse Hedge Fund Index that measures the aggregate performance of risk arbitrage funds. Risk arbitrage event driven hedge funds typically attempt to capture the spreads in merger or acquisition transactions involving public companies after the terms of the transaction have been announced. The spread is the difference between the transaction bid and the trading price. Typically, the target stock trades at a discount to the bid to account for the risk of the transaction failing to close. In a cash deal, the manager will typically purchase the stock of the target and tender it for the offer price at closing. In a fixed exchange ratio stock merger, one would go long the target stock and short the acquirer’s stock according to the merger ratio, in order to isolate the spread and hedge out market risk. The principal risk is usually deal risk, should the deal fail to close.

HFRI ED: Merger Arbitrage Index

The HFRI ED: Merger Arbitrage Index includes strategies which employ an investment process primarily focused on opportunities in equity and equity related instruments of companies, which are currently engaged in a corporate transaction. Merger Arbitrage involves primarily announced transactions, typically with limited or no exposure to situations which pre-, post-date or situations in which no formal announcement is expected to occur. Opportunities are frequently presented in cross border, collared and international transactions which incorporate multiple geographic regulatory institutions, with typically involve minimal exposure to corporate credits. Merger arbitrage strategies typically have over 75% of positions in announced transactions over a given market cycle.

MSCI All Country World Index

The MSCI ACWI is a free float–adjusted, market capitalization–weighted index designed to measure the equity market performance of developed and emerging markets. The MSCI ACWI consists of 49 country indexes comprising 23 developed and 26 emerging markets country indexes. The developed markets country indexes included are: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom, and the United States. The emerging markets country indexes included are: Argentina, Brazil, Chile, China, Colombia, Czech Republic, Egypt, Greece, Hungary, India, Indonesia, Korea, Malaysia, Mexico, Pakistan, Peru, Philippines, Poland, Qatar, Russia, Saudi Arabia, South Africa, Taiwan, Thailand, Turkey, and the United Arab Emirates.

MSCI World Index

The MSCI World Index represents a free float–adjusted, market capitalization–weighted index that is designed to measure the equity market performance of developed markets. It includes 23 developed markets country indexes: Australia, Austria, Belgium, Canada, Denmark, Finland, France, Germany, Hong Kong, Ireland, Israel, Italy, Japan, the Netherlands, New Zealand, Norway, Portugal, Singapore, Spain, Sweden, Switzerland, the United Kingdom, and the United States.

MSCI World Growth Index

The MSCI World Growth Index captures large- and mid-cap securities exhibiting overall growth style characteristics across 23 developed markets countries. The growth investment style characteristics for index construction are defined using five variables: long-term forward EPS growth rate, short-term forward EPS growth rate, current internal growth rate and long-term historical EPS growth trend, and long-term historical sales per share growth trend.

MSCI World Quality Index

The MSCI World Quality Index is based on MSCI World, its parent index, which includes large- and mid-cap stocks across 23 developed markets countries. The index aims to capture the performance of quality growth stocks by identifying stocks with high-quality scores based on three main fundamental variables: high return on equity, stable year-over-year earnings growth, and low financial leverage.

MSCI World Value Index

The MSCI World Value Index captures large- and mid-cap securities exhibiting overall value style characteristics across 23 developed markets countries. The value investment style characteristics for index construction are defined using three variables: book value to price, 12-month forward earnings to price, and dividend yield.