Keeping Underwater Endowments Afloat (and the Programs They Support)

When endowment funds slip “underwater” (below the historic dollar value of the original gift), institutions face a tradeoff between distributing anticipated budget support and restoring the endowment to its original value. Ultimately, the choice of underwater policy depends on the situation and needs of each institution in balancing endowment preservation with program support.

Prior to the 2006 promulgation of the Uniform Prudent Management of Institutional Funds Act (UPMIFA 1 ), spending was not permitted from a donor-restricted endowment that had fallen “underwater,” i.e., below its historic gift value. This model legislation added new governing principles to the legislation adopted under its predecessor, the Uniform Management of Institutional Funds Act (UMIFA), with one of the notable changes pertaining to spending from underwater endowments. The concept of “historic dollar value” was eliminated, so as states began to adopt the legislation starting in 2008, institutions within those states received more flexibility when determining whether to spend from underwater endowments.

However, legislative flexibility is not the only consideration for nonprofits grappling with newer endowment funds with market values that may be lower than or approaching the initial gift value. Institutions in this position are also thinking about donor relations, budgeting and planning, and the goal of intergenerational equity—for endowment funds to serve multiple generations on an equal basis.

While the newest endowments are the most susceptible to falling below the initial gift value during low return and negative market cycles, even a diversified policy portfolio can be expected to experience significant declines from time to time. Our models suggest that the probability of a market value decline of more than 20% (after spending) at any point over a ten-year period is 38%. In a low-return environment, that probability could increase to 55%. 2 Gift policies that extend the period before spending from a new endowment are one way to mitigate the risk of a decline in those funds. Underwater endowment spending policies are another way of dealing with the issue.

This note shares findings from a recent survey of how peer institutions manage underwater endowments, and analyzes the impact of policy decisions on an illustrative portfolio under different market conditions. Lastly, it summarizes the factors that fiduciaries may wish to weigh when determining policies that will best preserve and use endowment assets, respect the intent of donors, and serve the beneficiaries of their generosity.

Peer Practices: Recent Cambridge Associates Survey Results

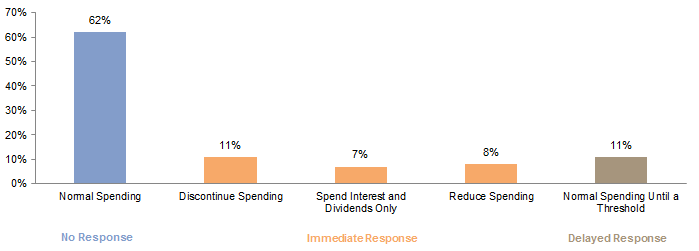

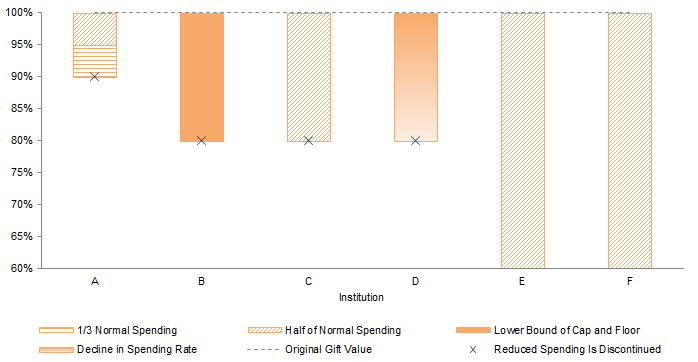

In January 2016, a Cambridge Associates survey of nonprofit clients asked: What is your current policy/practice for spending from “underwater” endowments? Over 60% of respondents (44 of 71) indicated that they spend from the underwater endowment using the normal spending rate and rule (Figure 1). Remaining respondents modified their spending in some way, with 26% reacting immediately. Immediate responses to the underwater state fell into three main categories: (1) discontinuing spending as soon as the market value declines below initial gift value, (2) reducing spending by spending only dividend and interest income, or (3) reducing spending by a particular amount once underwater and then, in some cases, suspending it when the endowment hits a pre-determined threshold. Figure 2 depicts the range of modifications that the six institutions in the third category apply to the spending policy of underwater endowment funds.

Figure 1. Institutions’ Current Policy for Spending from Underwater Endowments

As of January 2016 • n = 71

Source: Cambridge Associates survey of endowments and foundations.

Figure 2. Details of Adjustments for Immediate Response Policy: Reduce Spending Once Underwater

As of January 2016 • Percent (%) of Original Principal • n = 6

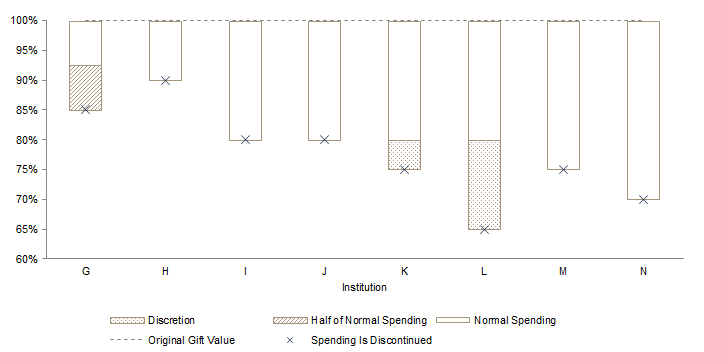

Other respondents wait to react, distributing according to their normal spending policy until they arrive at a pre-determined threshold amount. At that point, spending is either suspended entirely or reduced. For these institutions, the threshold percentages of the original gift value range from 70% to 92.5%. The “x” on Figure 3 indicates, for each institution, the endowment value that triggers a halt to distributions. Three of the institutions that apply a threshold response modify the spending formula before terminating the distribution.

Figure 3. Details of Adjustments for Delayed Response Policy: Normal Spending Until a Threshold

As of January 2016 • Percent (%) of Original Principal • n = 8

Crafting Policy: A Balancing Act

Institutions questioning if and when they should moderate spending from underwater endowments need to consider the impact of the policy on the operating budget and the programs supported by the endowments, as well as on the long-term market value of the endowment. Donor intent, gift agreements, and donor relations may also inform policy choices. To evaluate how the different policy options may change endowment distributions and market values, the following analysis simulates underwater spending policies during a period of market decline and illustrates the impact of the policies on the endowment value and the enterprise.

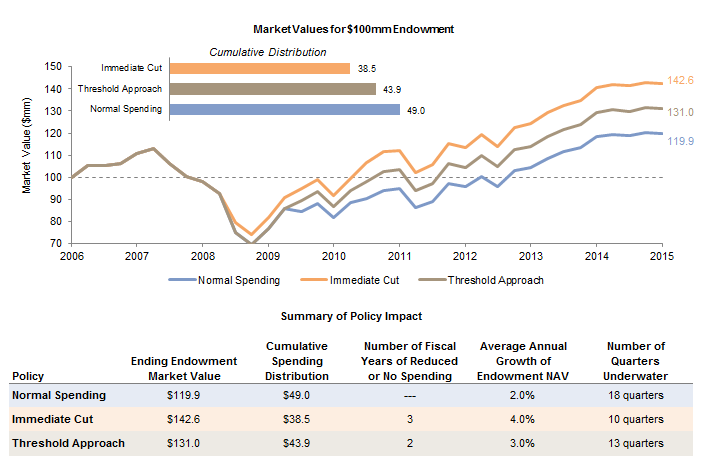

Our modeling analyzes a $100 million endowment with a simple portfolio on the precipice of the market downturn. 3 The market downturn of 2007–08 provides a stress scenario that sheds light on the implications of the different policy levers once the endowment falls below its initial gift value. Given the policies followed by respondents to our survey, we model three policy responses: “normal spending,” “immediate cut,” and “threshold approach” (Figure 4).

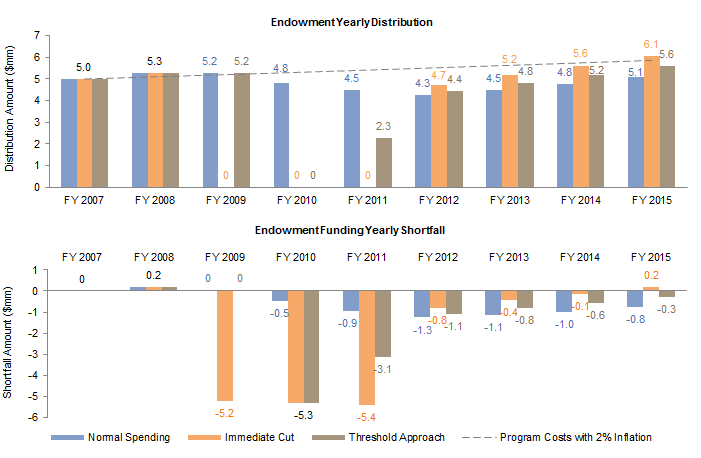

Figure 4. Illustration of the Endowment Impact of Three Underwater Endowment Policies in a Stress Scenario

June 30, 2006 – June 30, 2015

Notes: Portfolio modeled is a $100 million endowment with 70% US equities (S&P 500) and 30% US bonds (Barclays Aggregate). “Normal spending” policy indicates an institution that adheres to its spending policy regardless of endowment value. The “threshold approach” policy models an approach that cuts the spending policy by 50% when the endowment value drops to 90% of the original gift value and then stops spending if the value drops below 80% of the original value. The “immediate cut” policy eliminates spending as soon as an endowment is measured at a value lower than the initial gift value.

Normal Spending. The institution that adheres to its spending policy and forgoes an underwater endowment spending policy will distribute the most consistent and highest spending stream to operations when the endowment market value falls. Normal spending policy results in total spending of $49 million. However, the average endowment growth rate is just 2.0% and the endowment is underwater for 18 quarters during this period.

Immediate Cut. An institution that eliminates spending as soon as an endowment is underwater achieves the highest endowment market value at the end of the ten-year period—the endowment grows at a rate of 4.0% annually and recovers to its original gift value after ten quarters. However, this response also results in the lowest total spending from the endowment, $38.5 million over the ten-year period. The endowment also does not distribute any funding to operations in fiscal years 2009, 2010, and 2011 in our model, which are downturn/post-downturn years when other operating revenues could also be under pressure.

Threshold Approach. The threshold approach falls between the normal spending and immediate elimination of spending responses in terms of ending market value and cumulative spending: the endowment grows at a rate of 3.0% annually and total spending is $43.9 million over the ten-year period. The endowment does not distribute any funding to operations in fiscal year 2010 and spends at 50% in 2011. The endowment recovers after 11 quarters, but after a short recovery it dips below the original market value for two more quarters before a full recovery.

In addition to considering the effects of each policy on cumulative spending over the ten-year period and ending market value, the normal spending policy creates a long-term tradeoff in a negative investment environment. Normal policy will “lock in” a larger amount of permanent losses from selling assets at depressed valuations during the risk-off period, which could be characterized as a penalty that the institution must pay to maintain the consistency of spending. This might be a very worthwhile cost for an institution with high fixed costs and/or high endowment reliance, but for others with more budget flexibility the opportunity cost may be too high.

Impact on Program Funding

Endowments support specific elements of the institutional mission; therefore, before implementing an underwater endowment policy, an institution needs to weigh the tradeoffs between restoring the endowment’s value and long-term purchasing power, and the near-term implications of endowment support to current operations. If budgeted revenue is disrupted, corrective action needs to occur in the budget process. This reaction will be more significant if the endowment distribution is a sizable component of budgeted operating revenue. Either the institution will need to reduce the activity that was to be funded by the distribution, or maintain the activity by finding other sources of funding that will offset the endowment spending shortfall. Just as spending in down markets presents opportunity costs for the long-term investment portfolio, reducing or eliminating spending can present opportunity costs for the enterprise.

Continuing our example of the $100 million endowment, Figure 5 considers the impact on program support under each policy approach. The program costs, and endowment funding, start at $5 million in the first year. If program costs grow at the rate of inflation (2% estimate), the endowment falls short of funding goals during the negative market cycle modeled, with the exception of the immediate cut policy in 2015. The charts demonstrate the dramatic impact that immediate cut and threshold approach underwater endowment policies would have on program funding during a market downturn like 2008.

Figure 5. Illustration of the Program Support Impact of Three Underwater Endowment Policies in a Stress Scenario

June 30, 2006 – June 30, 2015

Notes: Portfolio modeled is a $100 million endowment with 70% US equities (S&P 500) and 30% US bonds (Barclays Aggregate). “Normal spending” policy indicates an institution that adheres to its spending policy regardless of endowment value. The “threshold approach” policy models an approach that cuts the spending policy by 50% when the endowment value drops to 90% of the original gift value and then stops spending if the value drops below 80% of the original value. The “immediate cut” policy eliminates spending as soon as an endowment is measured at a value lower than the initial gift value. Fiscal year begins July 1 and ends June 30.

All scenarios have some funding shortfall from the underwater endowment. The timing of the shortfall is also a consideration. The immediate cut policy, which is designed to restore endowment value as quickly as possible, results in the greatest shortfall during the market downturn from 2009–11. The threshold approach policy provides more time before distributions are cut in 2011 and 2012. The normal spending policy shortfalls are smaller and spread over six years, starting in 2010. Policies that emphasize preservation of the endowment market value require a sacrifice of support for current operations. Swift policy reactions demand quick adaptations for the enterprise, and this may include program changes, communicating with donors, and accessing resources beyond the endowment.

Underwater Response in a Low Return Environment

Revisiting the global financial crisis provides a stress scenario that pulled newer endowments underwater. In our simulations of the fiscal year 2006 to 2015 period, all policy options recover fairly swiftly given the market rebound that followed the global financial crisis. The next crisis is not likely to look exactly like the last one, and the path to recovery may not be as swift.

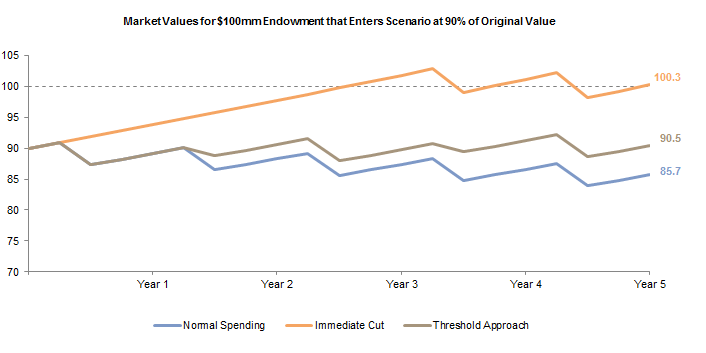

Given current conditions, institutions are thinking about policy choices in a low growth environment. If an endowment enters a low return scenario 4 at 90% of its original value and the low returns persist for five years, only an immediate spending cut would restore the underwater endowment to its initial gift market value by year five (Figure 6).

Figure 6. Illustration of the Endowment Impact of Three Underwater Endowment Policies in a Low Return Scenario

Market Value (USD millions)

Notes: Portfolio modeled is a $100 million endowment with 70% US equities (S&P 500) and 30% US bonds (Barclays Aggregate). “Normal spending” policy indicates an institution that adheres to its spending policy regardless of endowment value. The “threshold approach” policy models an approach that cuts the spending policy by 50% when the endowment value drops to 90% of the original gift value and then stops spending if the value drops below 80% of the original value. The “immediate cut” policy eliminates spending as soon as an endowment is measured at a value lower than the initial gift value.

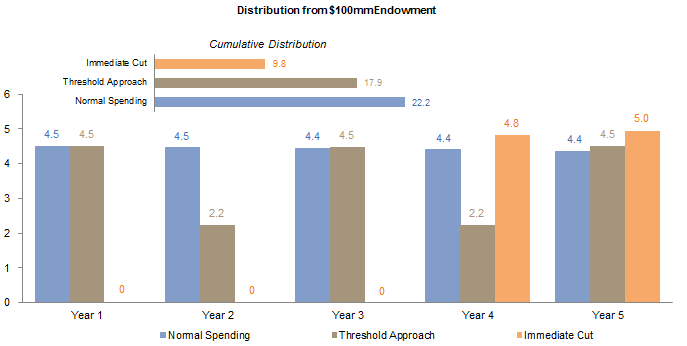

The limited or eliminated distributions to current operations in the low return environment could persist. With an immediate cut policy, the spending freeze continues for three years. Under the threshold approach, the endowment would distribute reduced spending during years two and four. Over this five-year scenario, the immediate cut policy distributes less than half the amount of the normal spending policy (Figure 7). The immediate cut policy will require the elimination of $12 million in program costs, or the acquisition of $12 million in funding from alternative resources, or some combination of cost reductions and alternative funding.

Figure 7. Illustration of the Spending Distribution Impact of Three Underwater Endowment Policies in a Low Return Scenario

Spending Amount (USD millions)

Notes: Portfolio modeled is a $100 million endowment with 70% US equities (S&P 500) and 30% US bonds (Barclays Aggregate). “Normal spending” policy indicates an institution that adheres to its spending policy regardless of endowment value. The “threshold approach” policy models an approach that cuts the spending policy by 50% when the endowment value drops to 90% of the original gift value and then stops spending if the value drops below 80% of the original value. The “immediate cut” policy eliminates spending as soon as an endowment is measured at a value lower than the initial gift value.

Conclusion

The choice of underwater policy depends on the situation and needs of each institution, and there is no “correct” policy. Current UPMIFA principles provide fiduciaries some leeway to interpret the best path for their institution.

Several questions should be considered when determining an underwater endowment policy that will best serve the institution and carry out the intent of the donors:

Can the enterprise absorb a disruption to spending policy?

- How reliant is the institution’s mission on distributions from endowments that are below or are approaching underwater levels?

- Would the institution be willing and able to reduce or suspend the programs that underwater endowments support if distributions are interrupted?

- What percentage of the overall endowment portfolio is underwater? If it is a significant percentage, then the disruption to spending driven by an immediate response will have significant budget ramifications, especially if the commitments to the programs the endowments funds are fixed costs.

- Are there other sources of funding (liquidity outside the long-term investment portfolio or unrestricted endowment) that could fill the funding gaps left by suspended spending?

Even when endowment distribution represents a modest amount of operating revenues, the proceeds can support important programs and commitments. If the programs, positions, and scholarships are fixed, regardless of endowment distribution, then the costs will require funding from other sources such as unrestricted gifts, working capital, or program revenues. Is the institution better off temporarily depleting a portion of the original gift to fund the donor’s intent, or diverting other operating funds to support the initiative? More generally, what is the higher priority: preservation of the market value or the consistency of endowment distributions?

The answers to these questions will reveal the institution’s priorities when addressing underwater endowments, and help the board identify policy choices that reflect those priorities. If the institution leans more toward wanting to preserve the market value of its endowment funds, then the immediate elimination of spending is the option most responsive to that goal. Alternatively, if the institution favors maintaining a consistent annual distribution, then adhering to the normal spending policy even when endowments fall underwater is likely to be the option chosen. Threshold responses and reducing the normal spending policy rate are policy choices that fall somewhere in the middle and attempt to strike a balance between the goals of preserving endowment market value and consistency of annual spending.

Footnotes

- UPMIFA is adopted by US states, and specific state statutes can differ. Institutions should determine their interpretation and approach to endowment management in light of their state’s legislation and after conferring with legal counsel.

- Analysis is based on a portfolio with following asset allocation: 22% US equities, 16% international equity, 7% emerging markets equity, 11% bonds, 20% hedge funds, 8% private equity and venture capital, 9% real assets and inflation linked bonds and 7% cash and other investments. Analysis considers Cambridge Associates “equilibrium” scenario as well as our “return-to-normal” scenario to model a low return environment. CA’s “equilibrium” capital market assumptions are long-term assumptions based on a historical review of each asset class and its relationship to others, beginning with the core assumption that the greater the variability of returns of an asset class, the higher the returns must be to compensate investors for incurring more risk. In the “return to normal” scenario, we incorporate current valuations and assume equity valuations revert to fair value over ten years. This scenario makes assumptions about the market environment including mild inflation, moderate real earnings growth, and low corporate default rates, government bond yields, and credit spreads.

- In the model, returns are applied on a quarterly basis to a portfolio composed of 70% S&P 500 and 30% Barclays Aggregate Bond Index. The portfolio is rebalanced annually.

- In the low return or “return to normal” scenario, we incorporate current valuations and assume equity valuations revert to fair value over ten years. We assume that a 70% equity/30% bond portfolio’s average annual compound return in a return to normal scenario would be approximately 4.2%. For the purposes of this analysis, the model applies consistent quarterly returns of approximately 1.04% (based on this 4.2% annual return). We refer to these as return to normal–like returns; we would not assume consistent quarterly returns in a true return to normal scenario.

Tracy Filosa - Tracy is a Managing Director and Head of CA Institute.

About Cambridge Associates

Cambridge Associates is a global investment firm with 50+ years of institutional investing experience. The firm aims to help pension plans, endowments & foundations, healthcare systems, and private clients achieve their investment goals and maximize their impact on the world. Cambridge Associates delivers a range of services, including outsourced CIO, non-discretionary portfolio management, staff extension and alternative asset class mandates. Contact us today.