Germany’s Fiscal Boost Remains a Tailwind Despite Near-Term Risks

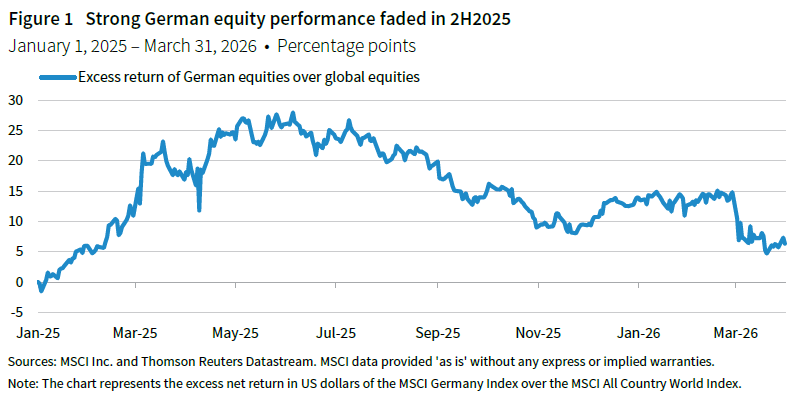

German equities entered 2025 with strong momentum, supported in part by a sharp shift in Germany’s fiscal outlook. After years of underinvestment, the government announced materially higher spending on infrastructure and defense. However, that momentum faded through 2025 into 2026, and German equities stalled (Figure 1). Slow implementation of the announced fiscal packages, limited exposure to artificial intelligence (AI)-driven market sentiment relative to the United States, intensifying manufacturing competition from China, and, more recently, the war in Iran, have all created notable headwinds. Even so, we remain constructive on Germany and, by extension, the euro area over the medium term. Subdued sentiment in the region creates upside potential, particularly since the growth impulse from fiscal stimulus should build throughout the year. While the conflict with Iran poses near-term risks, it may also reinforce the case for further fiscal expansion in Germany and greater policy coordination across the EU in the medium term. Together with still-discounted valuations, these factors support our tactical preference for global equities outside the United States over US equities.

Fiscal-driven optimism has faded

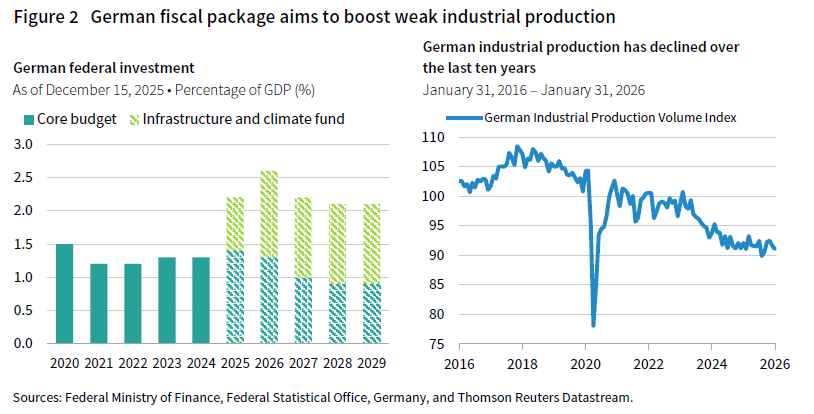

Germany unveiled an ambitious fiscal package last year. It included a special €500 billion infrastructure and climate fund to be deployed over 12 years, alongside changes to the debt brake that effectively removed constraints on defense spending. Defense spending planned for 2025–30 totals €650 billion, roughly double the level of the prior five years. If fully implemented, federal debt could rise by €850 billion by 2029, or about 19% of 2025 GDP. That would exceed the €613 billion increase recorded over 2020–24, a period that included the COVID-19 pandemic.

In many advanced economies, a package of this scale would raise concerns about debt sustainability. In Germany, the response was more constructive, in part because the country starts from a stronger fiscal position. Gross debt-to-GDP stood at ‘only’ 63%, compared with many advanced economies where the ratio is closer to, or above, 100%.

Years of conservative fiscal policy have led to significant underinvestment in key strategic sectors – including digitalisation – a diminished competitive advantage in manufacturing and eroded infrastructure (Figure 2). Substantial bureaucratic and regulatory burdens, together with elevated energy prices following the Ukraine conflict, added further headwinds. At the same time, China shifted from a consumer of German exports to a direct manufacturing competitor. The automotive industry is particularly exposed to this structural shift, as German manufacturers were slow to adapt to rising electric vehicle (EV) demand, while sectors such as chemicals and machinery also lost ground.

As a result, growth in the euro area’s largest economy stagnated (GDP growth averaged 0.1% over the last four years), while industrial production contracted by 4.4% in 2024 and a further 1.1% in 2025. The hope was that aggressive public spending would revive growth, modernise infrastructure, and restore Germany’s leadership in manufacturing and innovation.

That initial optimism faded in the second half of 2025, and German equities underperformed global peers. Although German and euro area activity showed tentative signs of improvement – including composite PMIs moving back into expansionary territory – there was limited evidence that fiscal announcements had yet lifted industrial activity. Investor attention instead shifted to the euro area’s weaker growth outlook and limited exposure to AI-driven enthusiasm relative to the United States, as well as ongoing labour market softness, including job cuts in key sectors such as automotive and chemicals.

Data also revealed central government investment spending, including infrastructure, rose slower than initially planned in 2025, rising by only 0.2% of GDP. Just 65% of the Infrastructure and Climate Fund allocated for 2025 was actually disbursed. Some delay between policy announcement and project execution was always likely. But Chancellor Friedrich Merz’s coalition, despite holding a workable majority, also faces internal tension over the balance between social spending and investment, particularly ahead of state elections in 2026. German GDP growth expectations have subsequently fell, from 1.3% to 0.9% for 2026.

Recent events in the Middle East have increased near-term risks to the outlook. Europe, along with many Asian countries, is particularly vulnerable as events unfold, as a meaningful share of their energy consumption depends on imported oil and liquefied natural gas (LNG). A prolonged conflict and persistently high energy prices expose European countries to an upwards inflationary and downwards growth shock, increasing pressure on Chancellor Merz to redirect federal spending towards cost-of-living initiatives. 1 Beyond the direct impact on consumer wallets, higher energy prices intensify balance sheet pressures on key manufacturing industries, complicating any recovery in activity.

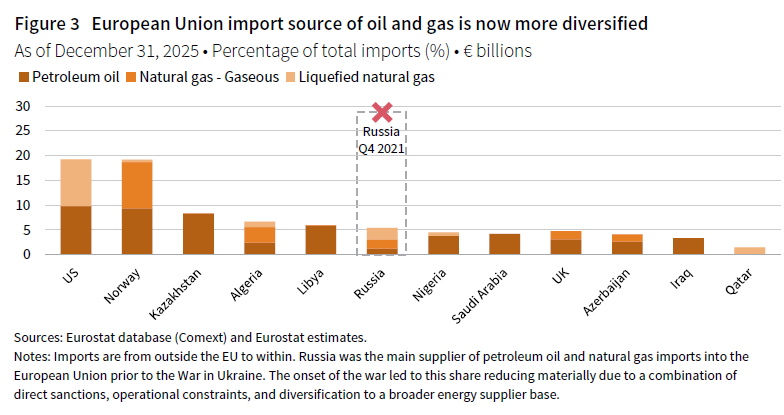

The EU is nonetheless better positioned than it was at the onset of the Russia-Ukraine conflict in 2022 (Figure 3). The energy import base is more diversified: Russia accounted for more than 25% of EU petroleum oil and natural gas imports in fourth quarter 2021, compared with roughly 10% from Persian Gulf countries in 2025. As a result, the current shock is more likely to affect Europe through higher global energy prices than through a direct disruption to physical supply. The region also enters this period with inflation closer to target, which should help cushion some of the economic fallout as the conflict unfolds.

Despite recent developments, we see reasons to be constructive over the medium term

We expect sentiment to improve over the medium term as fiscal stimulus begins to feed through more clearly. Recent data suggest that process is already under way: total federal spending in January and February was approximately 19% higher than in the same period of 2025. This increased spending is beginning to show up in economic activity. Although monthly figures are volatile, the increase in defense spending was particularly visible in December (in part due to the passage of the 2025 budget), contributing to a material upside surprise in new industrial orders – a 7.8% increase compared to consensus expectations of -2.2%. A sustained rebound in sentiment, however, likely requires a reduction in uncertainty around the economic effects of the Iran War.

The conflict, which adds to a year of rising geopolitical tensions, should also strengthen resolve to follow through on spending plans. A marked change in the United States’ relationship with other NATO member states – including reduced coordination between the United States and NATO allies on Venezuela and Iran, as well as the United States’ attempts to annex Greenland, which is a territory of Denmark – has heightened public and political calls for increased defense spending across NATO countries. Combined with the growing share of military procurement by European countries sourced from intra-European suppliers, this should benefit German defense manufacturers on a relative basis. Crises in recent years (e.g., the COVID-19 pandemic and the onset of the Russia-Ukraine war) have also been met with renewed coordination across the EU and within its member states on infrastructure investment and energy self-sufficiency. While calls to redirect infrastructure investment towards cost-of-living initiatives have grown louder, Germany’s fiscal headroom should help protect investment spending relative to other European countries.

That fiscal spending should add momentum to a euro area economy that, prior to the onset of the war, had stabilised and shown early signs of recovery following years of restrictive monetary policy and above-target inflation. The front-loading of planned German federal spending in 2026 and 2027 should support that momentum shift. According to the IMF Fiscal Monitor, the German fiscal thrust is estimated at 1% of GDP for 2026 and 0.95% for 2027 – a significant departure from nearly two decades of fiscal drag. Goldman Sachs estimates that around half of 2026 growth will be driven by fiscal stimulus, underscoring the importance of government spending in the turnaround (the economy grew 0.2% in 2025, while consensus expectations prior to the Iran War were for 1.0% growth in 2026).

A common critique of defense and infrastructure spending is that it generates a smaller long-term growth dividend compared to technology or education. But with Germany operating below potential output after years of sluggish growth, underinvestment, and labour market weakness, every euro of public spending acts as a catalyst for dormant private capital. As the government de-risks large-scale projects, we expect a ‘crowding-in’ effect, where private firms invest alongside the state. Planned reforms – including the euro area–wide ‘Draghi report’ aimed at reducing red tape, regulatory harmonisation, and capital markets integration (via the Savings and Investment Union) – should further incentivise this public-private capex recovery.

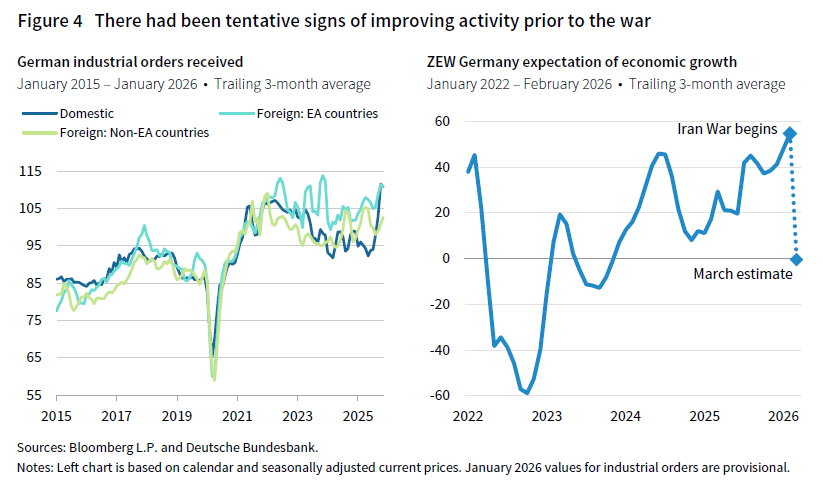

A complication for the broader euro area outlook is that other EU nations are experiencing fiscal drag. Even so, strong growth in peripheral countries such as Spain – now increasingly important buyers of German exports – should complement Germany’s fiscal impulse. Recent industrial orders data also suggest a tentative demand pickup from euro area countries alongside stronger domestic demand (Figure 4).

While large orders consistent with increased government military investment – particularly machinery, equipment, and defense goods – led the recent strong manufacturing prints, growth in new orders was also broad based. This provides encouragement for a wider economic recovery. Upside surprises in euro area economic data and German ZEW survey results to start the year suggest that growth expectations may have been turning more positive prior to the onset of the Iran War. The dissipation of US tariff-related disruption should also reduce headwinds for the region’s recovery, while the tariffs themselves have incentivised European countries to strengthen trade partnerships elsewhere, providing growth opportunities.

A more structural challenge is China’s shift from a consumer of German exports to a manufacturing competitor. We expect this trend to persist. Nevertheless, German infrastructure investment will largely focus on modernising existing infrastructure, particularly in transport. Renewed EU-wide efforts to protect businesses from increased Chinese competition and oversupply should provide relative upside potential for German business prospects if the fiscal package is fulfilled. Small- and medium-sized firms with less global presence may be better insulated from these pressures, as well as from any euro appreciation that accompanies stronger German and euro area growth.

Market impact and investment takeaways

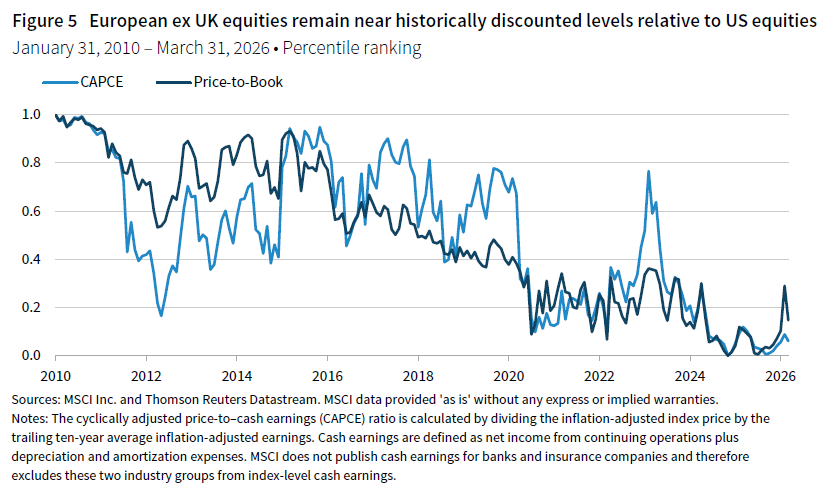

Dampened expectations in the euro area’s largest economy create the potential for positive surprises and act as a tailwind for a recovering German and euro area growth outlooks. The flow of fiscal spending through the economy is another tailwind for sentiment. These factors support our tactical preference for global equities excluding the United States, relative to US equities. Despite strong 2025 performance, Europe ex UK equities still trade near historically discounted valuations relative to US equities (Figure 5). Potential pension reforms, recently passed in parliament and commencing from January 2027, could provide additional capital injection into European equity and infrastructure investment in the medium term. 2

Developments in the Middle East are a clear risk to this outlook in the near term. However, if the Strait of Hormuz opens and Europe’s relative growth and inflation outlooks do not show further material deterioration, the trade will become even more compelling. While the situation remains fluid and uncertainty heightened, a sustained closure of the Strait of Hormuz would become increasingly economically and politically costly for all parties, intensifying pressures to restore the passage of ships in coming weeks. In that scenario, any equity market rebound is likely to be strongest in regions where valuations have been hit hardest, pointing to potential outperformance by global equities outside the United States versus US equities.

Heightened geopolitical tensions should also continue to support our view that the US dollar will remain in a downtrend over a multi-year horizon. Despite recent outperformance since the onset of the Iran War, due in part to the US status as a net oil exporter, the US dollar is down notably from its January 2025 level. US-centric geopolitical volatility adds to domestic economic policy uncertainty, overvalued assets, and concerns about fiscal sustainability, all of which dampen the attractiveness of US assets relative to elsewhere and, therefore, lower demand for the US dollar. This is an important aspect of our preference for global equities excluding the United States, relative to US equities.

Drew Boyer also contributed to this publication.

Index Disclosures

The MSCI All Country World Index (ACWI) is a benchmark tracking over 2,500 large- and mid-cap stocks across 23 developed and 24 emerging markets. Covering approximately 85% of global investable equity, it is heavily weighted toward US equities and technology.

The MSCI Germany Index is designed to measure the performance of the large- and mid-cap segments of the German market. With 54 constituents, the index covers about 85% of the equity universe in Germany.

Footnotes

- OECD forecasts for the 2026 German economic outlook show an inflation forecast change of +0.8 percentage points (to 2.9%) and GDP growth forecast change of -0.2 percentage points (to 0.8%).

- Under the plan, private pensions will become increasingly important to supplement state pensions in retirement and allow improved flexibility to investors to allocate funds to higher yielding assets. An investor could theoretically allocate 100% of their funds to equities, for example.

Max English - Max English is an Investment Director for the Capital Markets Research team at Cambridge Associates.

About Cambridge Associates

Cambridge Associates is a global investment firm with 50+ years of institutional investing experience. The firm aims to help pension plans, endowments & foundations, healthcare systems, and private clients achieve their investment goals and maximize their impact on the world. Cambridge Associates delivers a range of services, including outsourced CIO, non-discretionary portfolio management, staff extension and alternative asset class mandates. Contact us today.