US Private Families Should Revisit How Munis Fit Within a Broader Diversification Strategy

Many US private families reduced US tax-exempt municipal bond (muni) exposure in recent years as low yields, poor performance, and elevated volatility weakened the case for tax-exempt fixed income. That rationale now looks much less compelling. With yields higher and a more meaningful tax advantage of munis, tax-exempt bonds should play a larger role in the portion of the portfolio intended to diversify equity risk.

At the same time, effective portfolio construction in this segment of the portfolio should still balance tax-efficient income with broader objectives, including liquidity, downside protection, and diversified sources of return. In that context, some families with acute liquidity or spending needs may still benefit from modest exposure to cash or taxable fixed income, while selected diversifying strategies, including certain hedge fund strategies, can complement munis and support stronger after-tax portfolio resilience.

Why some US private families have soured on munis

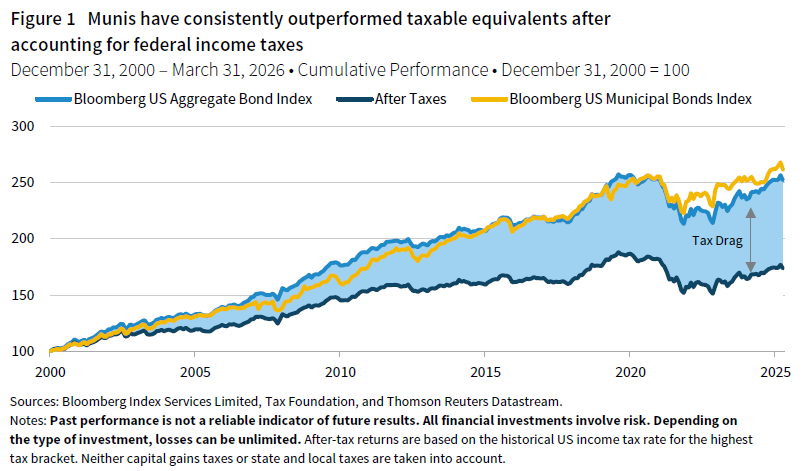

Historically, munis have delivered stronger after-tax returns than comparable taxable bonds, making them a core fixed income allocation for high-net-worth US private families (Figure 1). Most US private families have long allocated the majority, if not all, of their fixed income exposure to munis, though some have maintained modest positions in taxable alternatives such as cash, US Treasury securities, and investment-grade credit.

In recent years, however, several structural headwinds have challenged that position. Relative to larger segments of the investment-grade bond universe, particularly the US Treasury market, the muni market is smaller and less liquid, with a larger retail investor base. As a result, munis have at times been more vulnerable to liquidity squeezes and sharper bouts of volatility during periods of market stress. During the COVID-driven sell-off in early 2020, for example, some investors were forced to sell at a discount, crystallizing losses at an inopportune moment.

Meanwhile, persistently low yields in the years following the Global Financial Crisis (GFC) reduced the relative tax advantage of munis. More recently, the sharp rise in bond yields and the return of positive stock-bond correlations weakened fixed income performance more broadly and reduced its effectiveness as a diversifier. Together, these developments made it understandable that some families reduced their overall fixed income exposure and shifted a portion of their remaining allocations away from munis.

Cambridge Associates’ data suggest this shift has been meaningful. The median US private family client held nearly 90% of fixed income and cash assets in munis in 2015; by 2025, that figure had fallen to below 70%.

Why munis are regaining their edge

With the benefit of hindsight, reducing muni exposure was a defensible decision. The past five years were unusually challenging for munis, with low starting yields, rising interest rates, and elevated volatility weighing on returns. Over this period, munis returned 0.8%, significantly outperforming Treasuries at -1.8% but trailing cash at 1.8% after taxes, despite considerably higher volatility. Some alternative strategies, including certain hedge funds, also delivered stronger after-tax outcomes. The subset of hedge funds we view as most investable outperformed munis by nearly 400 basis points (bps) per year after taxes and net of fees.

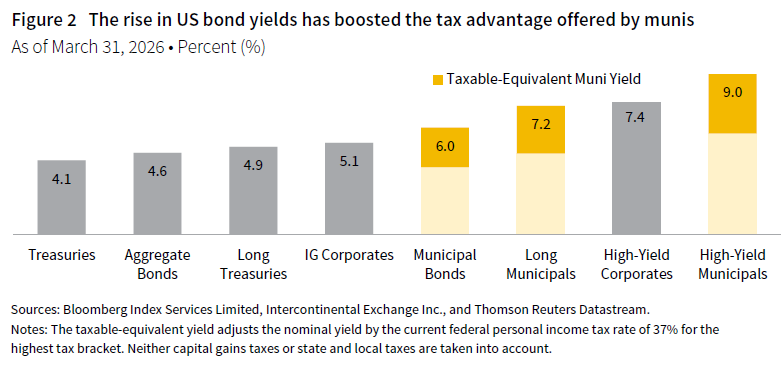

Today, the environment is more favorable. Higher yields have improved return prospects across fixed income and provide a larger cushion against future volatility than investors had in recent years. They have also significantly increased the tax advantage of munis. As yields rise, the value of the tax exemption increases, resulting in greater tax savings for US private families in high tax brackets (Figure 2).

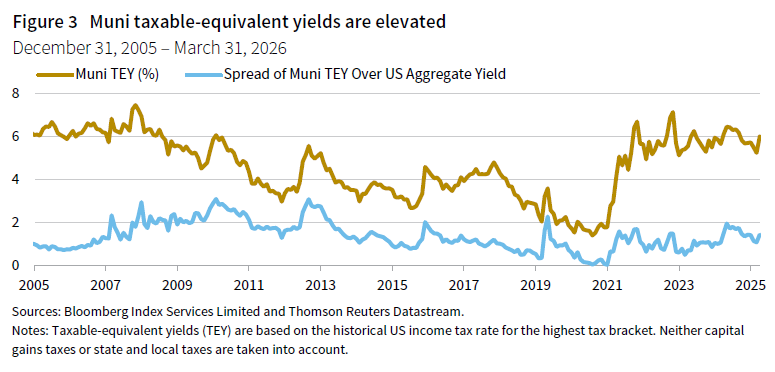

The Bloomberg Municipal Bond Index currently yields 3.8%, translating to a taxable-equivalent yield (TEY) of 6.0% for top-bracket US private families, which are well above levels seen for most of the past decade and higher than comparable taxable bonds. On a pre-tax basis, muni yields may not appear especially compelling relative to taxable bonds by historical standards. After adjusting for taxes, however, the value proposition improves. The TEY spread versus the Bloomberg Aggregate Bond Index is currently 140 bps, in the 85th percentile of the past ten years (Figure 3). Historically, higher TEY spreads have been associated with stronger after-tax excess returns for munis.

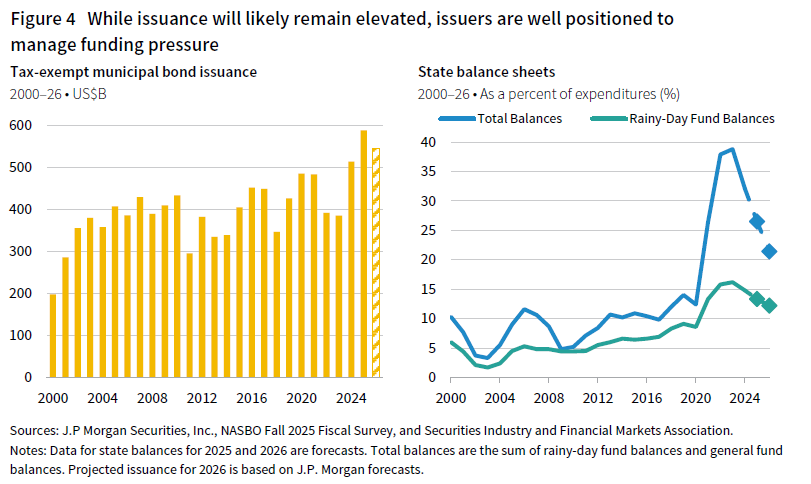

These elevated TEY spreads come even as sector credit fundamentals remain strong. State and local governments maintain healthy balance sheets, revenues continue to outpace expenditures, rainy-day fund balances are near record highs, and public pension funding ratios have improved for a third consecutive year (Figure 4). The expiration of COVID-era federal support and new federal policy changes present emerging headwinds, particularly for sectors such as hospitals and higher education. Even so, the broader municipal credit backdrop remains solid.

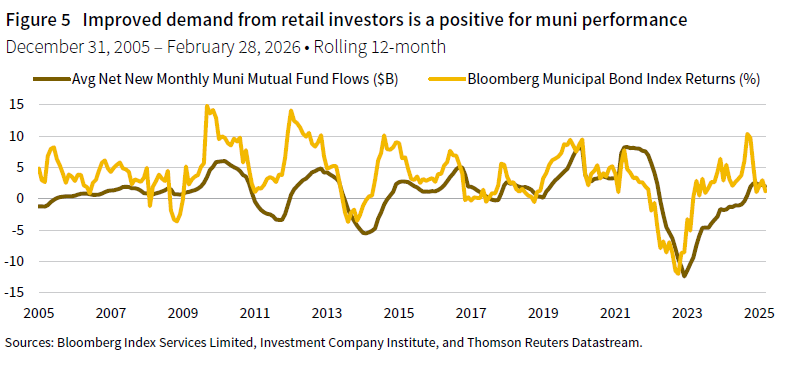

Reduced federal support is also contributing to higher issuance, and supply is likely to remain elevated as municipalities continue to fund capital needs. Attractive after-tax yields, sound fundamentals, and a healthy macro backdrop should nevertheless support healthy retail demand. Inflows into muni separately managed accounts (SMAs), mutual funds, and exchange-traded funds (ETFs) accelerated in 2025, and the market appears well positioned to absorb additional supply (Figure 5).

Recent events provide an early test of that thesis. The Iran War has weighed on risk assets and pressured fixed income, echoing some of the dynamics seen in 2022, albeit on a smaller scale. So far, munis have held up relatively well compared to Treasury securities. While near-term risks remain elevated, the medium-term case for munis to play a larger role in after-tax portfolio resilience remains intact.

How munis fit within a broader diversification strategy

Munis should remain the core holding for US private families within the portion of the portfolio intended to diversify equity risk. With yields higher and the tax advantage of munis more meaningful again, the case for allocating more to less tax-efficient alternatives has weakened. While those assets can still play narrower complementary roles in some cases, the tax cost of holding them should carry greater weight in portfolio construction than it did in recent years. For those that reduced muni exposure, the case for rebuilding it has become materially stronger.

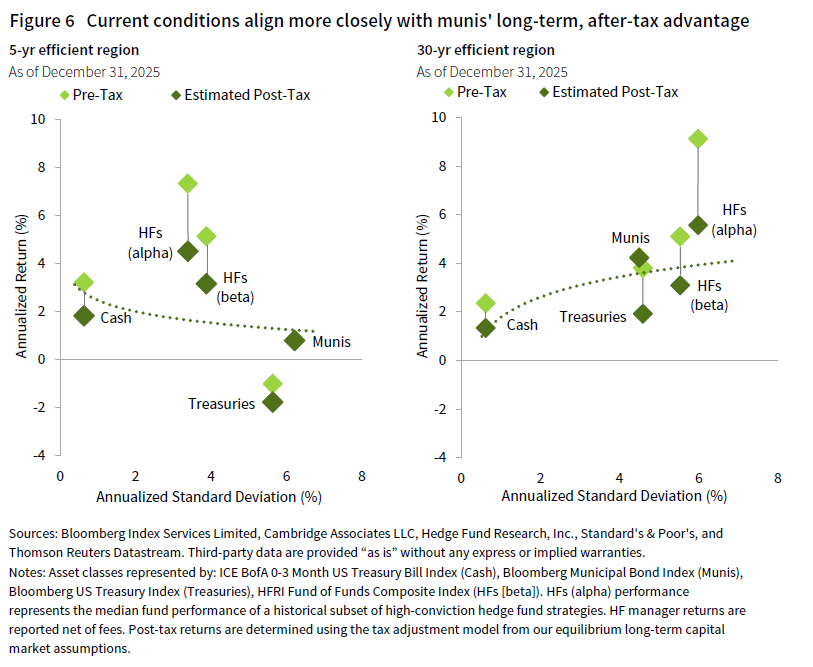

Figure 6 compares munis with a range of less tax-efficient alternatives, including US cash, US Treasury securities, and hedge funds. It plots volatility on the x-axis and both pre- and after-tax returns on the y-axis over the past five and 30 years to show how the return, risk, and tax trade-offs among these assets have shifted over time. Over the past five years, the tax cost of moving away from munis was not especially meaningful in the context of the broader return and risk environment: cash and many hedge fund strategies held up better after taxes, while US Treasury securities performed worse than munis even on a pre-tax basis. However, that period appears more unusual than representative. Over the past 30 years, munis delivered approximately 4.2% after taxes, outperforming cash at 1.3%, Treasuries at 1.9%, and even a broad hedge fund index at 3.1%, while doing so with much lower volatility than hedge funds. The key exception is a carefully selected group of hedge fund managers capable of generating persistent after-tax alpha. The median performance of the subset of hedge funds we view as most investable has exceeded muni returns by 135 bps per year after taxes over the past 30 years, net of fees.

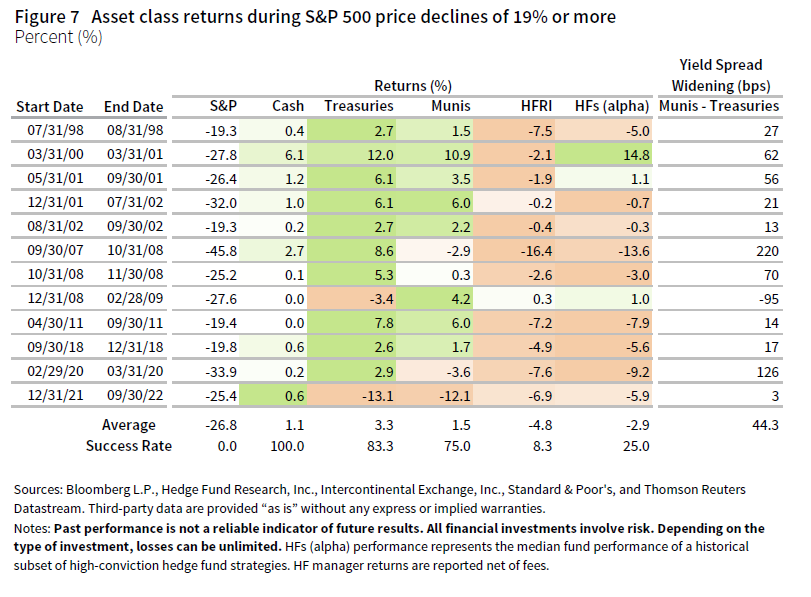

Taken together, this analysis suggests US private families should maintain a higher bar for shifting too much away from munis, given higher-than-expected after-tax returns prospects. This does not mean less tax-efficient alternatives no longer have a role. Cash, Treasuries, and other high-quality taxable bonds may still be appropriate for some US private families with near-term liquidity or spending needs, particularly because cash and Treasuries have been more resilient in some periods of market stress (Figure 7). But periods when munis underperform Treasuries have typically been relatively modest and/or brief, with the notable exception of the GFC, and US private families should not underestimate the cumulative tax drag of holding those assets over time. In many cases, a leaner cash position paired with access to a line of credit may offer a more tax-efficient way to preserve flexibility while maintaining meaningful muni exposure.

Selected hedge fund strategies have a stronger case than other less tax-efficient alternatives because they can provide differentiated return streams and, in some environments, greater resilience when traditional fixed income is under pressure, as seen in 2022 and in more recent, less severe equity market corrections. Even so, the hurdle remains high: these strategies should complement, rather than replace, meaningful muni exposure and are most compelling when implemented through carefully selected managers with a demonstrated ability to generate persistent after-tax alpha. 1 This aligns with our previous advice to build exposure across a range of diversifier strategies—a principle that remains relevant, since no single strategy performs well across all environments.

Conclusion

We believe US private families should continue to anchor the portion of the portfolio intended to diversify equity risk with munis, while being more selective about allocations to cash, Treasuries, and other taxable fixed income, given the shift in after-tax trade-offs. Selected hedge fund strategies also remain an attractive complement to fixed income today, particularly when accessed through managers with a demonstrated ability to generate persistent after-tax alpha. For US private families that have drifted away from munis in recent years, the after-tax math has shifted decisively back in their favor. Now is the time to reassess and, in many cases, rebuild exposure.

Drew Boyer also contributed to this publication.

The Bloomberg US Aggregate Bond Index is a broad-based benchmark that measures the performance of the US investment-grade, taxable bond market. The index includes securities such as US Treasuries, government-related and corporate bonds, mortgage-backed securities, asset-backed securities, and commercial mortgage-backed securities that meet specified maturity, liquidity, and quality requirements.

The Bloomberg US Municipal Bond Index measures the performance of the US dollar-denominated, long-term, tax-exempt bond market. The index is designed to cover the investment-grade US municipal bond market and includes municipal bonds that meet specified maturity, liquidity, and quality requirements.

The Bloomberg US Treasury Index measures the performance of US dollar-denominated, fixed-rate, nominal debt issued by the US Treasury. The index includes public obligations of the US Treasury with remaining maturities that meet specified index requirements. Index returns do not reflect deduction of fees, expenses, or transaction costs.

The HFRI Fund of Funds Composite Index is a global, equal-weighted index designed to reflect the performance of funds of hedge funds. The index includes fund of funds managers that invest with multiple underlying hedge fund managers and report returns to HFR Database. The index is intended to provide a broad measure of the fund of funds segment of the hedge fund universe.

The ICE BofA 0-3 Month US Treasury Bill Index tracks the performance of US dollar-denominated Treasury bills publicly issued by the US government in its domestic market with remaining maturities of less than three months. The index is intended to measure short-term US government bill performance.

The S&P 500 Index is an unmanaged, market capitalization–weighted index consisting of 500 leading publicly traded US companies. The index is designed to measure the performance of the large-cap segment of the US equity market.

Footnotes

TJ Scavone - T.J. is a Senior Investment Director in the Capital Markets Research Group at Cambridge Associates.

Katherine Armstrong - Katherine Armstrong is a Managing Director for the Private Client Practice at Cambridge Associates, a global investment firm.

About Cambridge Associates

Cambridge Associates is a global investment firm with 50+ years of institutional investing experience. The firm aims to help pension plans, endowments & foundations, healthcare systems, and private clients achieve their investment goals and maximize their impact on the world. Cambridge Associates delivers a range of services, including outsourced CIO, non-discretionary portfolio management, staff extension and alternative asset class mandates. Contact us today.