A New Era of Dispersion in Direct Lending Favors Disciplined Managers

Direct lending has attracted significant institutional capital over the past decade, with investors drawn to its attractive yields, floating-rate nature, and senior-secured position. This growth unfolded against a benign backdrop of limited credit stress, helping the asset class generate strong, stable returns but obscuring meaningful differences in manager skill. This narrow performance dispersion remained even as assets under management (AUM) surged and new entrants proliferated.

That environment is now changing. Weakening underwriting standards, retail vehicle growth, and technological disruption are creating a more challenging landscape. Given these changes, we expect performance dispersion to emerge more clearly between managers that remained disciplined throughout these heady times and those that did not. This widening range of outcomes reinforces the importance of manager selection and taking a diversified approach across strategies, geographies, and borrower segments.

How we got here

Since the Global Financial Crisis, banks have steadily retreated from many traditional lending markets, creating an opportunity for private lenders. Over the past five years alone this trend accelerated, with US direct lending AUM roughly doubling to $1.3 trillion. Retail-oriented vehicles like interval funds and business development companies (BDCs) have played a key role in this recent expansion, with BDC assets alone now totaling more than $500 billion.

The rapid growth of assets, particularly via semi-liquid funds, has coincided with a slower merger & acquisition (M&A) environment, leaving more capital competing for fewer deals. The result has been intensified competition among direct lenders and a borrower-friendly market characterized by spread compression, weaker underwriting standards, and looser lender protections across the upper, core, and lower middle market.

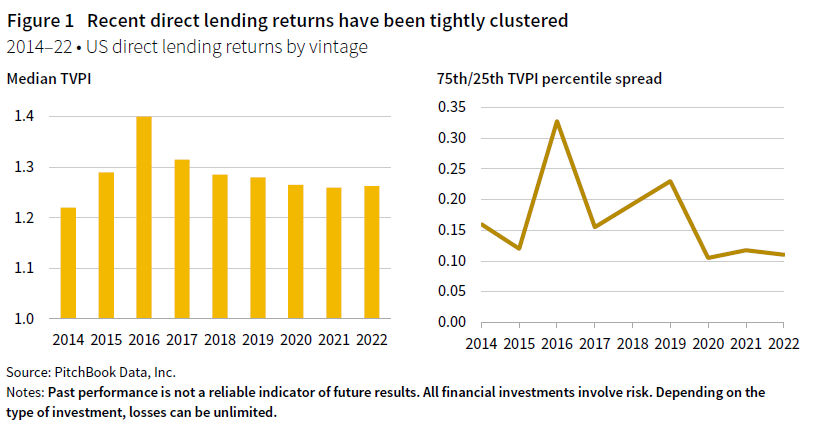

Meanwhile, the benign credit environment that prevailed for much of the past decade—marked by historically low default rates—masked differences in manager quality. Because direct lending returns are highly asymmetric and driven largely by loss avoidance and recoveries, weak underwriting or limited workout experience often did not show up in returns. As a result, the gap in total value to paid-in (TVPI) between top- and bottom-quartile managers narrowed to just 0.1x, understating the true dispersion in underlying portfolio quality (Figure 1).

Making sense of the negative headlines

Since late 2025, the press has highlighted valid risks in private credit, but the coverage often exaggerates the extent and, thus, vulnerability.

Retail vehicles and asset-liability mismatch

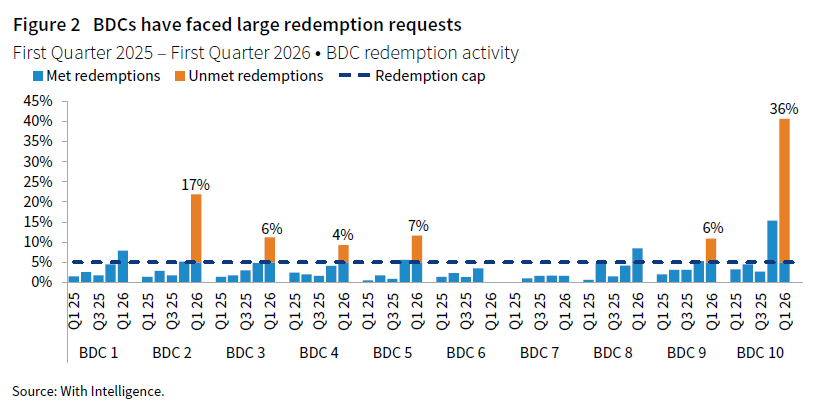

Retail-targeted vehicles offering limited quarterly liquidity have created a mismatch between investor liquidity expectation and the illiquid, five- to seven-year nature of the underlying loans. Private BDCs manage this tension by capping quarterly redemptions at 5% of net asset value through discretionary tender offers, but recent increases in withdrawal requests have led some managers to activate these gates, weighing on sentiment (Figure 2). This reaction, however, appears partly driven by investor (and perhaps media) misunderstanding of the fund structure and its intended liquidity profile.

Gating can protect investors by preventing fire sales or the selective liquidation of high-quality assets that would disadvantage remaining investors. This risk is amplified by the use of leverage in BDCs, as deleveraging can generate further pressure on asset prices. Managers with healthier loan portfolios and sophisticated liability management are better positioned to manage through these pressures. In contrast, managers facing sustained redemption pressures, credit deterioration, and weaker liability management may be left holding more stressed or illiquid assets, increasing the risk of losses.

Institutional investors in longer-duration, lock-up vehicles are not directly exposed to these dynamics. Near-term spillover from retail outflows may affect deal flow and slow deployment, but the longer-term implications could be constructive. If redemption pressure persists, the supply/demand dynamic may become more balanced, positioning managers with stable capital bases to deploy into opportunities with wider spreads and stronger lender protections.

Weakening underwriting standards

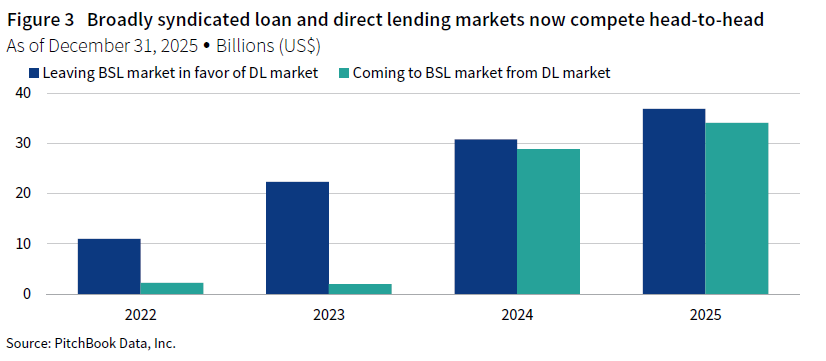

An oversupply of capital relative to deal opportunities has pressured direct lending, compressing yields and weakening underwriting standards and lender protections. This has been most evident in the US upper middle market, where large publicly traded asset managers have concentrated their retail-oriented vehicles. This segment began to attract a disproportionate amount of direct lending AUM in 2022, when Federal Reserve rate hikes and recession fears dislocated public loan markets and created attractive pricing for direct lenders. However, once the broadly syndicated loan market reopened, the direct lenders in the upper middle market began competing directly with the public markets (Figure 3).

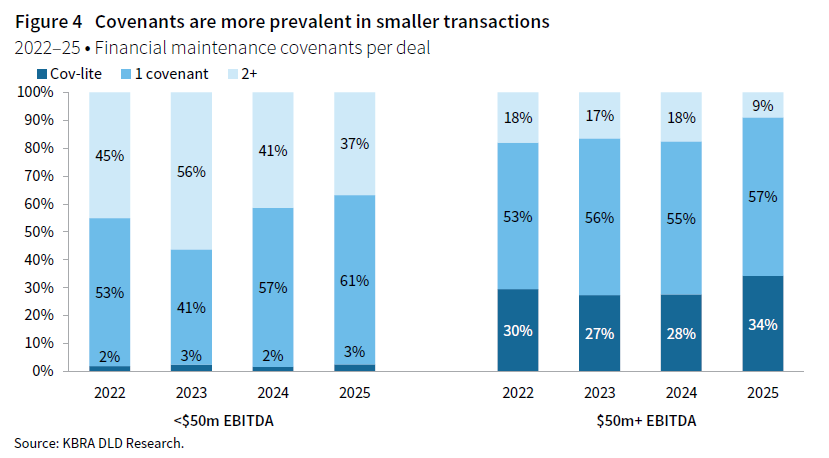

That competitive overlap has weakened deal terms. To compete with the broadly syndicated loan market, the upper middle market has long accepted the absence of financial maintenance covenants. Competitive pressures have also weakened lender protections in parts of the core middle market, including fewer maintenance covenants and looser documentation in some transactions. Even where covenants remain, aggressive EBITDA adjustments, unrealistic financial projections, and loose definitions often weaken them and create a false sense of protection (Figure 4). By contrast, lower middle market and specialty lenders—which typically serve more complex borrowers—have largely maintained covenant discipline.

The supply/demand imbalance in the market has put newer and less-established entrants at a disadvantage. Managers with established sponsor and borrower relationships have greater access to repeat financing opportunities, while less-established entrants are more likely to compete in broadly marketed transactions where documentation and pricing discipline were weaker. In a strong economy with low interest rates, these underwriting decisions may matter less, but if rates stay persistently high or the economy slows down, these managers are likely to face elevated portfolio stress.

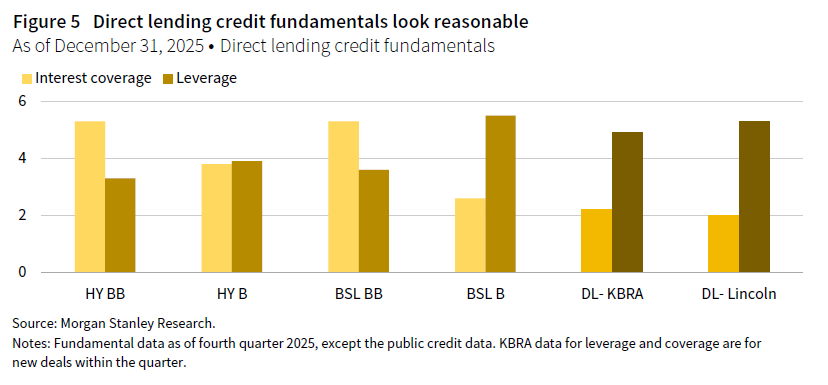

Early signs of stratification are already visible. While average metrics for the direct lending universe such as interest coverage ratios and non-accrual rates appear stable, the tail of weaker portfolios is growing (Figure 5). For example, 11% of public BDCs receive more than 10% of total investment income in payment-in-kind (PIK), while the average BDC receives only 6% of income in PIK.

Software exposure and AI disruption

Technology-related deals, and software in particular, have dominated leveraged buyout (LBO) activity over the past decade. Direct lenders have financed a significant share of these transactions, often at elevated valuations and leverage levels. On average, direct lenders carry approximately 20% exposure to the software sector, much of it originated during an era of low interest rates and optimistic growth assumptions. Additionally, a notable subset of software loans consists of annual recurring revenue loans: financing extended to companies with recurring revenue but little or no positive free cash flow. As these loans approach maturity, borrowers face a more difficult exit environment, marked by compressed valuations and tighter financial conditions, which raises refinancing and repayment risk.

Artificial intelligence (AI) poses two primary risks to software companies: obsolescence risk, as customers build proprietary solutions in-house, and margin compression, as lower-cost competitors erode pricing power and force incumbents into defensive investment. Companies with proprietary data, embedded workflows, and regulatory moats are better insulated, and some incumbents may benefit by successfully integrating AI into their products. Nevertheless, the full effects of AI disruption will take time to emerge, and uncertainty itself warrants caution.

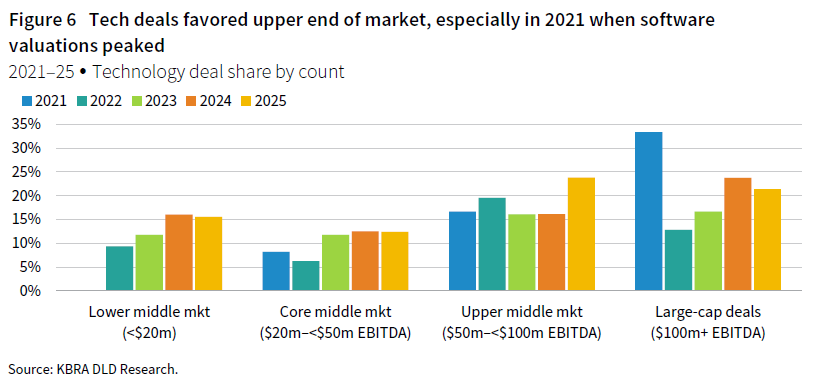

Most software deal flow in direct lending has been concentrated in the upper middle market, precisely where aggressive lending practices and weaker protections are most prevalent (Figure 6). As a result, private software loans carry, on average, more than a full additional turn of leverage relative to other major direct lending sectors and exhibit lower interest coverage ratios. These metrics are often measured against adjusted EBITDA figures, which further overstate borrower resilience and understate underlying liquidity risk. In this environment, direct lenders that have emphasized strong creditor protections and disciplined deal structures appear best positioned. These features provide managers with greater control and flexibility, enabling earlier intervention when signs of stress arise. In addition, many of these managers have maintained lower software exposure than the broader direct lending market, reflecting a disciplined avoidance of the most competitive deals. Some borrowers may be forced into expensive capital solutions, disadvantaging equity and remaining credit investors.

Expect wider dispersion

The era of uniformly strong, low-dispersion direct lending returns is ending. Weaker underwriting in parts of the market, retail vehicle stress, and AI-driven uncertainty in software are converging to create a more challenging environment. Going forward, we believe outcomes will depend more on manager quality, documentation discipline, and sector selectivity than on market exposure alone. Investors should expect a wider gap between top- and bottom-quartile performance, making manager selection more consequential than at any point in the asset class’s recent history.

As previously noted, we continue to favor strategies like lower middle market and specialty lending. These segments remain less crowded and, in our view, better positioned to hold up in a tougher environment. We believe manager outcomes will increasingly depend on their ability to:

- Target less competitive market segments. In the United States, crowding in the core and upper middle market has compressed spreads and weakened lender protections, we believe making the less-trafficked lower middle market more attractive on a risk-adjusted basis. Managers with strong sourcing capability and the ability to underwrite complexity are likely to be rewarded, including specialty lenders that focus on non-sponsored borrowers, companies in transition, and out-of-favor sectors.

- Demonstrate disciplined underwriting and experienced workout capabilities. In a more challenging environment, capital preservation will depend on proactive portfolio management, early identification of stress, and the ability to maximize recoveries when credits deteriorate. In our experience, these capabilities are often, though not exclusively, associated with larger, more experienced managers that have invested through prior credit cycles.

While the focus of this paper has been on the US market, we’d note that the market structure in Europe is generally more favorable for direct lending investors. European direct lending remains less crowded and more disciplined, and it has not seen the same growth in retail-oriented vehicles that has fueled the excess capital, spread compression, and underwriting deterioration in parts of the US market.

Conclusion

After a decade of strong and stable returns, the direct lending market is entering a more demanding phase. Compressed spreads, weaker underwriting in parts of the market, retail vehicle pressures, and AI-driven disruption in software are collectively widening the gap between managers that remain thoughtful and disciplined, and those that do not. Investors who prioritize underwriting discipline, creditor protections, capital preservation, and thoughtful portfolio construction—including diversification across managers, geographies, and borrower segments—will be best positioned for what lies ahead.

Graham Landrith also contributed to this publication.

About Cambridge Associates

Cambridge Associates is a global investment firm with 50+ years of institutional investing experience. The firm aims to help pension plans, endowments & foundations, healthcare systems, and private clients achieve their investment goals and maximize their impact on the world. Cambridge Associates delivers a range of services, including outsourced CIO, non-discretionary portfolio management, staff extension and alternative asset class mandates. Contact us today.