Endowment Spending to the Rescue?

The current health crisis is creating extraordinary financial disruptions for nonprofit enterprises, leading stakeholders to ask if the endowment can come to the rescue of revenue shortfalls and often growing costs. How should an institution evaluate this, and what are the long-term implications of boosting spending beyond policy levels? First, we consider whether it is possible and prudent to spend more, given endowment restrictions and the risk that higher spending will compromise long-term purchasing power. Second, we consider the timing and the extent of an institution’s heightened reliance on the endowment, to evaluate the ongoing implications of higher spending. Finally, we consider the role of the endowment in the enterprise to provide further context of the impact of higher spending. While institutional needs and resources are far from uniform, each must tread carefully and evaluate thoughtfully before making short-term spending decisions that will impact the institution forever.

Can We Spend More from the Endowment?

The first question an institution must ask is if there is flexibility to spend from the endowment at a level that will erode the value of the portfolio. While we use the term endowment to describe all kinds of long-term investments, the funds in the portfolio are not all the same. There are three types of funds that may reside in the long-term investment portfolio (LTIP):

- Donor-restricted endowment funds that have been given to the institution with the understanding and commitment that those funds will be stewarded to fund their designated purpose (e.g., a scholarship or faculty salary) in perpetuity

- Board-designated, or unrestricted, endowment funds that have been set aside by the governing board, rather than a donor

- Long-term reserve funds that may be invested for long-term support of the institution

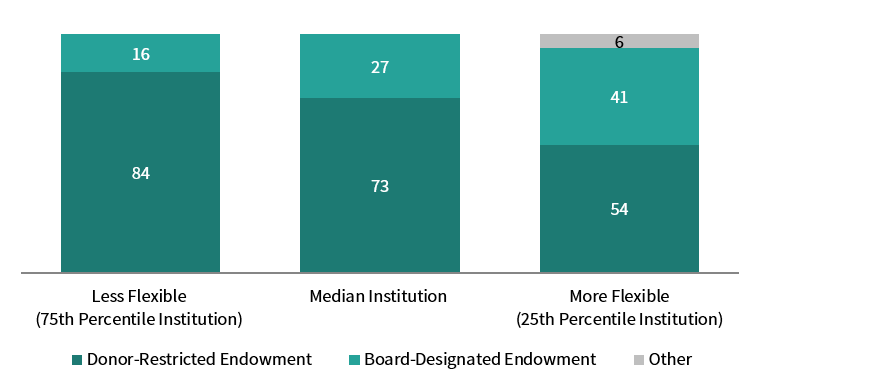

Most assets in the LTIP are permanent endowment funds that support the institution in perpetuity and most of those permanent funds are donor-restricted endowments. Figure 1 portrays three different levels of LTIP flexibility of the Cambridge Associates endowment universe. The median institution has an LTIP that is composed of 73% donor-restricted endowment and 27% board-designated endowment. All of the assets in that portfolio are endowed for the long-term support of the institution, and the majority are donor-restricted. The LTIP representing the 75th percentile has less flexibility because 84% of the portfolio is donor-restricted funds. This endowment must avoid spending beyond policy because higher spending would reduce the purchasing power of the funds the donor has restricted for perpetual support and introduces a risk of breaching the commitment to the donor. By contrast, the upper quartile institution has a more flexible endowment that, in addition to donor-restricted funds, is also composed of board-designated endowment and some long-term reserve funds. While all the funds in the 25th percentile portfolio have also been set aside to provide long-term support to the institution, the institution may repurpose the long-term reserves and, perhaps, board-designated funds in the portfolio if near-term spending needs are prioritized over long-term support.

FIGURE 1 LEVEL OF RESTRICTED FUNDS IMPACTS INSTITUTIONS’ SPENDING FLEXIBILITY

As of June 30, 2019 • Percent (%)

Source: Cambridge Associates LLC.

Note: This chart is based on a cohort of 122 long-term investment portfolios ranging from $23 million to $20 billion in assets.

Endowment assets have primarily been restricted by donors, but also by institutional leaders planning for the long-term financial health of the institution. Of course, financial emergencies, such as those wrought by the COVID-19 pandemic, can override long-term plans with immediate needs. Nonetheless, fiduciaries are legally bound to honor donor restrictions, and Board-designated endowment can only be repurposed by an overriding board decision.

What are the implications of spending more?

The financial impact of higher spending depends on the level and the duration of elevated expenditures, as well as the investment performance that accompanies the spending.

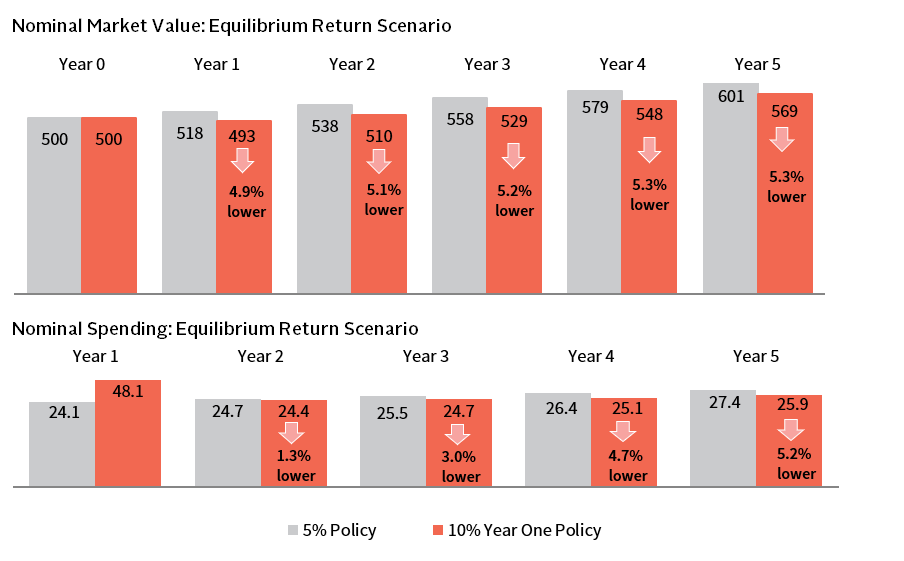

The following case study examines a $500 million endowment that has a one-time higher spending event, spending 10% in one year, effectively twice the typical 5% target spending. We evaluate the financial implications of that decision in two different investment environments: an equilibrium environment where strong investment returns contribute to portfolio growth and a U-shaped market environment where higher spending happens at the same time as negative returns. 1

In a robust equilibrium-return environment, the higher spending scenario results in a lower ending market value compared to the scenario that adheres to policy, but the loss in market value is temporary (Figure 2). After one year, market value is restored and exceeds the starting value, because investment returns outpace cumulative spending. In the equilibrium-return environment, the higher spending portfolio still grows 14% over the five-year period.

FIGURE 2 PURCHASING POWER OF HIGHER SPENDING PORTFOLIO TRAILS, BUT RECOVERS IN A STRONG

RETURN ENVIRONMENT

US Dollar (millions)

Source: Cambridge Associates LLC.

Spending policy will generate higher spending each year in a strong return environment, even if the institution spends 10% in Year One. By Year Five, spending in the higher spending scenario falls 5% behind the policy spend, but has grown 7.4% from the initial spending policy amount of $24 in Year One (compared to 13.8% spending growth for the portfolio that adhered to spending policy over that timeframe).

The impact of spending more from a perpetual pool of capital is itself perpetual. Spending an additional 5% today, as in the example above, will decrease market value by approximately 5% compared to spending based on policy, and this 5% gap will persist over time. Most endowments incorporate market value into the spending policy calculation; therefore, this gap will persistently reduce spending distributions. The most common spending policy takes a percentage of the trailing 12-quarter average market value, as used in this example. Under this type of policy, the effects of the market value decline will gradually phase in until the full trailing period incorporates the lower market value, and thus spending is approximately 5% lower in the fourth year and thereafter. The precise difference in market value and spending will depend on the amount of overspending and on market conditions during and after spending. However, controlling for these factors, an institution can expect any overspending by a given percentage to decrease market value and spending by that same percentage, and for that decline to continue over the long term.

What if Higher Spending is Accompanied by Negative Returns?

The implications of higher spending are more severe in a negative market environment. When we consider U-shaped investment scenario, higher spending is synchronous with a negative investment return, so the market value loss is more severe than an equilibrium environment and recovery takes longer (Figure 3). If the institution had maintained its 5% spending policy in Year One, spending would have declined 4.9% from the starting point from the negative return environment, while the higher spend scenario is 10.3% lower than the starting spending policy distribution and 5.7% less than the scenario that adhered to spending policy.

FIGURE 3 A NEGATIVE RETURN ENVIRONMENT EXACERBATES THE IMPACT OF HIGHER SPENDING

US Dollar (millions)

Source: Cambridge Associates LLC.

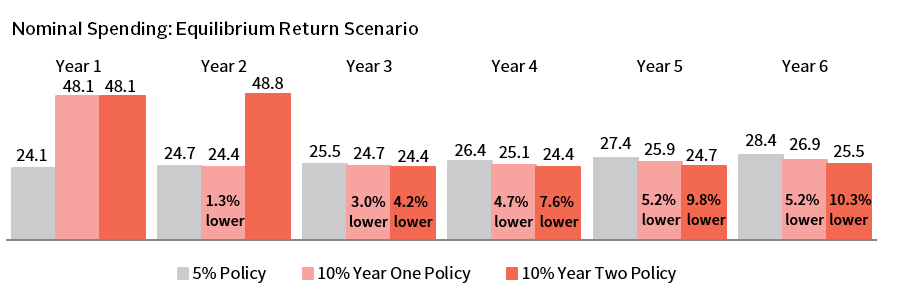

What if Higher Spending Continues for Multiple Years?

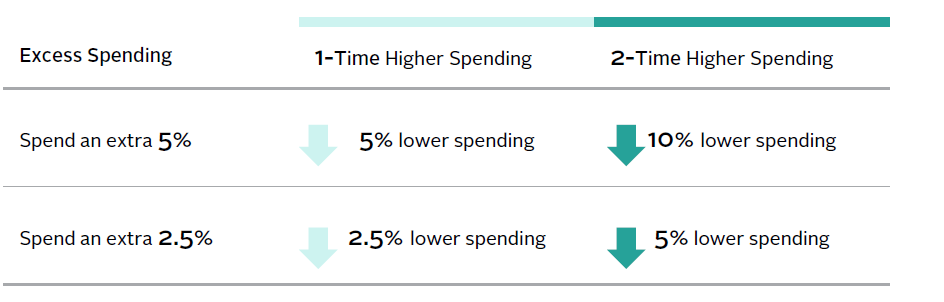

Spending more from endowment in the present results in lower future spending than what would have otherwise been available. Over time, that 5% increase in spending results in a corresponding 5% drop in annual spending. If the higher spending level persists for two years, it will result in an additional 10% outflow that will ultimately result in 10% lower spend in future years. The institution benefited from the infusion of funding for two years, but future budgets must be balanced with the lower spending generated by the depleted portfolio, even in an equilibrium return scenario (Figure 4). The math is simple and stark once the full impact of overspending has been fully incorporated into the spending rule calculation (Figure 5).

FIGURE 4 PROLONGED HIGHER SPENDING FURTHER ERODES LONG-TERM PURCHASING POWER

US Dollar (millions)

Source: Cambridge Associates LLC.

FIGURE 5 INSTITUTIONS THAT SPEND MORE NOW WILL NEED TO MANAGE WITH LESS SUPPORT FOR FUTURE BUDGETS

Source: Cambridge Associates LLC.

How will Higher Spending Impact the Budget?

While this crisis may force institutions to boost endowment spending, they must understand the resulting budgetary impact of depleted future spending. As shown in Figure 6, an institution that is more endowment-dependent will have a larger gap in future budgets if they choose to spend more today.

FIGURE 6 INSTITUTIONS WITH THE HIGHEST RELIANCE ON ENDOWMENT FUNDS EXPERIENCE GREATEST DECLINES IN BUDGET FUNDING

Percent (%)

Source: Cambridge Associates LLC.

Continuing with our case study, if the spending from the $500 million endowment provides 10% of funding for a $250 million budget, then a 10% decline in future spending will represent a 1% cut in the overall budget (or the funding will need to be replaced by another funding source). If the institution is highly reliant on the endowment and it is supporting 50% of a $50 million budget, then the 10% decline would result in a 5% decline in budget funding and have a greater impact on the enterprise.

Conclusion

When an institution needs additional cash, turning to the endowment is one option, but the opportunity cost of drawing down long-term capital is very expensive—that capital is no longer earning returns or supporting future spending. While many institutions have good reasons to rely on the endowment more heavily in a financial emergency, they may prefer to turn to short-term or long-term reserves, if they are available. Or they may turn to the liability side of the balance sheet and draw on a line of credit or issue long-term debt. The endowment has an important role in supporting borrowing, providing ballast to the balance sheet, contributing to a strong credit rating, and less costly borrowing.

It is not easy to offset revenue losses and fund expenses when the enterprise faces extensive and prolonged disruptions. A financial emergency brings difficult decisions and tradeoffs. One-time, slight increases in spending will not have significant long-term implications, especially for an institution that is not very reliant on the endowment. Higher, multi-year spending can erode an endowment’s purchasing power and leave large budget gaps in the future. Institutional stakeholders should evaluate options in the hopes of using capital effectively in the near term and then returning to long-term financial health and sustainability.

Footnotes

- Spending policy is 5% of the trailing 12-quarter average market value. In a 10% spending scenario, a 10% spending rate is applied to the 12-quarter average market value for fiscal year 2021 spending and reverts to 5% policy thereafter. Investment returns are based on a 70/30 US Equities/US Treasuries portfolio, rebalanced annually. The equilibrium scenarios use CA’s Long-Term return assumptions, which result in an 8.8% annual return for the 70/30. The U-Shaped scenario is based on the average of 3 historical market downturns and recoveries that took a similar shape over three years, resulting in the following fiscal year returns for a 70/30 portfolio: -12.6%, 13.8%, and 8.6% for the final two years of modeling returns revert to equilibrium.

About Cambridge Associates

Cambridge Associates is a global investment firm with 50+ years of institutional investing experience. The firm aims to help pension plans, endowments & foundations, healthcare systems, and private clients achieve their investment goals and maximize their impact on the world. Cambridge Associates delivers a range of services, including outsourced CIO, non-discretionary portfolio management, staff extension and alternative asset class mandates. Contact us today.