Mission Critical: Maximizing the Impact of Healthcare System Investments

The past few decades have been generally favorable for healthcare systems; inexpensive debt, solid revenue growth, and consolidation have fueled the accumulation of sizable capital pools. Historically, many healthcare systems have treated these pools as protective reserves, investing more conservatively than endowments and foundations that rely on their portfolios for operational support. However, as pressures mount in the healthcare industry, capital accumulations will likely slow and may ultimately reverse, with many healthcare systems being forced to rely on spending from reserves to support operations. In such an environment, strong investment returns will become critical to the success of a healthcare system’s mission.

An investment approach that embraces a higher equity orientation and greater illiquidity, known as the “Endowment Model,” can be a powerful return generator for healthcare systems. But such an approach introduces risks that need to be managed and aligned with the enterprise. This paper examines the robust cash flows that have strengthened healthcare system balance sheets in recent years, and mounting industry pressures that will likely threaten those flows in the future. We then explore how to calibrate a healthcare system’s investment strategy to enterprise dynamics, and how to implement a customized investment strategy that can position the healthcare system for continued success in a challenging environment.

Video Overview:

The authors of Mission Critical share their thoughts on healthcare investing

Capital Accumulation

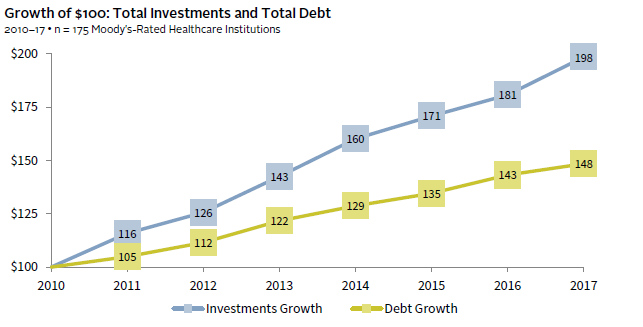

Healthcare systems deliver essential services and research to improve the quality of life in their communities. As they manage interactions with their patients, employees, physicians, payers, and donors, healthcare systems also rely on multiple capital pools that directly impact their financial health and growth. In aggregate, they have indeed become stronger financially in recent years. Since 2010, investment asset growth has increasingly outpaced additions to debt, fortifying healthcare system balance sheets (Figure 1). The deceleration of new borrowing and favorable interest rates have also benefited healthcare systems by controlling interest expense.

FIGURE 1 ACCELERATING ASSET GROWTH

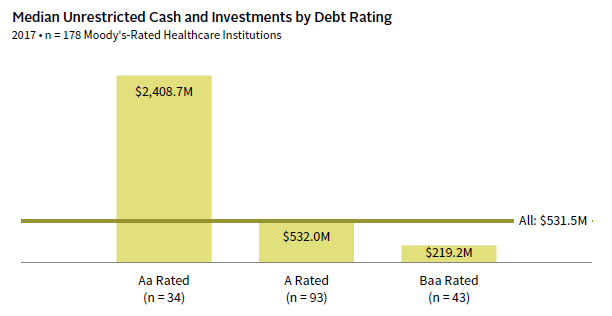

This asset accumulation dynamic creates a positive feedback loop: the more capital a healthcare system amasses—and therefore the lower its need to issue debt—the stronger its debt rating becomes. The size, liquidity, and flexibility of assets are important factors in supporting a healthcare system’s debt rating, which in turn influences the cost of debt and the capacity of an organization to deploy debt as a lever for strategic or operational reasons. The 34 Aa-rated healthcare entities in Moody’s 2017 universe, for instance, had nearly five times the unrestricted cash and investments of the overall median (Figure 2). Healthcare systems that have optimized their investments have accumulated billions more in their war chests with which to support—or expand—their missions.

FIGURE 2 THE IMPACT OF ACCUMULATED ASSETS

Source: Moody’s Investors Service.

Note: The all category also includes institutions with debt rated below Baa and debt not rated.

A Shifting Landscape

While many healthcare systems have benefited from dramatic investment asset growth, no healthcare system will be immune from the substantial revenue and operational challenges that loom for the industry in the coming years. Healthcare institutions are being disrupted by multiple forces including changes to delivery of care, demographic shifts, falling reimbursement rates, rising costs, and increasing competition.

Over the past decade, reimbursement levels have been declining due to demographic trends and the varying rates of reimbursement that apply to different population segments. As the US population ages, the proportion of patients covered by Medicare and Medicaid has increased, resulting in an adverse shift in the mix of reimbursement rates. For example, government payers have increased from 55% in 2006 to 61% in 2016, while commercial insurance payers dropped from 38% of the mix to 33%. 1 Patient volume growth has also been pressured as employers and insurers continue to shift costs to patients through higher deductible plans. These plan structures incentivize fewer healthcare system visits, as patients seek treatment at lower-cost outpatient centers or clinics.

Margins are further compressed by expense pressures, fueled by an uptick in labor costs, as well as nursing shortages in certain regions. Capital expenditures will remain high to support expansion to locations closer to patients and to improve technology within flagship campuses. Investments in medical technology and medical records systems require significant outlays for hardware, software, and ongoing IT staffing.

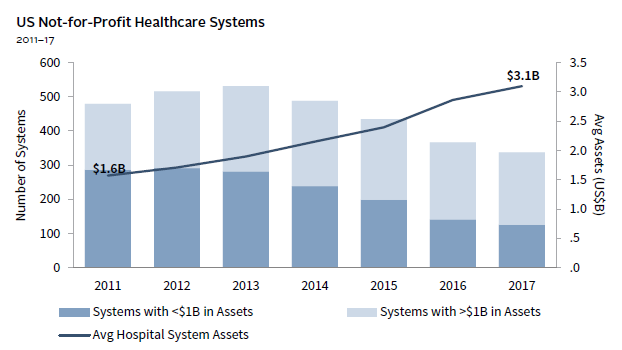

To counter some of these pressures, many healthcare systems have tried to achieve scale and generate greater cash flow through mergers or acquisitions (Figure 3). Larger systems can consolidate administrative functions and better negotiate reimbursement rates with insurers, as well as labor and supply costs. Larger entities tend to have more patient options and diversified revenue streams but, of course, consolidation also brings risk, particularly around integration of services and technology.

FIGURE 3 THE CHANGING HEALTHCARE SYSTEM LANDSCAPE

Source: Modern Healthcare Health System Financials Database.

Scale provides some protection but, as a group, healthcare systems still face the prospect of significant operating margin compression because of these growing pressures. In this environment, institutions with significant investment assets will maintain a distinct advantage, not only by being better equipped to maintain healthy debt ratings, but by having greater capacity to spend in order to subsidize operations and fund capital expenditures.

Calibrating a Different Model

If the pressures described above do indeed force healthcare systems to rely more heavily on their capital reserves for support—if capital reserves become a source of cash rather than a repository for it—strong investment returns will be required to maintain purchasing power of capital pools and to provide a consistent level of support. However, it is important to note that the superior returns that might be generated by the Endowment Model come with greater risks and illiquidity and require skilled implementation for healthcare systems. The Endowment Model is so named because its approach was designed specifically for endowments—pools of capital with a defined purpose, a predictable spending rate, and an infinite time horizon.

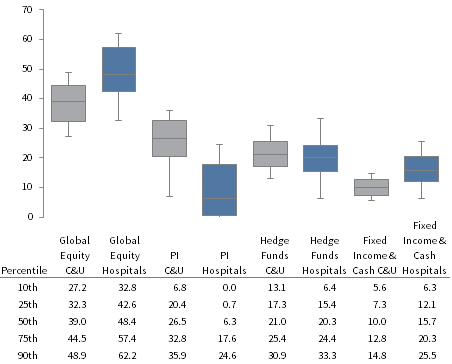

Healthcare systems differ significantly from endowments and foundations in how their investment pools are—and should be—invested. This is demonstrated in the figure below, which shows the range of asset allocation targets for healthcare systems and colleges and universities (C&U) with greater than $1 billion. On average, healthcare systems invest far more in public equities than does the C&U universe, primarily because they have less, on average, in private investments. Healthcare systems are also more likely to have much higher allocations to bonds and cash. Interestingly, there is greater disparity in asset allocations among healthcare system investment pools than C&Us, reflecting the fact that different healthcare systems have very different objectives, constraints, and operating considerations.

ASSET ALLOCATION TARGETS FOR HEALTHCARE SYSTEMS AND COLLEGES & UNIVERSITIES

Source: Cambridge Associates LLC.

Note: Data from 53 Cambridge Associates Colleges and Universities with endowments greater than $1 billion, and from 32 Cambridge Associates healthcare system clients (excluding pensions).

Healthcare systems, however well endowed, are not endowments. As described, healthcare systems tend to rely more heavily on debt, often have multiple pools with different objectives, and typically have less predictable flows into and out of their investable pools. To optimize a healthcare system’s investment strategy successfully, it is necessary to develop a comprehensive understanding of the enterprise and how its various pools work together to support it. We refer to this process as the enterprise review.

Enterprise Review

An enterprise review considers the relationship between the investment portfolio(s) and the healthcare enterprise and provides a framework for investment policy and portfolio construction. In conducting such a review, the operating environment of the healthcare system is the first factor to consider. Will operating margins be positive and contribute to capital plans and asset levels? Or will operating deficits require liquidity from investment pools to balance? Are operating costs fixed or growing, and will they exceed revenues? Or do new conditions, such as merged organizations, create new dynamics where costs can be curtailed by new efficiencies? The complexity and volume of the operating inputs demand attention so that investments can be calibrated for the near term and long term.

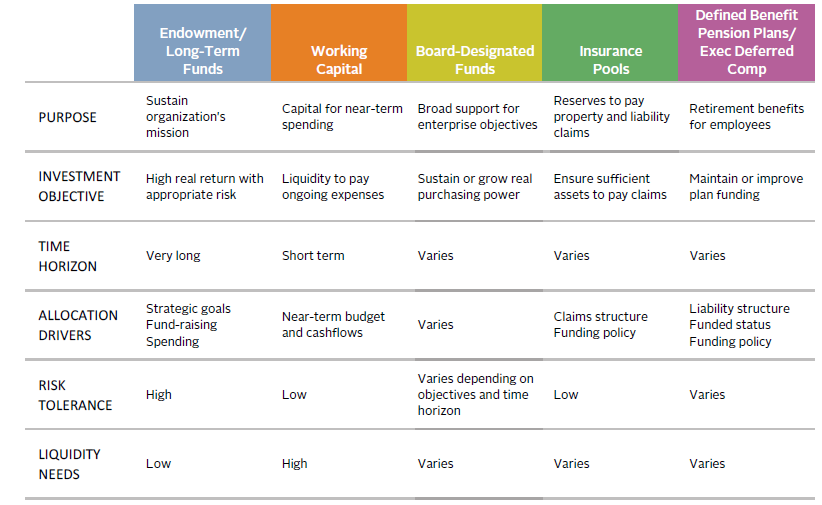

Work must also be done at the individual pool level to define the role each pool plays in supporting the enterprise. Such pools vary broadly by purpose (e.g., long-term restricted fund; escrows; short-term liquidity pool; pension), liquidity, time horizon, and other aspects. Although they may go by different names at different healthcare systems, they generally fall into one of several categories captured in Figure 4.

FIGURE 4 HEALTHCARE SYSTEM INVESTMENT POOLS

Source: Cambridge Associates LLC.

The primary factors influencing asset allocation for each of these distinct pools include minimum acceptable return, time horizon, risk tolerance, purpose of the pool, and liquidity requirements. Factors that may have a greater influence on allocation decisions for healthcare systems than for other institutions include the nature of flows into and out of each pool, 2 the mix of restricted versus unrestricted assets, and the extent to which any of the pools support the issuance or rating of debt. This pool-by-pool exercise may be fairly simple for an entity such as a healthcare foundation or a single-site healthcare system, but can get increasingly complex for multi-campus healthcare systems.

Another critical component of the enterprise review is how the healthcare system’s investment assets support the debt portfolio. The amount, structure, and type of debt on a healthcare system’s balance sheet can have material implications for how the portfolio is invested, from how much illiquidity the enterprise can assume to the choice of investment vehicle. The most obvious investment implication for levered healthcare systems is sustaining a positive debt rating and maintaining compliance with debt covenants. Volatility is another concern because most covenants are tied to a healthcare system’s level of unrestricted funds. A sudden drop in unrestricted assets could trip key covenants precisely at a time when refinancing or paying down debt becomes significantly more difficult.

Healthcare systems with defined benefit pension plans face an additional layer of complexity. As we have written in a previous piece, pension risk management is best executed by looking at the key levers of asset returns, liability hedges, contribution policy, and benefit management. 3 Healthcare systems with defined benefit plans that are open and accruing new benefits, for instance, may emphasize targeting higher returns through equity orientation and lessened liquidity. Meanwhile healthcare systems with frozen plans will likely gravitate toward liability-driven investment mandates that seek to protect the healthcare system’s balance sheet from adverse pension funding hits that may result from equity volatility or detrimental moves in interest rates. In most cases, however, careful coordination of at least several of these levers is key to effective pension plan management.

These different factors often lead healthcare systems to have a higher bias toward liquidity and safety than necessary. But healthcare systems can create long-term, intermediate-term, and short-term investment pools, and aggregate assets by investment objective, even if the pools must be tracked separately for accounting and reporting purposes. The work of the enterprise review can identify how each sub-pool can be invested to maximize return and ultimately build out long-term capital.

Honing in on the “Fulcrum”

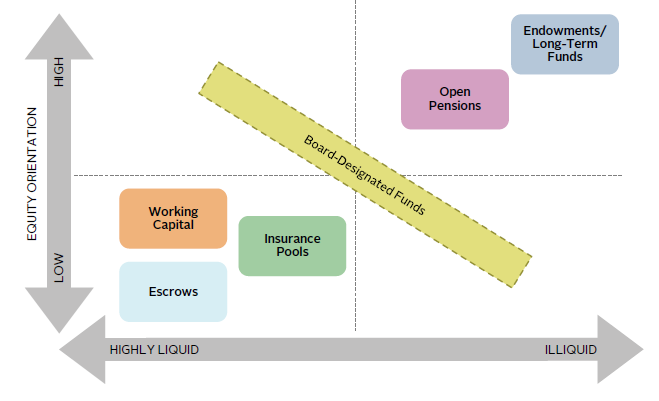

Aggregating and streamlining the investment structure can substantially reduce complexity and optimize portfolio efficiency, including by consolidating manager relationships across multiple sub-accounts to maximize fee savings. But the greatest benefit achieved by optimizing the pool structures is the identification of the assets “at the fulcrum”: assets in excess of immediate liquidity needs or debt covenants that can be invested with a longer time horizon, take on more risk and illiquidity, and generate higher return. If reasonable scenario analysis determines such fulcrum assets are not needed to fund short- to mid-term capital requirements, they may be directed toward less liquid, longer-term equity strategies with maximum risk-adjusted return potential (Figure 5).

FIGURE 5 OPTIMIZING HEALTHCARE SYSTEM RETURN AND LIQUIDITY

Source: Cambridge Associates LLC.

Embracing Equity and Illiquidity

While return expectations are far higher for equities than for bonds under normal conditions, the current environment of extended global equity valuations may challenge equity returns in the intermediate term. Lower returns from market beta therefore necessitate the exploration of value-add strategies that can keep return potential healthy.

Perhaps the strongest source of value-added returns, private investment strategies have been a powerful return driver. However, the ability to commit capital to such strategies hinges greatly on the enterprise’s ability to absorb illiquidity risk. If successfully executed—with a consistent, disciplined process and the ability to identify and access top-tier managers—investments in areas such as private equity, venture capital, private real assets, and private credit may potentially provide multiple percentage points of enhanced return. This requires discipline and the ability to identify and access top-tier investment managers. In addition, the appropriate pacing strategy for private investment commitments needs to be based on a keen understanding of enterprise cash flows.

Healthcare Systems’ Risk Management Constraints

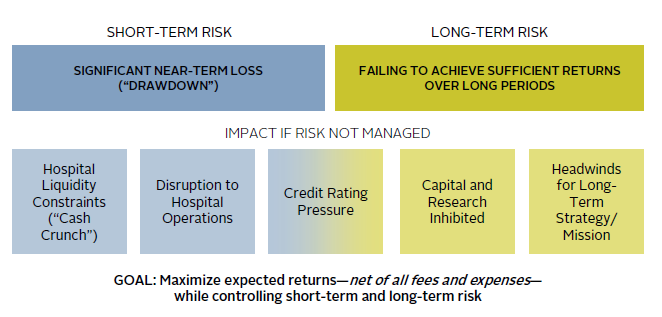

Although the opportunity exists to maximize investment gains through high equity orientation and harvesting the benefits of illiquidity, such exposure does result in greater investment risk. Defining, assessing, and ultimately managing this investment risk should be an exercise that is performed in close concert with each organization’s leadership; neither investment risk nor organizational risk can be treated as a “given,” as both are quite interrelated. Figure 6 captures the impact of investment risk, and the ultimate peril it may create for the organization if poorly managed. The risks associated with equity orientation in particular—drawdown risk and high asset volatility—can be thought of as short-term risks. Such risks should never be assumed without a realistic ability to tolerate the severity of loss that may occur by holding higher-return/higher-risk, equity-oriented assets. If not managed correctly, such risk can have damaging consequences for healthcare system operations and needed liquidity.

FIGURE 6 HEALTHCARE RISK MANAGEMENT ACROSS TWO DIMENSIONS

Source: Cambridge Associates LLC.

As a foil to short-term risk, equal attention must be paid to the concept of long-term risk, which expresses the risk of failing to achieve sufficient returns over longer periods of time in inflation-adjusted terms. Such long-term risk results from an overly conservative investment strategy that may mitigate short-term risk by minimizing volatility but lead to a cumulative shortfall over time. These competing short-term and long-term risks can both be addressed by examining the healthcare system enterprise from the bottom up, at the most granular account level, as well as from the top down in a strategic sense.

Creating the Optimal Portfolio

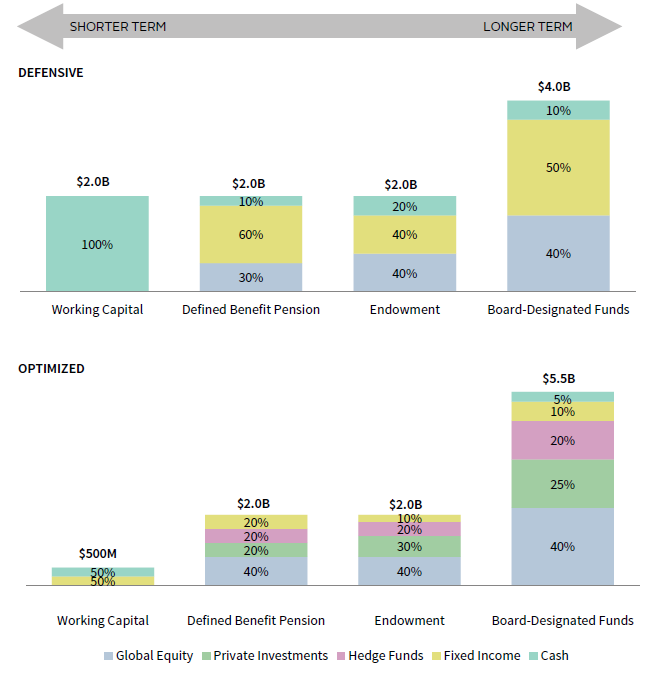

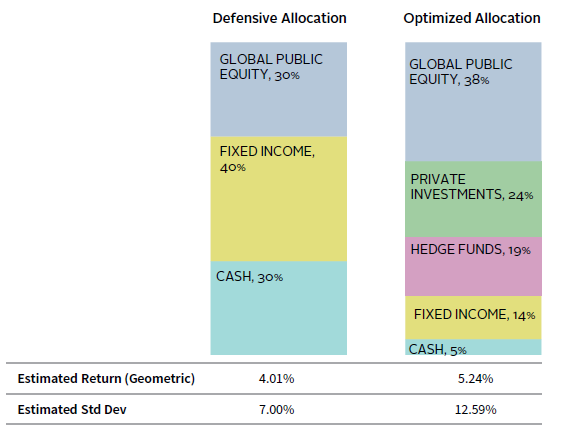

An optimal asset structure for healthcare systems not only addresses the allocation across asset classes but also the sizing of pools so as to ensure alignment with risk/return objectives. Figure 7 demonstrates this effect by comparing a more defensive healthcare system against an “optimized” healthcare system with regard to investment allocation and pool sizing. Although both institutions have identical assets for investment, the defensive institution maintains a higher allocation in shorter-term pools (i.e., working capital), while the optimized healthcare system has directed as much money as possible to longer-term pools (i.e., board-designated funds). In addition, the defensive healthcare system maintains more conservative asset allocations within each pool with heavier allocations to bonds and more liquid asset classes. Conversely, the optimized healthcare system has invested higher allocations in equity-oriented and less liquid asset classes.

FIGURE 7 OPTIMIZING ASSET STRUCTURE THROUGH ASSET ALLOCATION & POOL SIZING

Source: Cambridge Associates LLC.

Note: Please see the disclosures at the end of the publication for more information on our hypothetical and projection performance.

Figure 8 highlights the aggregate asset allocations of these two healthcare systems and the potential expected return outcomes. Larger allocations to private equity, hedge funds, and equity result in higher expected returns for the optimized portfolio. Also, we believe the optimized allocation has greater potential for alpha generation due to its underlying exposures. With multiple points of return differential between the two healthcare systems in this case study, the optimized healthcare system allocation is potentially in a better position to generate higher investment returns that could compound over time, resulting in incremental funds that could then be directed to key capital initiatives for the institution.

FIGURE 8 AGGREGATE ASSET ALLOCATIONS AND POTENTIAL RETURN OUTCOMES

Source: Cambridge Associates LLC.

Note: Please see the disclosures at the end of the publication for more information on our hypothetical and projection performance.

To translate the expected return impact into dollars, assume both healthcare systems hold $10 billion in total assets across these pools. The healthcare system with a more optimized pool structure and asset allocation would be expected to earn an additional $123 million per year from beta return alone with additional gains possible through higher value-add opportunities. While such a return experience would come with greater return volatility, larger equity allocations and illiquid investments would deliver substantial compounded gains over time to the more optimized investment structure.

Quantifying and “Stress-Testing” the Impact of Investments on the Enterprise

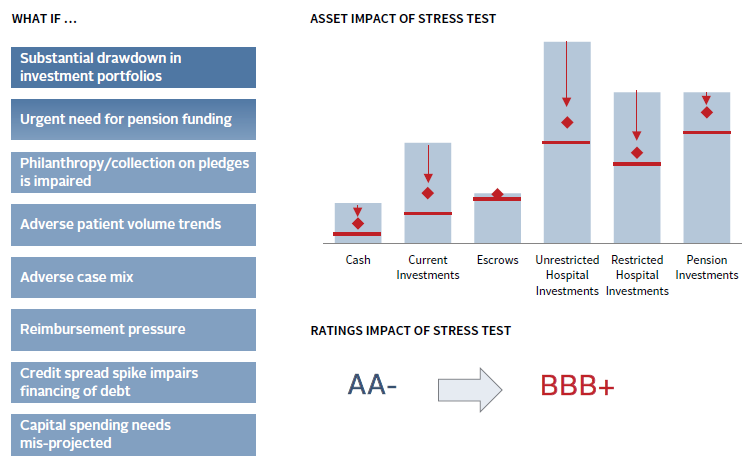

One of the most valuable exercises in healthcare investment management is conducting a thorough stress test to simulate a severe market event. The most robust stress test should be conducted as a partnership between investment and finance teams—making severe, but possible, assumptions of operational and investment adversity throughout the organization and investment pools. For the healthcare institution’s operations, economic adversity may mean modeling stresses such as severe declines in volumes or revenue, worsening of revenue mix, unexpected cost spikes, sudden regulatory uncertainty, impairment of cash flow conversion (i.e., will collections of receivables be impacted?), and balance sheet pressures that may damage the credit rating. For the healthcare institution’s investment pools, adversity can be quantified by stress testing each pool for a seizing up of capital markets including liquidity implications. The blended operational and investment stress-test results in calculating a theoretical “low water mark.” This worst-case base level should still be sufficiently high for all healthcare constituencies to take comfort that the enterprise is not assuming too much investment risk and can remain resilient (Figure 9).

FIGURE 9 STRESS TESTING THE HEALTHCARE SYSTEM

As of December 31, 2016

Source: Cambridge Associates LLC.

Expectations can be set on explicit dollar returns from all healthcare investment accounts in both a long-term (25+ year) capital market forecast as well as on a more interim-term basis that captures the current investment environment. In effect, these projections become a capital budgeting exercise that will hold significant value to the organization’s leadership and may influence capital decisions for years to come. Strategic check-ins should be conducted at least annually to refresh the impact of the investment “profit center,” and analysis can be conducted to identify any interrelatedness between capital market conditions and the healthcare institution’s core operations.

Adapting to Change in the Healthcare Industry

Healthcare systems must confront an increasing number of disruptive structural forces in their operations that will require greater dependence upon investment pools and calibration of investment strategy to adapt to new demands. Healthcare operations may face greater uncertainty not only in day-to-day profitability but in terms of the capital expenditure levels needed to adapt to a changing industry model. Concurrently, high valuation levels across most asset classes may set the stage for a lower return environment in the coming years. At both the pool-by-pool and enterprise levels, many healthcare systems confront the reality that cash flows are a two-way street; recent years’ accumulations could reverse in direction as capital demands escalate. While many healthcare systems have become accustomed to the positive side of these flows, all should now be prepared for a reversal. The most effective strategy will acknowledge the uncertainty associated with future cash flows, but avoid being overly conservative so as not to impair future cash flow generation.

Hypothetical Performance Disclosure

This publication contains hypothetical performance. Hypothetical performance results have many inherent limitations, some of which are described below. There are frequently sharp differences between hypothetical performance results and the actual results subsequently achieved by any particular investment program. Hypothetical results do not involve financial risk, and no hypothetical record can completely account for the impact of financial risk in actual investing. For example, the ability to withstand losses or to adhere to a particular investment program in spite of losses are material points, which can also adversely affect actual performance results. There are numerous other factors related to the markets in general or to the implementation of any specific investment program, which cannot be fully accounted for and all of which can adversely affect actual results.

Projection Performance Disclosure

The return to normal scenario incorporates current valuations and assumes equity valuations revert to fair value over ten years. This scenario makes assumptions about the market environment including mild inflation, moderate real earnings growth, and low corporate default rates, government bond yields, and credit spreads. The standard deviation estimate is based on long-term equilibrium projections and can be unstable over shorter time periods.

Footnotes

- Moody’s Investors Service, “Not-For-Profit and Public Healthcare – US: 2018 Outlook Changed to Negative Due to Reimbursement and Expense Pressures,” December 2017.

- Unlike endowments, where flows out of the portfolio are often substantially greater than flows into it, healthcare system pools may have greater inflows than outflows or vice versa depending on the purpose of the pool. For example, capital reserve or long-term funds may have very little spending, if at all, but may benefit from the addition of operating surpluses, resulting in a positive net flow in most years, with the possibility of negative flows when funds are called upon. Funded depreciation pools may also grow in a typical year, but be subject to large and unpredictable withdrawals.

- Jeff Blazek et al., “A Balancing Act: Strategies for Financial Executives in Managing Pension Risk,” Cambridge Associates Research Report, 2017.

Tracy Filosa - Tracy is a Managing Director and Head of CA Institute.

Hamilton Lee - Hamilton is Co-Head of the Healthcare Practice at Cambridge Associates.

About Cambridge Associates

Cambridge Associates is a global investment firm with 50+ years of institutional investing experience. The firm aims to help pension plans, endowments & foundations, healthcare systems, and private clients achieve their investment goals and maximize their impact on the world. Cambridge Associates delivers a range of services, including outsourced CIO, non-discretionary portfolio management, staff extension and alternative asset class mandates. Contact us today.