Expect Lackluster Returns on Most Liquid Credits

Low yields on many liquid credit assets curbed returns in 2021, a trend that seems likely to continue in 2022. Central banks have begun hiking rates and curbing asset purchases as strong growth pushes inflation higher, a headwind for fixed rate assets in particular. Despite strong 2021 performance, floating-rate collateralized loan obligation (CLO) liabilities may again outperform, aided by reasonable spreads. Still, most liquid credit is likely to underperform higher-spread private credit, which often benefits from higher-quality underwriting.

Strong economic growth and rising inflation in 2021 pushed government bond yields higher, hurting core fixed income returns. While growth may moderate somewhat in 2022, persistent inflationary pressures mean market expectations for rate hikes are being moved forward. Unfortunately, spread compression in many credit assets has resulted in scant cushioning to offset rising rates. As an example, the current spread on BB-rated corporate bonds (around 230 bps) has only been this low 28% of the time, though leveraged loan spreads are much closer to historical medians.

The flipside is that a strong economic recovery has helped corporate fundamentals rapidly rebound, and they may continue to improve in 2022. Metrics like net leverage and interest coverage for high-yield borrowers are now better than historical averages, and default rates have fallen below 1%. Rating agencies are scrambling to reverse last year’s downgrades, and a dramatic upgrade cycle is in turn improving metrics for structured finance vehicles like CLOs.

Next year, assets like US high-yield bonds and broadly syndicated loans with sub-5% yields may only generate low/mid-single-digit returns, and longer-duration investment-grade bonds could post losses if there are more rate hikes than expected. Within liquid credit, CLO liabilities stand out by offering higher spreads than similarly rated corporate peers, though liquidity is a consideration. Private credit strategies like direct lending, which offer higher spreads and demonstrated their resilience during the pandemic, should do better still. Assuming that ample liquidity has been reserved to meet anticipated spending and other needs, cash is not compelling, as low yields will continue to drag on portfolio returns. Short-duration exposure to high-quality securitized and corporate credit is a compelling alternative.

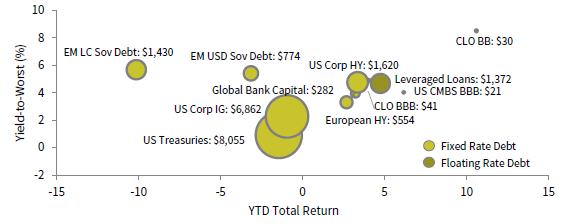

MANY CREDIT INVESTMENTS OFFER MODEST YIELDS

As of November 30, 2021 • US Dollar

Sources: Bloomberg Index Services Limited, Credit Suisse, and J.P. Morgan Securities, Inc.

Notes: The area of each bubble represents the current market value of each index, shown in USD billions. CLO BBB bubble is covered by US Corp HY and Leveraged Loans. Global Bank Capital is represented by the Bloomberg Global Contingent Capital Index, CLO BBB by the J.P. Morgan CLO BBB Index, CLO BB by the J.P. Morgan CLO BB Index, US CMBS BBB by the Bloomberg US CMBS Investment Grade Baa Index, US Corp IG by the Bloomberg US Corporate Investment Grade Index, EM LC Sov Debt by the J.P. Morgan GBI-EM Global Diversified Index, EM USD Sovereign Debt by the J.P. Morgan EMBI Global Diversified Index, European HY by the Bloomberg Pan European High Yield Index, Leveraged Loans by the Credit Suisse Leveraged Loan Index, US Corp HY by the Bloomberg US Corporate High Yield Index, and US Treasuries by the Bloomberg US Intermediate Treasury Index. Total returns data for EM LC Sovereign Debt are in USD terms. Yield for the Credit Suisse Leveraged Loan Index is calculated as the three-month LIBOR plus three-year discount rate.

Wade O’Brien - Wade O’Brien is a Managing Director for the Capital Markets Research team at Cambridge Associates.

About Cambridge Associates

Cambridge Associates is a global investment firm with 50+ years of institutional investing experience. The firm aims to help pension plans, endowments & foundations, healthcare systems, and private clients achieve their investment goals and maximize their impact on the world. Cambridge Associates delivers a range of services, including outsourced CIO, non-discretionary portfolio management, staff extension and alternative asset class mandates. Contact us today.