Will the Nascent Shift in Equity Market Leadership from US to Non-US Equities Persist?

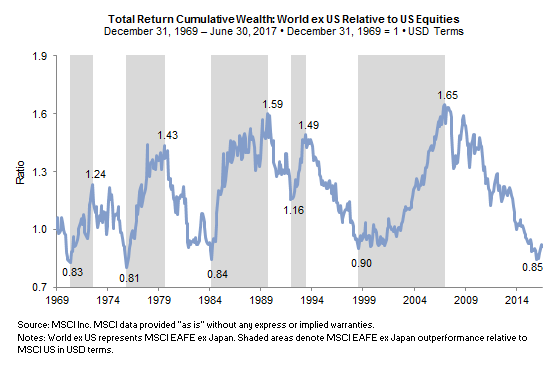

Prospects for a continued turn in the cycle look promising. US outperformance relative to other developed markets peaked in November 2016, as the chart below shows, raising the prospect that the cycle has indeed turned. US equity leadership has faded as valuations have moved into very overvalued territory, while other markets are fairly valued and both economic and earnings momentum outside the United States have picked up. Further, the United States is at a later stage in the economic cycle than other markets, suggesting that continued economic growth is more likely to result in profit margins coming under pressure from rising wages and higher interest expenses than in other markets that maintain considerably more economic slack.

While political risks outside the United States remain and will continue to usher in uncertainty regarding prospects for economies, earnings growth, and currencies, recent months have seen some improvements. Political risks in the Eurozone have moderated considerably this year with the defeat of populists in Dutch elections in March and the election of the staunchly pro-European Emmanuel Macron as France’s president in May. The strong showing by Macron’s party (La République En Marche!) in the National Assembly elections has opened the possibility that Macron will be able to push through labor reforms, perhaps serving as a bargaining point with Germany in exchange for movement toward a common European budget and sharing of fiscal responsibility after the German election in September.

Upcoming Italian elections remain a potential flashpoint for Europe. Elections must be held by May 2018 amid political instability following roughly a decade of low economic growth, high unemployment, and elevated debt levels. Even as the Italian economy has been lagging other Eurozone countries, conditions are improving for now, providing some easing of political pressure. Importantly, European Union authorities agreed in June to allow Italy to circumvent the EU’s Bank Recovery and Resolution Directive that was preventing Italy from cleaning up its troubled banking sector.

Political and economic risks in the United Kingdom, in contrast, appear to be on the rise. The loss of the Conservative party majority in Parliament in the June 7 snap election—called by Prime Minister Theresa May in a failed effort to increase her party’s majority—has raised uncertainty regarding “Brexit” negotiations. The absence of a Parliamentary majority means the UK’s Brexit negotiating position is not stable and, whatever the outcome, will probably fail to be approved by a majority in Parliament. The uncertainty now surrounding the government and Brexit will send animal spirits into hibernation. Already the UK economy is showing some signs of faltering.

Turning to Japan, economic conditions have improved recently. We continue to see improvements in corporate governance as an important driver of profitability and increased returns to shareholders, including increasing dividends and share buybacks. Challenges remain, including the volatility in Japanese equity shares associated with yen moves and, over the long term, the growth drag from a declining population.*

Across these markets, earnings growth and expectations for forward growth have mirrored improved economic conditions. For example, after falling for the better part of the last five years, Eurozone earnings have turned up, while UK earnings remain stagnant. Similarly, after hitting a rough patch last year, Japanese equity earnings growth has resumed. Relative to the United States, earnings growth prospects for the Eurozone, Japan, and emerging markets over the next two years are at least as good, if not better, and valuations are favorable. If earnings growth is sustained, this valuation gap should narrow, with non-US markets rerating to higher valuations. As earnings are more depressed relative to US equities and the economic cycle is less advanced, non-US earnings will likely grow more rapidly, provided the economic expansion persists.

Should the economic expansion stall, US equities would likely outperform, as the US market and US dollar tend to benefit from a “flight to quality” in times of stress. However, extreme relative valuations suggest that over the long term, US equities should underperform from a starting point of today and that even in a downturn, relative underperformance of non-US equities would be mitigated by their more attractive starting valuations.

Celia Dallas - Celia Dallas is the Chief Investment Strategist and a Partner at Cambridge Associates.

About Cambridge Associates

Cambridge Associates is a global investment firm with 50+ years of institutional investing experience. The firm aims to help pension plans, endowments & foundations, healthcare systems, and private clients achieve their investment goals and maximize their impact on the world. Cambridge Associates delivers a range of services, including outsourced CIO, non-discretionary portfolio management, staff extension and alternative asset class mandates. Contact us today.