2023 Outlook: Interest Rates

We expect interest rates will increase in many developed markets, as implied by market pricing. But we think the Fed will hold rates in restrictive territory for longer than expected. We don’t believe any increases will prompt another European sovereign debt crisis.

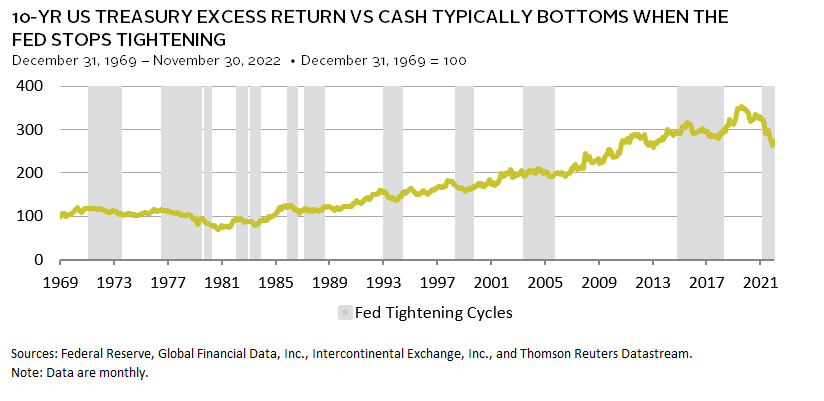

US Federal Reserve Pauses, but Does Not Pivot in 2023

Celia Dallas, Chief Investment Strategist

The US Federal Reserve has sent clear signals that inflation is enemy number one and that defeating inflation requires further monetary policy tightening even if this results in recession. We see a pause in tightening as more likely than a pivot to easing in 2023 because inflation will be slow to decelerate, causing the Fed to hold rates in restrictive territory 1 for longer than many other cycles.

Inflation is starting to decelerate in some segments of the economy; however, “sticky inflation” sources (e.g., housing, services) continue to accelerate. Wages are supported by persistent labor market strength and will only ease as the economy softens. Unemployment remains near recent lows of 3.5% amid lower, but still robust, job growth. The number of job openings is down by more than 10% from its March peak, so the labor market is starting to soften, but it remains tight.

With inflation decelerating slowly and labor markets showing resilience, the Fed will see little reason to pivot in 2023. At the end of November, the market is pricing in that the Fed will stop tightening in May 2023 with a terminal rate of 4.9%. This would imply an average degree of tightening based on tightening cycles since 1965 despite an above-average level of inflation. Still, markets will be far less vulnerable to rising rate risk in 2023 given the degree of tightening priced into the market.

Developed Markets Government Bonds Will Rebound in 2023

TJ Scavone, Investment Director, Capital Markets Research

Global bonds are on pace to suffer their worst year on record in 2022, with the FTSE® World Government Bond Index returning -18.1% through November 30 in USD terms. Unlike today, yields offered on government bonds were near their all-time lows heading into 2022, which left them vulnerable to the sharp rise in yields that occurred as central banks tightened policies.

Monetary policymakers have aggressively tightened policy in 2022 to bring down elevated inflation. Out of the 37 central banks tracked by the Bank for International Settlements, 33 have raised policy rates so far in 2022, with the median central bank increasing rates by 275 basis points (bps). However, we expect most central banks to dial back (or pause) tightening efforts in 2023, which should support government bonds.

There are several other reasons to suggest government bonds will perform better in 2023. For one, negative return years are rare. Ten-year US Treasuries have only experienced 11 negative return years out of 63 since 1960, and only once experienced back-to-back years of negative performance, in 2021 and 2022. Second, 2022’s sell-off was extreme. For example, on a rolling 12-month basis, ten-year UK gilt yields at one point had increased as much as 307 bps this year, which is the 13th largest increase since 1901, and the benchmark suffered its third worst 12-month performance on record over this period. Lastly, at some point, we expect the market will see stronger demand from buyers looking to lock in higher yields, such as pension funds.

Government bonds could continue to struggle if inflation remains sticky and central banks tighten more than expected. However, investors are being fairly compensated for duration risk at current yields based on long-term trends in economic fundamentals. In the short term, growth is slowing, which should help limit any further rise in yields. If yields do overshoot, government bonds have less downside, as index yields have increased and duration has fallen, whereas if the aggressive tightening by global central banks does cause a recession next year, government bonds are better positioned to support portfolios.

For many credit assets, 2022 will likely go down as one of the worst on record, but the flipside of poor performance is higher yields, which will eventually generate higher returns. The path to these returns could be bumpy, however, and investors should plan accordingly. Current potential headwinds include higher interest rates than anticipated and decreased debt affordability.

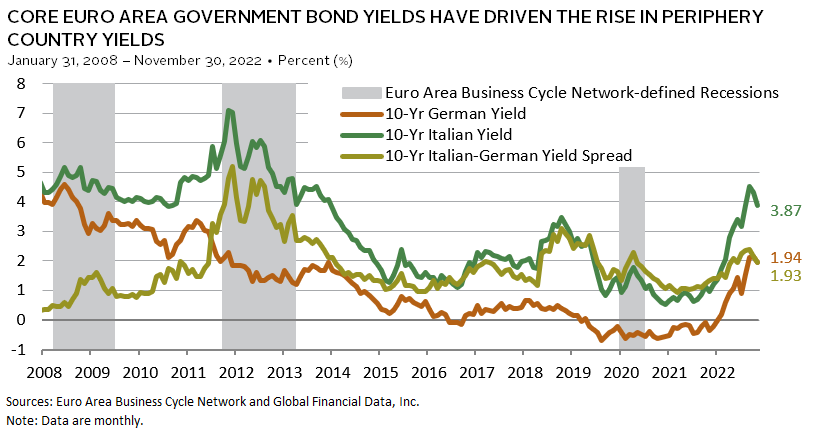

A European Sovereign Debt Crisis Will Not Occur in 2023

TJ Scavone, Investment Director, Capital Markets Research

European policymakers face a difficult challenge as the energy shock has increased the risk of stagflation, as we detail elsewhere in this outlook. The resulting mix of tight monetary and loose fiscal policies has heightened concerns about debt sustainability and put upward pressure on euro area (EA) government bond yields.

However, while ten-year Italian government bond yields, for example, are the highest they’ve been since the 2009–12 European Sovereign Debt Crisis, unlike previous “debt scares,” the rise in yields in 2022 has been driven by higher core EA country yields. The spread between ten-year Italian-German yields, while elevated, remains below its 2018 high and well below the heights reached in 2011. EA periphery yields may move higher as the European Central Bank (ECB) continues to tighten, or if the economic outlook deteriorates. But we do not expect spreads to blow out as they did in 2011–12.

Italy likely represents the biggest risk to this view. With a debt-to-GDP ratio of 150%, Italy is one of the most indebted EA countries. The combination of higher borrowing costs, looser fiscal spending, and weaker growth threatens to further strain Italy’s fiscal position. Further complicating matters is the far-right coalition’s recent election victory. However, high inflation and the low average cost and longer average maturity of outstanding Italian debt should mitigate the impact of higher borrowing costs and increased fiscal deficits. Italy also has less incentive to take a hardline stance toward the EU, as it did in 2018, given stronger support for the EU within Italy and the fact that Italy has grown increasingly dependent on the bloc.

Quantitative tightening is also a risk, but the ECB is incentivized to prevent a periphery spread widening, as it would reduce its ability to address inflation via tightening. As such, it has added tools (e.g., flexible pandemic emergency purchase programme reinvestments and the Transmission Protection Instrument) to strengthen the credibility of its backstop. If there was a large move in Italian-German spreads above their 2018 highs, we would likely view it as a buying opportunity.

Footnotes

TJ Scavone - T.J. is a Senior Investment Director in the Capital Markets Research Group at Cambridge Associates.

Celia Dallas - Celia Dallas is the Chief Investment Strategist and a Partner at Cambridge Associates.

About Cambridge Associates

Cambridge Associates is a global investment firm with 50+ years of institutional investing experience. The firm aims to help pension plans, endowments & foundations, healthcare systems, and private clients achieve their investment goals and maximize their impact on the world. Cambridge Associates delivers a range of services, including outsourced CIO, non-discretionary portfolio management, staff extension and alternative asset class mandates. Contact us today.