Investment Governance: Creating a Framework That Works for a Family

Investment governance plays a critical role in the ability of families with substantial wealth to define their financial objectives and formulate a strategy for a diversified portfolio. Investment strategy—including asset allocation, selection and monitoring of investments, and risk management—demands a large amount of attention from families and their advisors. While investment governance is at least as important, it too often receives less consideration. A well-defined governance framework is what drives an investment strategy and increases a family’s ability to formulate investment goals and execute on them over time. Without clear governance, families and their advisors will find it harder to engage in effective decision making, which can lead to adverse outcomes.

This paper provides an overview of investment governance that families can use in the development of their own investment decision-making framework. It focuses on three core building blocks of governance: people, authority, and process. A carefully constructed, intentional governance scheme incorporating these three elements will foster better alignment between the family’s goals and their investment strategy. As part of the examination of governance, a close look at the potential benefits of investment committees is provided. Also included is a list of best practices, which can help families develop an approach best suited to their needs.

What Is Investment Governance?

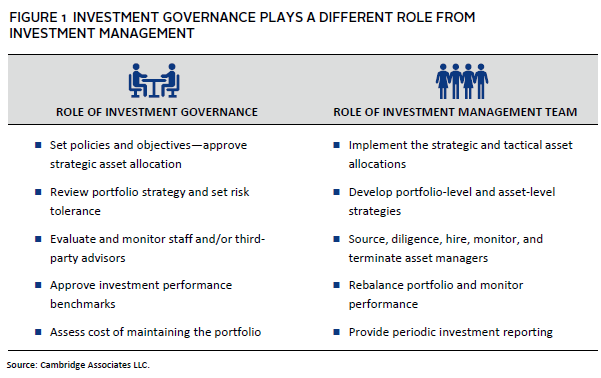

Investment governance is the process through which an individual or group exercises investment authority, makes investment decisions, and conducts investment oversight. At its best, governance focuses on a family’s high-level investment policies in accordance with the objectives of wealth owners and beneficiaries. Good governance should not be confused with the execution of an investment strategy. This distinction is a cornerstone of good governance and will help families who are developing their own investment governance policies avoid confusion that risks degrading the broader investment program (Figure 1).

There are other elements of investment governance besides decision making, including transparency, education and training, and strong leadership. Providing transparency into portfolio choices and allowing for honest discussion of successes and failures will help the broader group of family members better understand why the portfolio is behaving in a particular way. It can also strengthen their buy-in to the strategy. This is especially true when investments do not meet expectations. Education and training can also help the next generation of family decision makers be better prepared to assume leadership positions. Strong leadership—including knowledgeable and engaged family members and well-defined governance and management roles—can strengthen relationships with third-party investment advisors.

Three Building Blocks of Investment Governance

The right approach to investment governance varies greatly because each family has its own needs. Incorporating the following three building blocks of investment governance can help families create a framework that works best for them.

- People. Determine which family members, if any, will occupy a role in governance and what decision-making responsibilities might be delegated to third parties.

- Authority. Define the source of decision-making power in legal terms and how best to adhere to those requirements, such as whether authority is exercised by the family or third parties.

- Process. Articulate the decision-making procedures and the degree of formality to be adopted by the family or third parties.

A family can tailor each of these components to their particular circumstances as they optimize their approach to investment governance.

People

The earliest iterations of investment governance adopted by families of wealth are often relatively simple. For example, a first-generation wealth creator may reserve the right to make decisions as part of maintaining control. As the family grows and the number of portfolio stakeholders increases over time, they may need to develop a more representative system and further formalize investment governance, or at least put guardrails in place. More complex governance is typically required when second or third generation family members are empowered to reconsider an existing framework. When there are more wealth owners and beneficiaries, there is often a demand that decision-making roles be better defined to further promote trust, confidence, and broader representation. A family may decide to delegate some or all of the decision-making authority to one or more third parties, such as a family office, investment counsellor, private trust company, or other type of trustee.

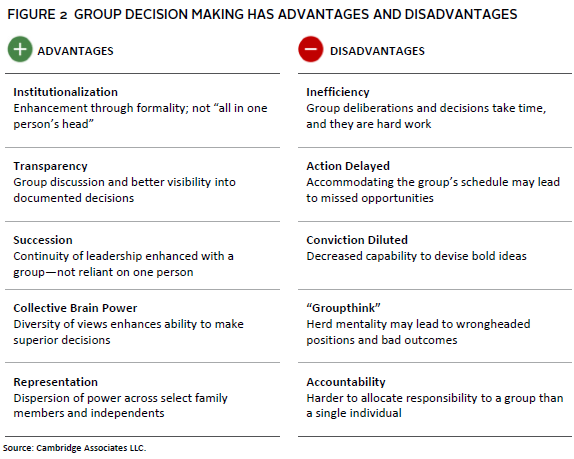

Another key decision that families should make is whether an individual or a group will be empowered to make investment decisions. Some families prefer more institutional, group-oriented decision making, but also want to maintain flexibility. There are ways to create group decision-making frameworks that are not overly constraining and that permit a constructive exchange of views. Figure 2 presents an overview of some of the advantages and disadvantages inherent in group decision making.

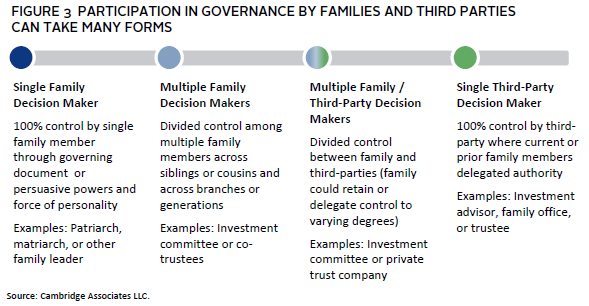

Some families want to be engaged and have a role in governance, while others don’t want to be as actively involved. Many families fall somewhere in between these two ends of the spectrum. Figure 3 shows four ways participation can be structured between family and third parties.

No matter individual participants’ level of participation, family members should think through their investment governance roles, including which elements of decision making will be retained and which will be delegated.

Authority

In addition to determining who is involved, a family should address the nature and source of legal authority for decision making. Authority usually resides in one of two places: a legal entity created by the family or a third-party investment advisory agreement. Any legal entity created by families to control or hold financial assets—whether a trust, family limited partnership (FLP), family office, or private trust company—inevitably has governance provisions. No matter what form the legal entity takes, the family should determine where the power to make investment decisions sits. For example, an investment committee with a chair and members might be created under the terms of a FLP to make investment decisions. Alternatively, a FLP might grant authority to a general partner.

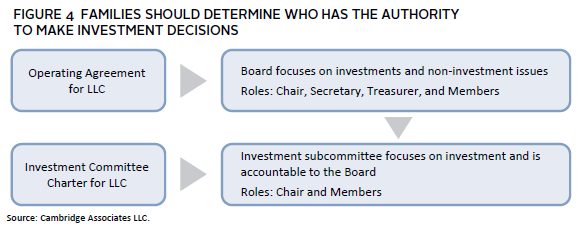

Figure 4 provides an example of an investment governance framework based on a legal entity holding diversified financial assets. In this example, a family establishes a limited liability company (LLC) whose operating agreement delegates authority over investment and non-investment issues to a board. An investment subcommittee is formed to focus on investments and is accountable to the board.

If a third-party investment advisor is hired, the family will have to decide whether to grant it decision-making authority as part of an investment advisory agreement. There are two approaches:

- Discretion. The family delegates full investment decision-making authority to a third-party portfolio manager or other type of investment advisor under a contractual relationship.

- Non-discretion. The family retains full investment decision-making authority for itself, or entities it has created, such as a family office or a trustee.

Some families opt for a middle ground approach, known as “partial discretion,” in which the family shares decision-making responsibility with the third-party investment advisor. In this case, clear demarcation of decision-making responsibilities is necessary to optimize the broader investment program and avoid misunderstandings.

Consider this nuanced example of partial discretion: a group of second-generation siblings hire a third-party investment advisor to help manage their family’s diversified portfolio. The siblings do not have investment backgrounds themselves, yet wish to retain some control. Thus, partial discretion is delegated to the investment advisor. In this scenario, the siblings can opt to retain discretion over “big picture” objectives, including strategic asset allocation. However, they can choose to delegate more tactical decisions, including establishing and adjusting individual investment positions and portfolio rebalancing. In terms of commitments to more illiquid private investments, the siblings can retain power of consent. Here, they may want to retain the ability to review and approve what could be a ten-plus year commitment to individual illiquid investments that cannot be unwound easily in the near term. In the final analysis, the family must be comfortable with the amount of authority delegated.

Process

The third component of investment governance that a family should consider is process, namely, the degree of formality decision makers will need to follow. Families should outline steps to be followed for making decisions, articulate who is authorized to decide, define the scope of responsibilities granted (or not granted) to decision makers, and establish a method for documenting and communicating decisions. A clear governance process will guide more effective investment management. This applies both to governance frameworks based on a single decision maker, but it is even more relevant when there is a group of decision makers.

As families grow larger, their need for clearer and more robust investment governance processes often grows as well. Increased formalization can ensure that governance remains accountable to more passive owners and beneficiaries. In this case, less engaged family members can take comfort that processes are in place, limiting the chance a precipitous decision will be made without any checks and balances. No matter the stage of a family’s development, a well-defined governance process is essential to setting and meeting expectations and maintaining confidence, integrity, and discipline in investment decision making.

Investment Committees

An investment committee is a formal body with a written charter that is tasked with making investment decisions within its legal authority. The aim of the committee is to synthesize diverse opinions and institutionalize the decision-making process, helping to reduce or eliminate biased or emotional decision making. Many families opt to form an investment committee to govern their investment strategy and goals. The investment committee model, explored below, is a well-known and widely practiced way of establishing a clear investment governance process.

The investment committee model can be customized to fit a family’s specific needs. For example, operating under the terms of a charter, a group of family members—perhaps including some “independent” or non-family members—can engage in discussion and make decisions about the strategic direction of the portfolio. Another option might involve a committee that provides for a senior family member to serve as chair with veto power over group decisions; this choice is most common when the wealth creator wants to maintain control. An investment committee may also be “advisory only”—that is, without the authority to make binding decisions—as that power has been delegated. An advisory committee, in addition to communicating opinions to a decision maker, can also serve to educate family members through participation in the investment process and provide a forum for discussion within the family group.

If a family uses an investment committee, five elements should be incorporated into the charter:

- Authority. Provisions for the investment committee’s authority is stipulated by a legal entity or vehicle that is linked to a broader governance and ownership structure.

- Purpose. Decision making is the most obvious purpose, but there may be others, such as communication to the broader family and education of the next generation.

- Responsibilities. Typical areas of responsibility are to establish policies and investment objectives, determine risk tolerance, evaluate performance, and monitor costs.

- Membership. Parameters set for the size of the committee, role of the chair, process for nominations, length of terms, qualifications, compensation, and rules for making decisions.

- Meetings. Rules for notice and frequency of regular and special meetings are defined along with the use of agendas and minutes with supporting written materials and financial reports.

These five elements can and should be crafted to create a committee that is customized to the family’s requirements, permitting robust discussion and good outcomes. Keep in mind an investment committee is not necessarily the right solution for every family. Other options include the delegating of investment decisions to co-trustees or a third-party investment advisor.

Best Practices

Formulating the investment governance approach best suited to a family’s needs can be a complex undertaking, but a consideration of the following best practices can help:

- Level of Family Engagement. Determine the dimensions of the family’s investment governance and what decisions will be retained, delegated, or shared by the family with third parties in each instance.

- Role. Differentiate between governance and management. Good governance separates the two, with governance focused on oversight, strategy, and planning—not execution.

- Strategic View. Take a long-term view with emphasis on broad, strategic goals and measuring success rather than more narrow, granular elements of the investment program.

- Process. Ensure there is at least some formality to the governance including a structured process for marrying discussion and decision making.

- Transparency. Make sure decisions are documented and provide clarity to owners and beneficiaries into the strategy and choices made, but also for the benefit of advisors executing the investment program.

- Leadership and Succession. Have a defined game plan for leadership and succession that is understood by stakeholders involved in investment governance.

It is normal for families to consider these best practices in more depth as they gain more experience with investment governance.

Conclusion

Governance is a critical part of any family’s investment program. By thinking about people, authority, and process, families can better define their optimal investment governance framework. A well-delineated framework will enhance effective investment decision making. Whether a family is developing an initial governance framework or modifying an existing structure, there are many ways to move forward. An intentional investment governance system that is customized to suit a family’s requirements is imperative to keeping the family aligned with its financial goals.

Private Wealth Strategies team, Private Client Practice