Declaring a Major: Sector-Focused Private Investment Funds

The competitive advantages and resulting return profile of sector specialists should not be ignored when constructing a long-term private equity portfolio

- While it seems clear that a sector specialist should outperform a generalist within their sector of focus, in this paper we introduce data to show that on average sector-focused managers do in fact outperform.

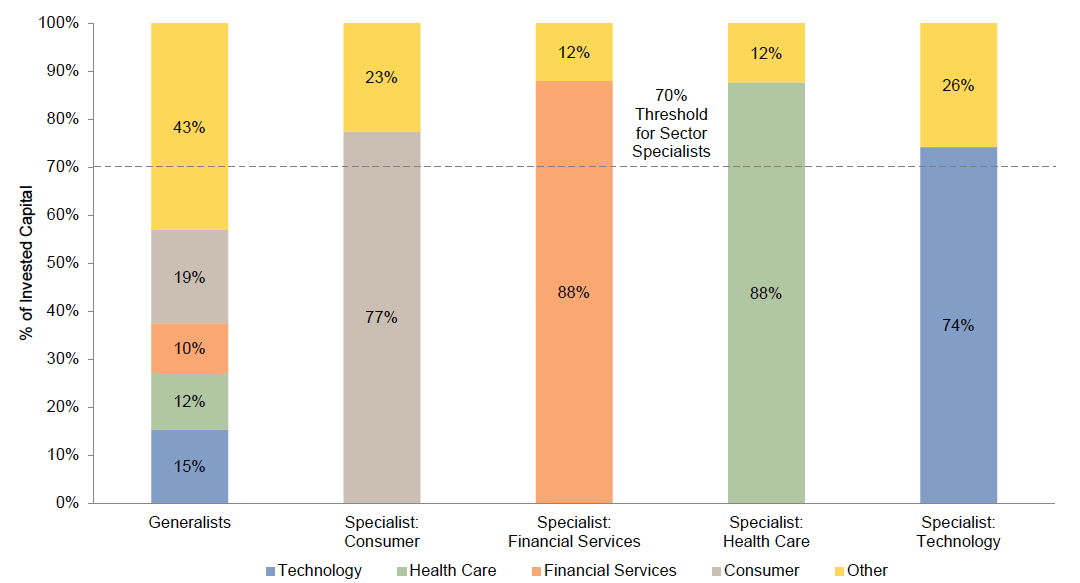

- For the purpose of this analysis, we define sector specialists as managers that have historically invested more than 70% of their capital in one of four sectors—consumer, financial services, health care, and technology—over a ten-year time period (2001–10).

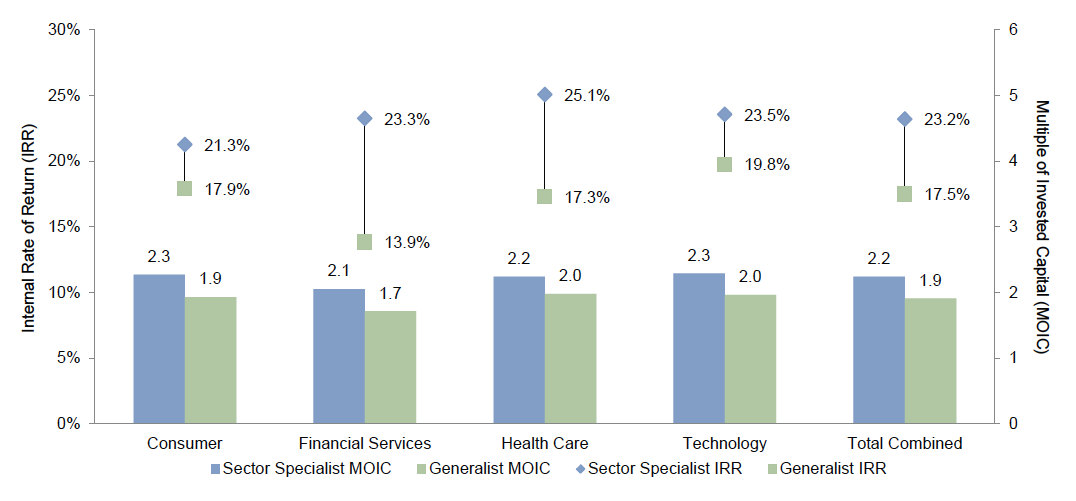

- Investments executed by sector specialists across these four sectors returned an aggregate 2.2 times MOIC and a 23.2% gross IRR, handily outperforming generalist investments that returned an aggregate 1.9 times MOIC and a 17.5% gross IRR.

- Sector specialists have a number of competitive advantages that we believe drive this outperformance: sourcing/portfolio company selection, post-acquisition value add, and exiting investments.

In an increasingly competitive private equity environment, a manager’s ability to demonstrate deep expertise in a focused field has become a key differentiating factor for both limited partners and potential target portfolio companies alike. As a result, the decision of whether to include sector-focused funds in a private investment portfolio is a popular discussion topic with limited partners. While it seems clear that an experienced sector specialist should have a competitive advantage over a less experienced generalist operating within the same sector, the use of sector-focused private equity managers has yet to gain widespread acceptance, despite the long-time use of sector-focused managers within the venture capital asset class. While it is easy to point to a number of factors and assert that investments made by sector-focused managers should outperform generalists within their sector of focus, in this paper we introduce data to show that on average sector-focused managers do in fact outperform on both an internal rate of return (IRR) and multiple of invested capital (MOIC) basis. We also discuss what is driving the outperformance and highlight areas for consideration as limited partners contemplate the inclusion of sector-focused funds in their portfolios.

Major, Minor, or Still Undecided …

The US buyout and growth equity manager universe can largely be sorted into two categories: sector specialists and generalists. For the purpose of this paper, sector specialists are defined as managers that have historically invested more than 70% of their capital in one of four sectors—consumer, financial services, health care, and technology—over a ten-year time period (2001–10). This threshold is purposefully high to identify the pure sector specialists that deploy a substantial amount of their capital within one sector (Figure 1). The remaining managers are considered generalists, which includes everything from true generalists that invest across a wide range of industries to sector-tilted managers that have a “minor” concentration in two to three sectors. To focus in on actual sector-specific investment performance versus fund-level performance, each underlying portfolio investment within the Cambridge Associates US Buyout and Growth Equity benchmark was assigned a sector classification based on Standard & Poor’s Global Industry Classification Standards (GICS). Investments within the four studied sectors represented approximately 60% of the benchmark’s total invested capital during this time period—consumer (19%), technology (18%), health care (12%), and financial services (11%).

Figure 1. Average Sector Exposures: Generalists vs Sector Specialists

As of December 31, 2013

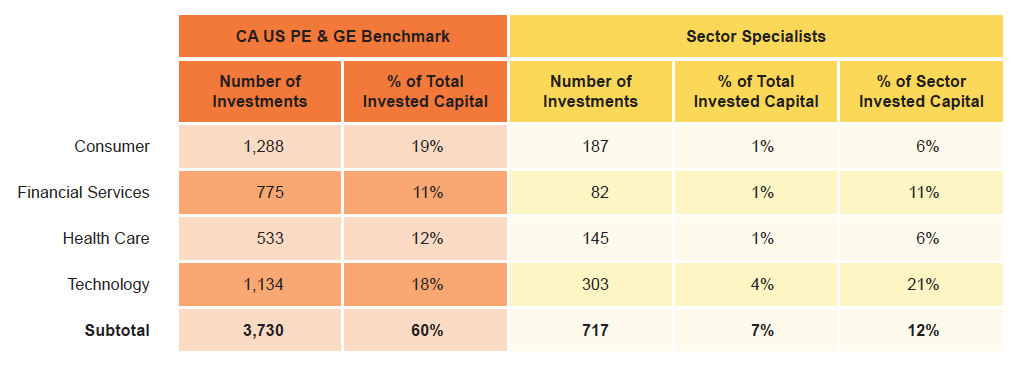

Based on our criteria, the benchmark data contain 717 sector specialist investments across the four studied sectors representing $33 billion of invested capital and 3,013 generalist investments representing $252 billion of invested capital. The greatest number of sector specialist investments was found in the consumer and technology sectors, with 187 and 303 investments, respectively. The sample set was lower in the financial services and health care sectors, with 82 and 145 investments, respectively (Figure 2). In aggregate, sector specialist investments with an initial investment date between 2001 and 2010 represented 12% of total invested capital in these sectors during this time period.

Figure 2. Sector Specialists in the CA US Buyout and Growth Equity Benchmark Data

As of December 31, 2013

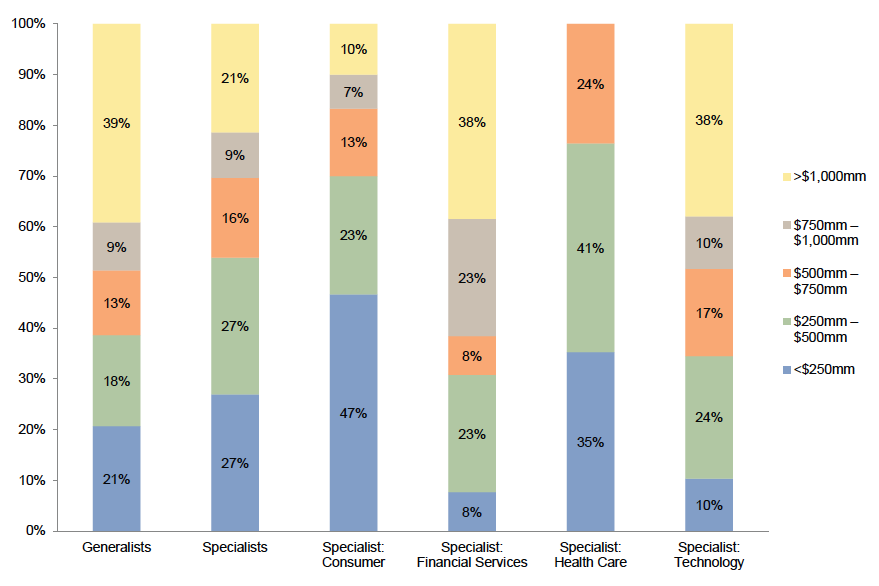

The identified sector specialists are mostly middle-market in size, with 70% of these funds coming in under $750 million in total capitalization. The generalists, on the other hand, vary much more in size, with 48% of funds over $750 million (Figure 3). The smaller size of sector specialists is not unexpected, as we believe these managers have tended to be more judicious in fund sizing and overall organizational growth.

Figure 3. Sector Specialists and Generalists by Fund Size

As of December 31, 2013

Making the Grade

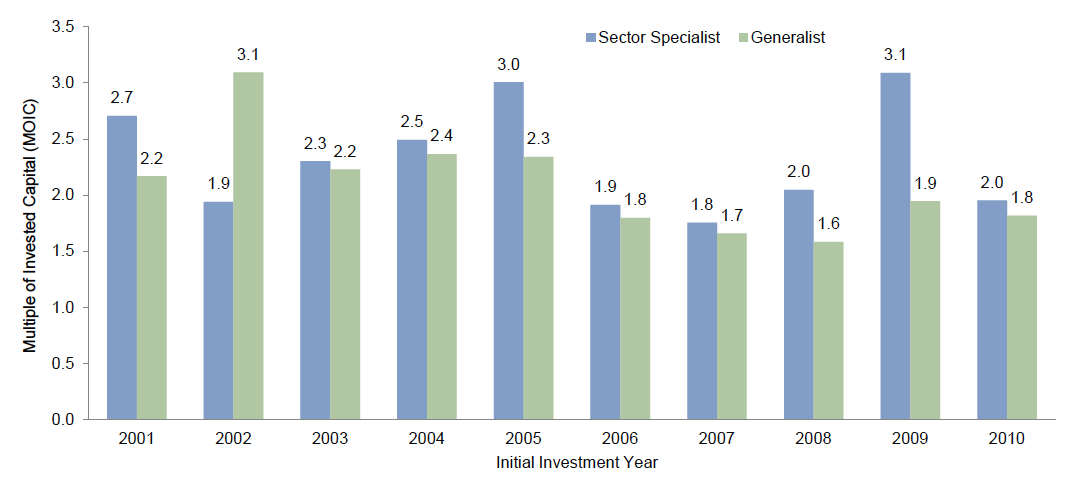

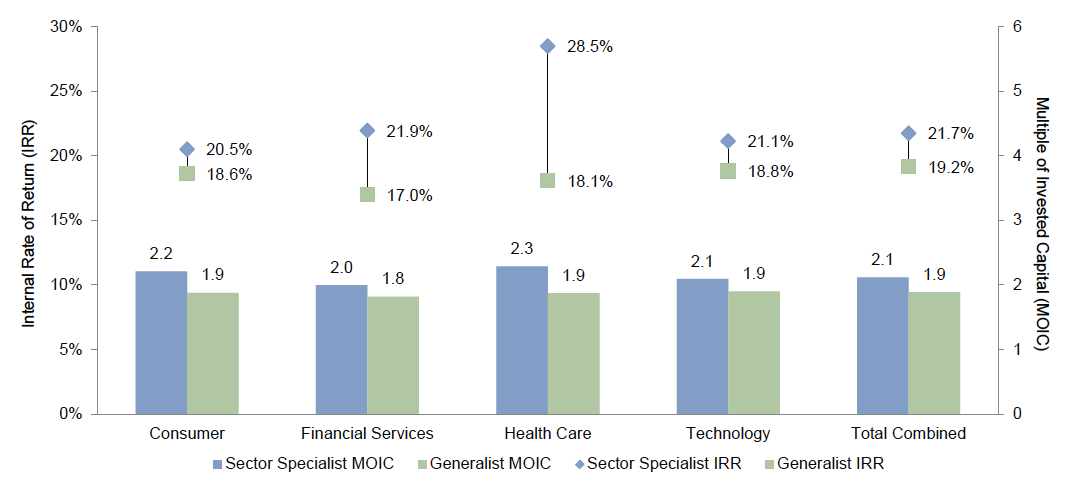

Measuring the performance of all US buyout and growth equity investments across the four sectors that had an initial investment year of 2001 to 2010 shows that investments executed by sector specialists generated an aggregate 2.2x MOIC, handily outperforming generalist investments that generated an aggregate 1.9x MOIC. Specialists also outperformed within each of the four underlying sectors, generating aggregate gross MOICs ranging from 2.1x to 2.3x, compared to generalists that invested in the same sectors and generated aggregate gross multiples of 1.7x to 2.0x (Figure 4). The consistency of sector specialist outperformance is further demonstrated in Figure 5, which shows that aggregate sector specialist investments produced higher MOICs in nine out of the ten years in the study.

Figure 4. Multiple of Invested Capital and Internal Rate of Return for Sector Investments

As of December 31, 2013

Figure 5. Sector Specialist and Generalist MOIC by Initial Investment Year

As of December 31, 2013

Over this time period, sector specialist investments generated a gross IRR of 23.2%, ahead of the generalist investments at 17.5%. Again, the outperformance was seen across all four sectors, with specialist investments outperforming generalist investments by 340 bps to 940 bps in each sector (Figure 4).

Given that limited partners can’t cherry-pick sector investments, we measured the performance of all investments regardless of sector within this time period using the same manager universe. The outperformance by sector specialists persists both at the aggregate level and at the sector level (Figure 6), suggesting that sector specialization has been a more important driver of returns compared to the ability to allocate capital across sectors.

Figure 6. Multiple of Invested Capital and Internal Rate of Return for Total Investments

As of December 31, 2013

Head of the Class

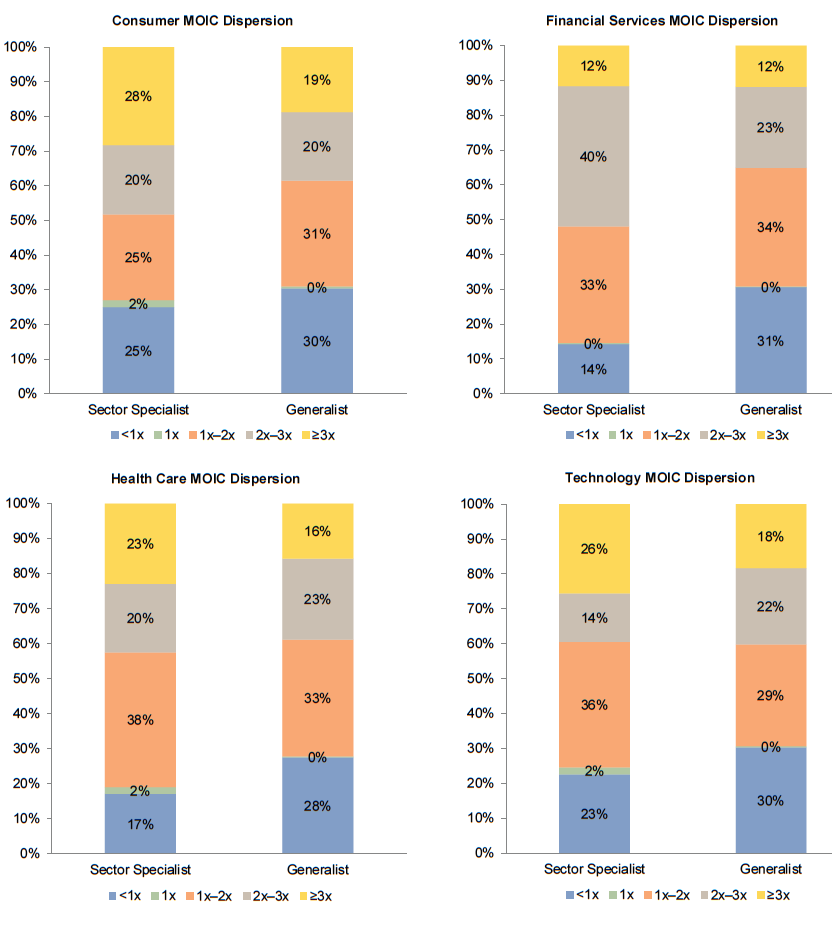

In reviewing the drivers of outperformance, the sector specialists demonstrated a greater ability to minimize capital loss while still achieving significant upside potential. For example, Figure 7 shows that across the four sectors only 14% to 25% of sector specialist capital was in investments valued at less than cost, compared to 28% to 31% for generalist investments. Further, 40% to 52% of sector specialist investments generated a multiple greater than 2.0x, while similarly high-performing investments only accounted for 35% to 40% of generalist investments. In other words, through specialization and domain expertise, the sector specialists appear to be better at avoiding bad investments without hindering their ability to invest in companies that generate outsized returns.

Figure 7. Return Dispersion: Multiple of Invested Capital

As of December 31, 2013

Class Size Doesn’t Matter

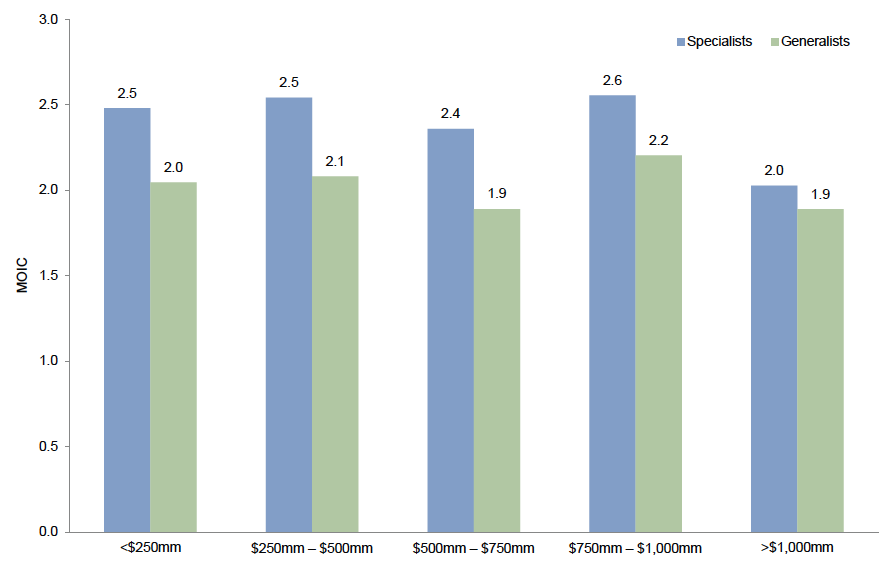

Given specialist firms are more likely to focus on the middle market and raise smaller funds, investors may be quick to assume that the generalist performance is simply hindered by larger fund sizes and a focus on a more efficient part of the market. However, our analysis shows that sector specialist investments outperformed across the spectrum of fund sizes (Figure 8). The spread of sector specialist outperformance does tighten as fund sizes go beyond $1 billion, as the benefits of specialization appear to be somewhat offset in a more competitive market segment. Looking at it another way, when investments are broken down by the size of the investment rather than the fund size, specialist investments also outperform across four different investment size buckets: less than $50 million, $50 million to $150 million, $150 million to $300 million, and greater than $300 million.

Figure 8. Multiple of Invested Capital for Sector Investments Based on Fund Size

As of December 31, 2013

You Wouldn’t Ask Your English Professor for Help on Your Science Project

So what is driving this outperformance? Sector specialists have a number of competitive advantages that we believe form the basis of the demonstrated outperformance:

- Sourcing/portfolio company selection

- Post-acquisition value add

- Exiting investments

The deep domain knowledge, industry contacts, and sheer number of repetitions in a sector leads to higher quality and increased volume of deal flow and better pattern recognition for sector specialists. The focused and dedicated resources that sector specialists can deploy within a sector allow them to be closer to industry participants, trends, and themes that can lead to more attractive and differentiated investment opportunities that generalists firms may overlook, creating at least an advantage and possibly even leading to the elusive proprietary opportunity. These opportunities can be proactively sourced through long-standing and consistent relationships with industry participants. In addition, sector specialists are better equipped to sift through a deal pipeline to identify attractive investment opportunities and avoid the bad ones. The lower impairment ratios of the sector specialists support the view that much of the outperformance generated by specialists is driven by simply avoiding marginal investments. Sidestepping the marginal investment is easier when a manager has the knowledge to discern risk factors to a greater degree than competitors.

Once an investment is targeted, a sector specialist’s reputation of deep domain expertise should also provide greater credibility with the seller and management team that the manager will understand the business and market, be able to efficiently evaluate the investment, and have an edge in post-investment value add. All of these factors should combine to enable the sector-focused manager to develop higher conviction and demonstrate that conviction to all parties involved in the transaction, resonating with key constituencies and possibly creating that angle to prevail.

Post-acquisition, it has become essential to know what to do with a company beyond just the capital structure. Industry-specific operating and strategic skills are equally important drivers of value creation. Sector specialists are better positioned to establish strategic and operational goals to improve company performance; recruit top executives, boards of directors, and industry advisors; develop and monitor key operating metrics; and position a company for sale. In terms of deciding when to exit an investment, sector specialists should be better able to determine the right time to sell based on underlying company and market level fundamentals and can more effectively identify and court potential buyers, both strategic and financial.

Hitting the Hammer/ Nail Issue Head On

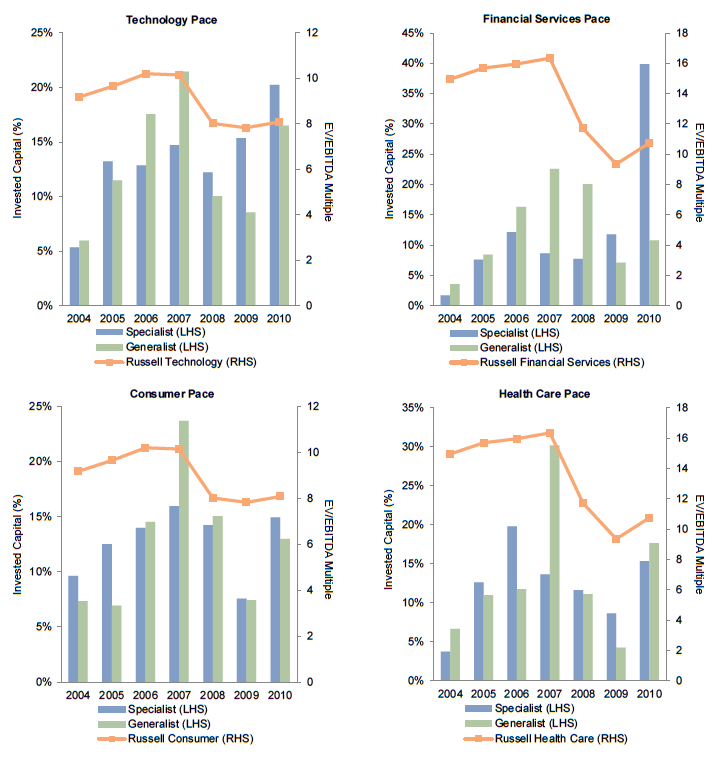

A key concern of investors is that sector-focused funds have to invest within their defined sector of focus, which could lead to capital deployment during unattractive market conditions or into unattractive investment opportunities. With only a hammer in their belt, do all investments look like nails to sector specialists?

Looking at the investment pace of sector specialists and generalists in each sector relative to public market valuations (Figure 9), sector specialists do not appear to be just “buying the market.” Using our data set since 2004, the data show that generalists are more likely to deploy capital into higher valuation environments (based on public market valuations as a proxy) within each sector, while specialists have shown more discipline through different valuation cycles. While the narrower focus of sector specialists should not be overlooked in terms of overall portfolio construction, the typical five-year investment period to deploy capital in private strategies allows specialists flexibility to navigate different market conditions.

Figure 9. Calendar Year Investment Pace Compared to Public Market Valuations

As of December 31, 2013

With that said, don’t expect every hammer to nail it. Investors don’t have to look far to find sector-focused funds that have underperformed for any number of reasons. Careful manager selection and evaluation remains critical. When a given sector is having a moment, it is not unusual for a crop of sector-focused funds to come to market to absorb interested capital. Take pains to understand the longevity of the sector’s overall investment opportunity, the length of time the manager has been active in the sector, and the relevance of the manager’s track record. Test the manager’s thoughtfulness and investment philosophy. For investors with existing exposures to sector-focused managers, careful monitoring during periods of sector volatility and disruption is also key in determining the longevity of the manager’s advantages within the sector.

Declare Yourself

When evaluating investments in sector-focused funds, limited partners need to determine at what level they need to be diversified—fund level, asset class level, or portfolio level. With the benefit of a well-diversified public investment program, the risk of sector concentration within the private portfolio due to the use of a sector specialist is more easily mitigated. Many limited partners will need to reconcile the tension between reducing the number of private manager relationships and the need to commit to more sector-focused managers to achieve the desired level of diversification in pursuit of more compelling returns. While we used a purposefully high threshold to identify sector specialists in this paper, we believe the results can be used to inform the evaluation of managers across the specialization spectrum. It is reasonable for investors to be undecided as there are many ways to be successful in private equity; however, the private equity market will only get more competitive, and the competitive advantages and resulting return profile of sector specialists should not be ignored when constructing a long-term private equity portfolio.

Average Sector Exposures: Generalists vs Sector Specialists

Source: Cambridge Associates LLC.

Notes: Data represent realized and unrealized investments within the Cambridge Associates US Buyout and Growth Equity Benchmark initiated between 2001 and 2010. For research purposes, sector specialists are defined as managers who have historically invested more than 70% of their capital in one of four sectors—consumer, financial services, health care, and technology. All other manager within the US buyout and growth equity benchmark are considered generalists.

Sector Specialists in the CA US Buyout and Growth Equity Benchmark Data

Source: Cambridge Associates LLC.

Notes: Data represent realized and unrealized investments within the Cambridge Associates US Buyout and Growth Equity Benchmark initiated between 2001 and 2010.

Sector Specialists and Generalists by Fund Size

Source: Cambridge Associates LLC.

Notes: Data represent funds with realized and unrealized investments within the Cambridge Associates US Private Equity Benchmark initiated between 2001 and 2010. Percentages based on the number of funds.

Multiple of Invested Capital and Internal Rate of Return for Sector Investments

Source: Cambridge Associates LLC.

Notes: Data represent realized and unrealized investments within the Cambridge Associates US Buyout and Growth Equity Benchmark initiated between 2001 and 2010. MOICs and IRRs are based on the aggregate performance of investments categorized as sector specialist or generalist. All performance is gross of fees and expenses.

Sector Specialist and Generalist MOIC by Initial Investment Year

Source: Cambridge Associates LLC.

Notes: Data represent realized and unrealized investments within the Cambridge Associates US Buyout and Growth Equity Benchmark initiated between 2001 and 2010. MOICs are based on the aggregate performance of investments categorized as sector specialist or generalist. All performance is gross of fees and expenses. Sectors represented include consumer, financial services, health care, and technology.

Multiple of Invested Capital and Internal Rate of Return for Total Investments

Source: Cambridge Associates LLC.

Notes: Data represent realized and unrealized investments within the Cambridge Associates US Buyout and Growth Equity Benchmark initiated between 2001 and 2010. MOICs and IRRs are based on the aggregate performance of all investments, regardless of sector, that were executed by the managers identified as specialists and generalists in each sector. All performance is gross of fees and expenses.

Return Dispersion: Multiple of Invested Capital

Source: Cambridge Associates LLC.

Notes: Data represent the MOICs of realized and unrealized individual investments within the Cambridge Associates US Buyout and Growth Equity Benchmark initiated between 2001 and 2010. All performance is gross of fees and expenses.

Multiple of Invested Capital for Sector Investments Based on Fund Size

Source: Cambridge Associates LLC.

Notes: Data represent realized and unrealized investments within the Cambridge Associates US Buyout and Growth Equity Benchmark initiated between 2001 and 2010. MOICs are based on the aggregate performance of investments categorized as sector specialist or generalist. All performance is gross of fees and expenses.

Calendar Year Investment Pace Compared to Public Market Valuations

Sources: Cambridge Associates LLC and Frank Russell Company.

Notes: Data represent calendar year cash fl ows for investments within the Cambridge Associates US Buyout and Growth Equity Benchmark initiated between 2001 and 2010. Index data provided by Frank Russell Company. Outliers were identified and excluded from the public company universes.

Josh Zweig - Josh Zweig is a Co-Head of North American Private Equity Research and a Partner at Cambridge Associates.

Andrea Auerbach - Andrea Auerbach is the Global Head of Private Investments and a Partner at Cambridge Associates.

About Cambridge Associates

Cambridge Associates is a global investment firm with 50+ years of institutional investing experience. The firm aims to help pension plans, endowments & foundations, healthcare systems, and private clients achieve their investment goals and maximize their impact on the world. Cambridge Associates delivers a range of services, including outsourced CIO, non-discretionary portfolio management, staff extension and alternative asset class mandates. Contact us today.