Private Credit Benchmarks: A User’s Guide

In response to the proliferation of new private credit strategies and managers, Cambridge Associates (CA) has developed a set of benchmarks that will help limited partners (LPs) assess the performance of new and existing fund managers (general partners or GPs). While CA already offered benchmarks of distressed and junior debt funds with data dating back to the late 1980s, the introduction of new, different strategies requires specialized benchmarks. The new private credit benchmarks rely on the same data as all of CA’s other private benchmarks. GPs report annual and quarterly financial statements, as well as cashflows to CA, and we then calculate quarterly, horizon, and since-inception returns based on the same methods used historically in benchmarking other private strategies. 1 CA believes that this consistency supports comparison not only within the very broad private credit asset class, but also among other private asset classes, and thus should underpin superior asset allocation decisions.

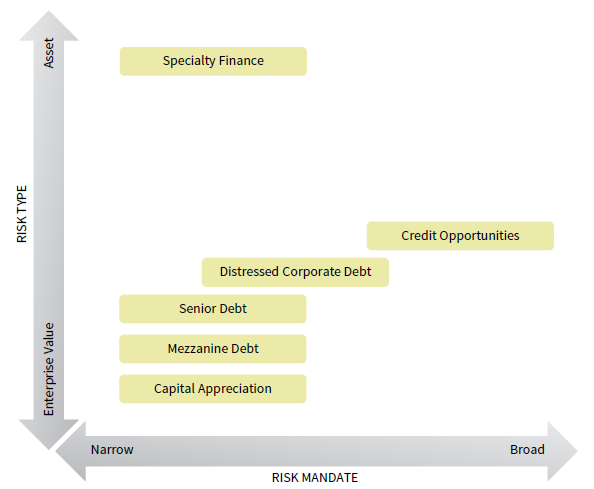

In devising the private credit benchmarks, CA sought to aggregate funds based on the type and level of risk assumed in a given strategy’s mandate (as opposed to mandates regarding geography or sector that, admittedly, carry their own type of risks) and underlying collateral. For example, some funds have a broad mandate that allows them to assume senior, junior, or even equity risk in corporate entities or single assets, while others have narrower risk mandates limiting investments to junior or senior credit or to primarily corporate or single-asset risk. Finally, CA seeks to group strategies that assume primarily corporate enterprise value (EV) risk separate from those that assume asset risk. Naturally, some broad mandates permit managers to take both types of risks, complicating categorization.

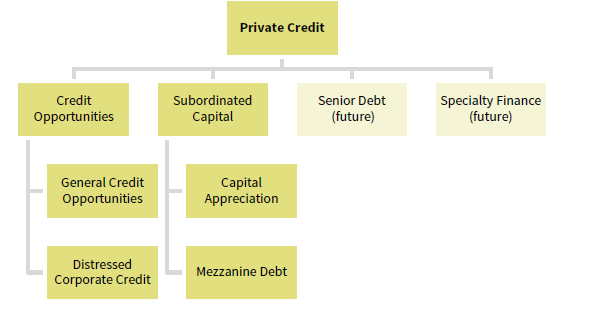

Today, the umbrella private credit benchmark comprises two narrower benchmarks, credit opportunities and subordinated capital.

PRIVATE CREDIT MATRIX: RISK AND BREADTH

Source: Cambridge Associates LLC.

The Broad Benchmark and Its Components

The general private credit benchmark is home to all strategies classified by CA as private credit. 2 It is home to the funds that are found in the credit opportunities and subordinated capital benchmarks.

PRIVATE CREDIT BENCHMARKS

Source: Cambridge Associates LLC.

The credit opportunities benchmark is home to more than 200 funds and dates back to 1988. It comprises two similar, yet distinct strategies: distressed corporate credit and general credit opportunities. Distressed strategies in the credit benchmark are those that can be categorized as “sprinters” or “milers,” as described in “Distressed Debt: A New Way to Categorize Managers.” 3 Distressed managers tend to purchase discounted debt obligations, such as bank loans, bonds, or other claims across the corporate capital structure (on a traded exchange, through an intermediary, or directly from existing creditors). These managers are adept at identifying the fulcrum security, or those securities senior to the fulcrum, helping them to maximize risk-adjusted returns. Most importantly, they are comfortable assuming the risks surrounding contentious restructurings, litigation, valuation, and negotiation. Managers in these strategies are comfortable taking either EV or specific asset risk.

Unlike distressed strategies, the general credit opportunities funds within the credit opportunities benchmark tend to originate and structure performing, direct credit instruments across the capital structure. These managers are adept at drafting their own documents and are comfortable assuming either EV risk or specific asset risk. However, they will also generally control an entire tranche of debt and offer bespoke terms and conditions in an attempt to minimize the risks of valuation, litigation, and restructuring embraced by their distressed-oriented counterparts. Nevertheless, during a credit cycle, they may flex into pure distressed investing. Outside of a credit cycle, however, credit opportunities managers will generally have more direct contact with borrowers and other creditors and will frequently be considered a “capital solution” to an acute liquidity need, lender fatigue, etc. 4

The subordinated capital benchmark includes more than 200 funds and dates back to 1986. It also comprises two types of strategies: regular way, sponsor-oriented mezzanine and capital appreciation. The mezzanine strategy includes lenders that make loans (either mezzanine or second-lien) that are junior in priority to a senior lender. These lenders almost always assume more EV risk; for example, as hard asset collateral is typically encumbered by a first priority lien enjoyed by the senior lender and, in general, lenders’ documents tend to lack the many protections enjoyed by senior lenders. In general, the key sources of return for mezzanine managers are coupon payments. While equity exposure is not uncommon, its contribution usually does not exceed that of coupon payments.

Capital appreciation strategies within the subordinated debt benchmark delve a little deeper into the capital structure, targeting greater returns by assuming more EV risk via directly originated preferred equity or deeply subordinated debt. Managers pursuing a capital appreciation strategy will typically generate returns through both current payment instruments as well as non-control participation in EV growth. In general, equity participation can take the form of warrants or conversion rights as well as creatively structured terms such as success fees or revenue sharing.

CA is also working with credit GPs to add two additional strategies to the broad private credit benchmark (these strategies currently lack a sufficient number of managers to constitute a meaningful benchmark): senior debt (commonly referred to as direct lending) and specialty finance. Senior debt will include regular way, sponsored and unsponsored direct lending strategies, which will be further delineated as either levered or unlevered. The specialty finance benchmark will include all managers that originate or buy (typically through bilateral purchases) debt obligations backed by assets. 5 In addition, the specialty finance strategy will include corporate, retail, and some real estate nonperforming loans (NPLs). Finally, the specialty finance category will also house certain hard asset leasing strategies that directly own assets such as aircraft or railcars that are then leased to transportation companies. While ownership of operating assets typically would slot a strategy into an equity benchmark, we plan to classify these as credit strategies primarily because asset ownership is divorced from control, functioning more as credit enhancement similar to a lien filed under the relevant laws, such as the Uniform Commercial Code in the United States.

Overlaps, Intersections, and Dilemmas

The descriptions listed above hint at intersections, where funds in one specific benchmark may occasionally puruse investments more commonly found in another strategy’s benchmark. This creates dilemmas as to where a fund should reside. If a fund has 70% of its assets in senior secured, performing corporate debt, should it be categorized as a senior debt fund? It certainly should if its mandate requires a minimum of 70% of its assets be invested in such instruments. But the conclusion is less obvious if the GP has a mandate to pursue opportunities across the capital structure but has elected to be overweight senior secured performing credit.

CA recognizes that dilemmas may arise, but believes that our focus on the strategy’s inherent risk is sound for two reasons. First, there is no real credible alternative. Fund classifications based on a resulting portfolio or its returns are unhelpful when allocating capital. Relying on the resulting portfolio to determine strategy prohibits benchmarking until the manager is fully invested. If the manager in the example above has a broad mandate, then categorizing it would be impossible until after the GP has decided that senior secured performing credit offers the best risk-adjusted returns and successfully constructed a portfolio. Similarly, focusing on returns presupposes that GPs are assuming risk commensurate with a generated return. A fund generating a 8% net internal rate of return could be a strong or weak direct lender (depending on leverage) or a strong or weak distressed manager (depending on the opportunity set). Second, a broad strategy can be viewed as another dimension of return generation. Funds with broader mandates enjoy the additional benefit (or challenge) of selecting the security, sector, or exposure that offers the best risk-adjusted return at a given point in the credit cycle. More risk-constrained funds must seek the best returns in a narrower opportunity set. Grouping together broad mandate funds separately from narrower mandate funds helps benchmark the GPs’ prowess in exploiting the opportunity set; a skill less easily exercised in more constrained strategies.

Conclusion

The new set of private credit benchmarks should improve performance analysis and manager selection. By focusing on the underlying risks assumed by a credit manager, the subordinated capital and broad credit opportunities benchmarks will assist LPs in better evaluating risk-adjusted performance and identifying the most talented managers. The roster of funds within these benchmarks will grow as returns season, GPs launch new funds, and new GPs elect to report into the benchmarks. CA is also striving to develop the nascent specialty finance and senior debt benchmarks into fully fledged reported benchmarks.

Footnotes

- CA calculates returns based on GP-provided financial statements, compares them with GP-reported returns, and then works with GPs to reconcile any differences. CA’s benchmarks are aggregated; we disguise GP data, and GPs that contribute to the indexes determine which, if any, of CA’s LP clients may access their data.

- Private credit refers to credit strategies pursued in illiquid vehicles commonly described as drawdown vehicles, private equity–style vehicles or lock-up vehicles. These vehicles offer no demand liquidity, have defined investment and harvest periods, and finite lives.

- “Marathoners,” usually control-oriented distressed managers, are instead covered by CA’s private equity team and reside within our private equity benchmarks because we believe that those managers’ ownership and control more closely resemble the strategy of an equity fund than a debt fund. Unlike most credit funds, control-oriented distressed funds assume greater operational and strategic risks in turning around, managing, and exiting businesses.

- CA also has a distressed securities benchmark that combines funds in the credit opportunities benchmarks (found within private credit) and control-oriented distressed (found in private equity) benchmarks.

- Assets could be real, such as trucks or aircraft, or esoteric assets, such as consumer loans or life settlements.

About Cambridge Associates

Cambridge Associates is a global investment firm with 50+ years of institutional investing experience. The firm aims to help pension plans, endowments & foundations, healthcare systems, and private clients achieve their investment goals and maximize their impact on the world. Cambridge Associates delivers a range of services, including outsourced CIO, non-discretionary portfolio management, staff extension and alternative asset class mandates. Contact us today.