The Private Credit Playbook: Understanding Opportunities for Family Investors

Today, private investors and wealthy families are facing uncertainties related to economic growth, inflation, interest rates, and private investment exit opportunities. Yet, these same market challenges are serving as tailwinds for certain asset classes, including private credit. In today’s environment, we believe private credit can deliver attractive returns, supported by a strong foundation in protected assets and faster capital deployment than other private growth assets. This paper presents an overview of the asset class and a discussion of how family investors can implement this strategy effectively in their investment portfolios.

What Is Private Credit?

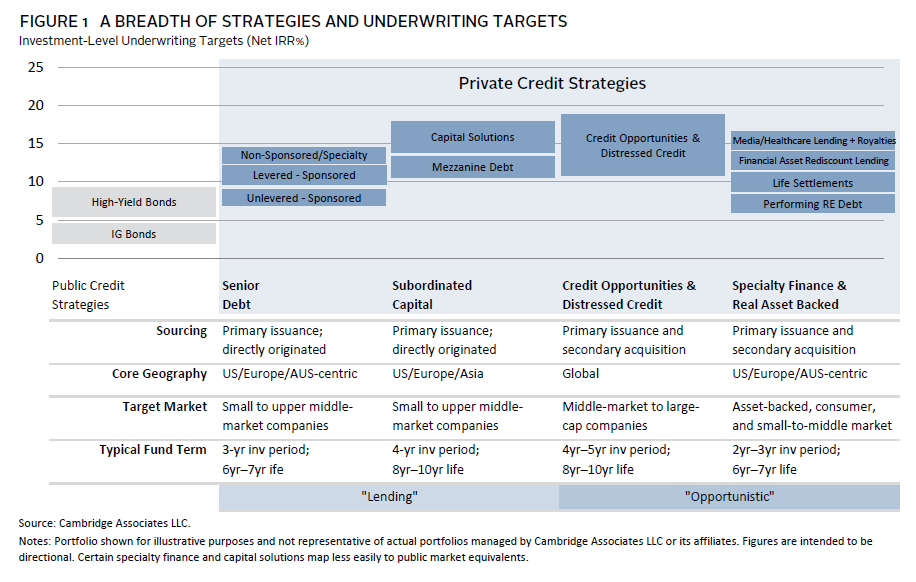

Private credit investments are non-publicly traded investments provided by non-bank entities that fund private businesses. These investments encompass a wide range of strategies, including senior debt, subordinated capital, credit opportunities, distressed credit, and specialty finance, each with distinct features. At a high level, private credit consists of two distinct categories—lending and opportunistic (Figure 1).

Private credit strategies offer higher yields than traditional fixed income, with low correlations to both liquid corporate/municipal bonds and equity markets. In addition, private credit involves bespoke terms and structures that can offer ongoing cash yield and charges fees on invested rather than committed capital. Both elements help to mitigate a portfolio’s private investment J-curve impact. 1

Lending Strategies

Lending strategies offer money to borrowers for periods ranging from short to medium term, usually between three and five years. These loans often come with variable interest rates that can change over time. These strategies can be particularly appealing when the loans are for shorter periods and the lender has a priority claim on the borrower’s assets in case of default. Furthermore, many lending funds have provided attractive returns that are not closely linked to changes in interest rates—through self-liquidating investments that are designed to pay themselves off within a three-year period. In 2022, for example, these strategies generated strong positive returns, while liquid high-quality bonds (e.g., US government, corporate, municipal, mortgage) were all down more than 10%.

Private lending strategies feature privately negotiated, senior structured debt and traditionally generate a 8%–10% net unlevered returns per annum. The deals usually include contractual payments, high-quality collateral, enforceable covenants, and bankruptcy remote structures to control and disburse cash from interest payments and fees. Based on our experience, lending strategy managers can currently achieve 10%–12% net 2 unlevered returns, benefiting from elevated base rates and reduced competition from traditional bank institutions.

Opportunistic Strategies

Opportunistic credit investments employ higher return and higher risk strategies by providing companies with a broader set of capital solutions relative to lending-only strategies. These funds fall between each end of the risk spectrum—from traditional direct lending to control-oriented distressed. Credit opportunity and specialty finance funds invest in instruments such as secondary market bonds and loans, directly originated loans with warrants, and structured equity solutions. These funds typically target net returns in the 12%–15% per annum range. We believe they have the potential to deliver even higher returns during periods of market stress when traditional capital sources are less widely available. For example, many opportunistic credit funds preserved capital with positive returns from interest and fees in 2022, offsetting modest marked-to-market losses amid broader interest rate uncertainty.

Combining Lending and Opportunistic

Investors can also create a blend of lending and opportunistic private credit approaches with the potential to target net returns more than 12% per annum. In many cases, we believe a blended private credit program can provide investor a balanced source of returns, with current income received sooner and the opportunity for higher returning assets over medium- to long-duration periods. In these balanced programs, the distributions and return of capital from the lending strategies can also be used to fund capital calls for longer lock-up, opportunistic credit funds with longer investment periods and fund life.

Current Opportunities for Private Investors

The current investment environment presents a unique set of private credit opportunities for families and private wealth investors. Traditional banks have become more cautious about lending due to mixed economic forecasts and interest rate uncertainty. This caution is partly because some borrowers, especially in commercial real estate and corporate debt, are facing difficulties due to higher interest costs, particularly with floating rate loans. Some of these borrowers are finding it harder to refinance their debts at reasonable costs and struggling to sell off loans without incurring significant losses. Consequently, banks are reserving more funds to cover potential losses and are being very careful about issuing new loans, leading to reduced loan activity and less money available for borrowers. As a result, private credit funds have emerged as a critical source of financing, especially for mid-sized companies that are often overlooked by larger financial institutions. These funds are stepping in to fill the gap, providing much-needed capital in a tighter lending environment.

Second, in a market characterized by volatility and ambiguity, private credit offers a relatively stable investment option due to its secured nature and structured returns. Engaging in direct lending opportunities can allow for more customized deal structuring, providing both protection and flexibility. This can include negotiating stronger covenant protections or opting for asset-based lending to further secure investments. Investors may also want to explore opportunities in distressed debt markets. Economic downturns and market dislocations can create attractive entry points for investors with the expertise to navigate these complex situations, potentially leading to outsized returns as markets recover.

Last, it’s crucial for private investors and wealthy families to partner with experienced fund managers who not only have a proven track record in private credit but also possess deep sectoral expertise and the ability to conduct thorough due diligence. We believe partnering with an investment advisor with deep private credit research capability is instrumental in uncovering hidden gems and avoiding pitfalls in this nuanced space.

Understanding Key Risks

While private credit offers attractive benefits, it is important to be aware of its inherent risks. These risks include: illiquidity, constrained upside potential compared to private equity, manager selection, and tax inefficiency.

Depending on the strategy, private credit investments can involve capital lock-ups of three to ten years. Although slightly more liquid than other private investments, private credit investors need to be prepared to commit for the long term. What’s more, unlike the high-growth potential of private equity, private credit strategies often come with fixed returns—or return levels in which the upside is capped. While this can result in more stable returns with lower risk relative to other private investments, it represents a ceiling on how much a strategy can earn.

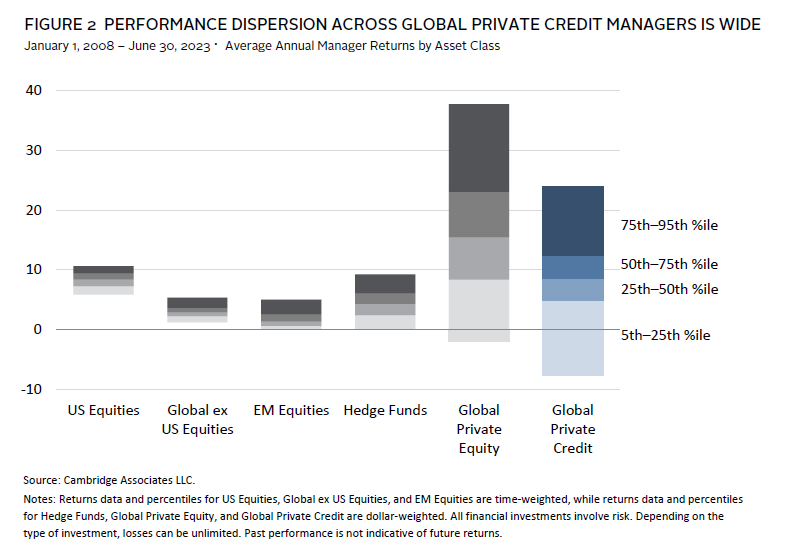

As with all private market investments, performance dispersion in private credit is wide (Figure 2). In some cases, steady returns might mask underlying challenges, including borrowers that have limited credit histories. We believe success in private credit investing comes from partnering with managers that have a proven track record, expertise in assessing credit risk, and a history of recovering investments. Selecting top-tier managers is essential for tapping into the full potential of private credit and earning an illiquidity premium.

Lastly, tax inefficiency poses a notable challenge for private and family investors in private credit. This issue arises because the interest income generated from private credit investments is often taxed at higher ordinary income rates, rather than the lower capital gains rates applicable to some other types of investments. This can significantly reduce the net returns that investors receive, especially for those in higher tax brackets. The complexity of the investment structures within private credit can also further complicate tax matters, requiring careful planning and management to meet the tax obligation. Understanding and navigating these tax implications can help maximize the efficiency and overall returns of private credit investments (see “Managing Tax Implications”).

Managing Tax Implications

When it comes to private and family investors, taxes are a critical input for investment decisions. Given their higher income orientation, private credit investments are less tax efficient than investments focused on long-term capital gains. Private credit strategies will have different tax considerations depending on the tax domicile of each investor.

Working with an experienced investment advisor to build a diversified program with different sources of return can help improve tax efficiency. To improve tax efficiency, thoughtfully incorporating different strategies into a diversified program is critical. For example, lending strategies with higher income orientations can be paired with opportunities funds that have greater capital gain potential. Investing in certain tax-favored vehicles also may offer solutions in some situations.

Understanding the tax trade-offs specific to each investor’s unique situation before committing to any investment is essential.

Implementation: Things to Consider

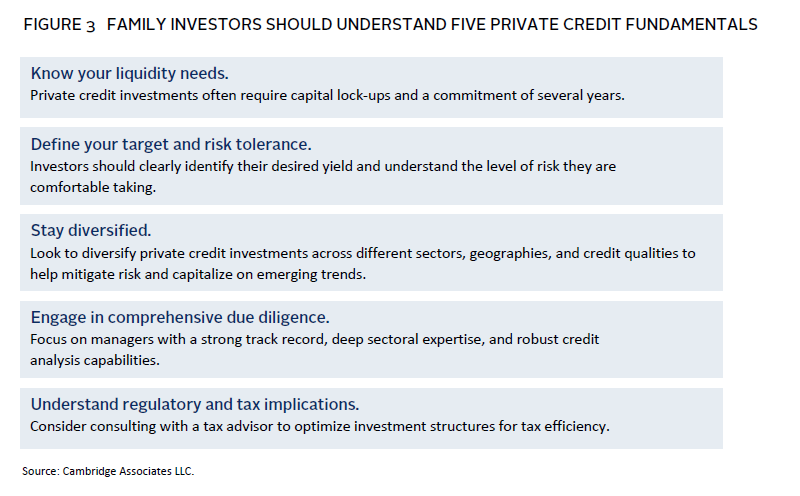

To take advantage of attractive yield opportunities available in private credit, family and private investors should carefully consider several key implementation factors (Figure 3). First, liquidity needs are an important consideration, given the illiquid nature of many private credit investments, which may not be easily sold or converted to cash. The longer commitments required of some private credit investments make them more suitable to investors with a longer-term outlook that have a clearly defined target yield. Determining this target requires a close assessment of risk tolerance, as higher yields often come with higher risks.

Diversification is another key aspect of private credit implementation. Investors should consider diversifying their private credit portfolios across sectors that demonstrate resilience and growth potential, such as technology, healthcare, and renewable energy. A diversified approach can help spread risk across various sectors and credit qualities while capitalizing on emerging trends.

Robust due diligence is also imperative. Understanding the borrower’s ability to meet its debt obligations is paramount to mitigating default risks. Market conditions continually influence the availability of opportunities and the risk/return profile of private credit investments. Staying mindful of regulatory and tax policy changes is also important, as these can impact investment structures, compliance requirements, and overall returns.

When implementing private credit strategies, private investors and wealthy families often have a flexibility advantage. They can allocate more nimbly than other large investors, such as pensions or endowments, and are thus well positioned to take advantage of the current robust opportunity set. Flexible asset class definitions and target ranges can likewise allow them to allocate more opportunistically. For instance, credit opportunity funds that target higher returning assets can be sourced from traditional private investment allocations. But private investors and wealthy families can also consider a wider range of capital sources. They can, for example, position lending strategies within a portfolio as part of a fixed income or diversifier allocation, helping to smooth returns and provide protection in adverse market environments. For investors building new private growth sleeves, private credit can provide another option for generating risk-managed alpha.

Giving Private Credit its Due

Private credit investments have experienced a rapid evolution over the past decade. In fact, the private credit landscape has changed so much that investors that last explored it ten or more years ago may not recognize it today. Market conditions have helped to shape what may be a particularly auspicious cycle for the asset class. Higher interest rates and changing credit market dynamics have created attractive opportunities for private investors and wealthy families—but proper due diligence and implementation is essential. Allocations to private credit can be additive to overall portfolio positioning, serving as a complimentary source of growth and income generation along with strong downside protection. Ultimately, a customized approach to private credit that accounts for liquidity and tax challenges may be the best path for investors seeking a consistent income source that is less correlated to traditional fixed income and equity markets.

Footnotes

- A J-curve is an early period characterized by negative returns and cash flows, as investments are initially made and develop over time before they are in a position to be sold.

- All financial investments involve risk. Depending on the type of investment, losses can be unlimited. Past performance is not indicative of future returns.

Wilbur Kim, CFA - Wilbur Kim is a Partner for the Private Client Practice at Cambridge Associates.

Buck Reynolds, CFA - Buck Reynolds is a Senior Investment Director for the Private Client Practice at Cambridge Associates. Buck advises families, family offices, and other sophisticated institutional investors on all topics related to portfolio management. This includes portfolio strategy, custom portfolio construction, asset allocation, and manager evaluation and selection across asset classes. At CA, Buck takes an active […]

About Cambridge Associates

Cambridge Associates is a global investment firm with 50+ years of institutional investing experience. The firm aims to help pension plans, endowments & foundations, healthcare systems, and private clients achieve their investment goals and maximize their impact on the world. Cambridge Associates delivers a range of services, including outsourced CIO, non-discretionary portfolio management, staff extension and alternative asset class mandates. Contact us today.