2024 Outlook: Currencies

We expect the US dollar and gold will more or less hold their values, given our economic expectation and the many geopolitical risks. We believe the yen will appreciate, and we expect the thawing crypto winter will fully transition to a spring.

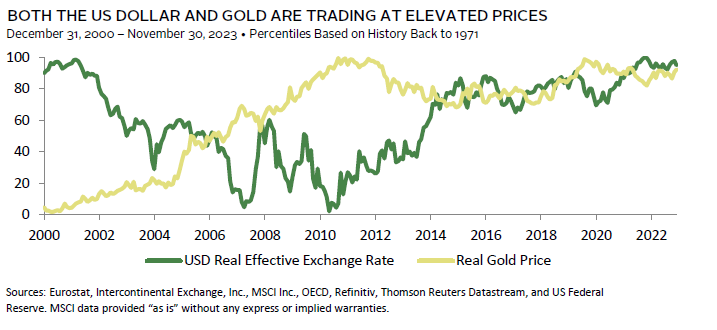

The US Dollar and Gold Should Hold Their Value in 2024

Sean Duffin, Senior Investment Director, Capital Markets Research, and Thomas O’Mahony, Senior Investment Director, Capital Markets Research

The US dollar and gold are both stores of value and tend to do well in periods of turmoil. Despite this reality, as well as our views that economic activity will be weak in 2024 and that equity market volatility will increase, we expect that prices of these assets will remain range bound.

The dollar’s best days are likely already behind it for this currency cycle, following the run-up that climaxed in September 2022. Looking forward, the path of least resistance for the greenback over the next five-year period is for it to depreciate from its current elevated real valuation. The currency is currently benefiting from wide interest rate differentials versus its peers, expectations of continued US economic outperformance, and risk aversion. The unwinding of any of these factors against a more normalized macroeconomic backdrop could precipitate dollar weakening.

Nonetheless, it may be premature to expect these supportive factors to dissipate in 2024. Consensus US growth outperformance versus the Eurozone and United Kingdom for 2024 is relatively modest and could improve, given the headwinds Europe faces. Relatedly, the Fed likely has the strongest claim to genuinely needing to keep rates higher for longer. And even if conditions in the United States continue to deteriorate, the flight-to-safety effect the US dollar enjoys may initially mitigate the impact of reduced growth and rate differentials. Therefore, 2024 looks more likely to deliver bounded dollar performance than a surge higher or lower.

Like the dollar, we expect gold’s performance will not stand out. Recently, geopolitical tensions and central bank buying have supported its price, but we believe its recent rally likely means that it is already pricing in an uptick in geopolitical risk and market volatility next year. With real yields now trading at their highest levels since the GFC and our view that the Fed will only modestly cut its policy rate in 2024, the opportunity cost of holding a non-interest-bearing asset like gold will remain high, making tactical gold positioning funded from assets like cash more difficult to tolerate.

There are several catalysts that could spark another strong year of performance for both gold and the dollar, such as unexpected escalation in geopolitical conflicts or an equity market meltdown, but we consider those catalysts as tail risks.

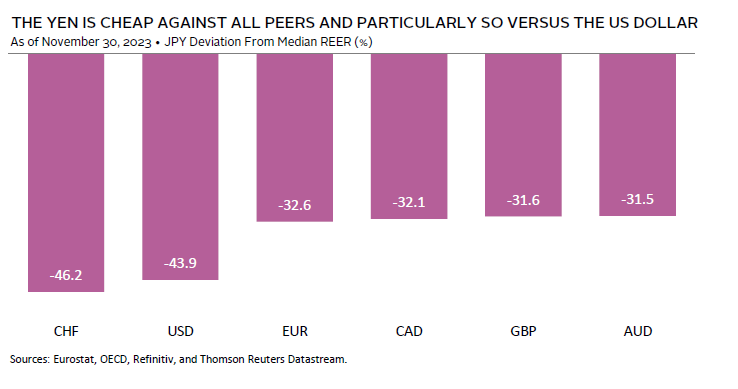

The Yen Should Appreciate in 2024

Thomas O’Mahony, Senior Investment Director, Capital Markets Research

The Japanese yen has weakened persistently since the beginning of 2021. Indeed, the most recent sell-off has taken the valuation of the yen to historically cheap levels. Our calculations show the currency’s real valuation versus the dollar is lower than 99% of observations back to June 1971. Monetary policy divergence lies at the heart of the yen’s decline. The post-COVID surge in inflation occurred sooner and more forcefully among Japan’s peers, with material monetary tightening being delivered. Japan, by contrast, maintains a negative policy rate.

The rise in inflation in Japan is undeniable, however, with Bank of Japan (BOJ) core inflation (excluding fresh food and energy) currently at 4.0%, the highest since the early 1980s. The only response so far from the BOJ has been to widen the bands of its Yield Curve Control (YCC) 1 policy. The relative lack of wage pressure has so far stayed the BOJ’s hand, as it retains concerns about the persistence of current inflation rates. Nonetheless, wage pressures are at the high end of the range of the last three decades and the labor market looks tight by most metrics. With core inflation having been above target for nine months and economic activity coming in firmer than in most of its peers, pressure is likely to build in 2024 for further monetary tightening.

While any further BOJ tightening is likely to be modest in comparison to other regions, it should be sufficient to drive some yen appreciation. It would reduce the currency’s negative carry, making it less onerous for those wishing to express a positive JPY view, and less beneficial to those using the yen as a funding currency. There are, of course, scenarios in which the BOJ does not deliver any further tightening. One of the most likely would be in the event of a more severe global economic slowdown. However, in this scenario, other central banks would be aggressively cutting interest rates, causing interest rate differentials to move favorably for the yen. While other scenarios could play out, the balance of risks appears skewed toward an appreciating JPY in 2024.

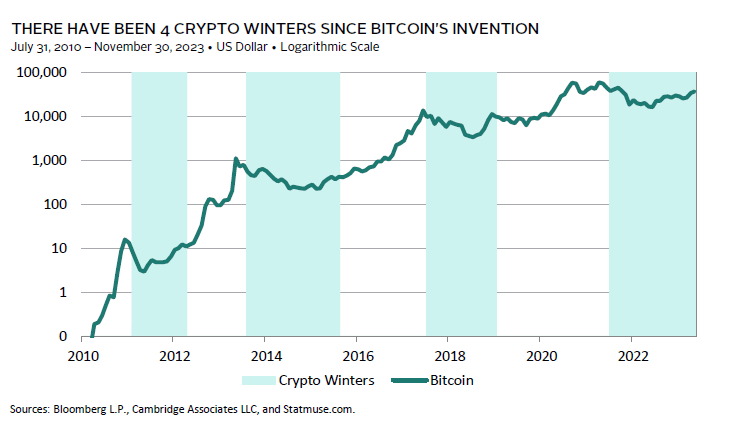

The Crypto Winter Should Transition to Spring in 2024

Joe Marenda, Head of Hedge Fund Research and Digital Assets Investing

Digital assets were in a so-called crypto winter from mid-2022 to late 2023. Crypto winters are bear markets when crypto prices and private valuations are depressed for extended periods. While episodic, this is the fourth such winter since the inception of the crypto markets. We expect a crypto spring will arrive in 2024, given recent price dynamics among some cryptocurrencies, recent regulatory developments in many key markets, and continued growth in both adoption and in the technology’s utility.

Prior crypto winters have been periods of innovation. Major technical advances and new use cases have followed prior winters. During this winter, progress has been made in core technologies that will make blockchain faster, cheaper, and more capital efficient. As a result, the prices of a few larger cryptocurrencies have performed well in 2023.

A hurdle for cryptocurrencies has long been its regulatory footing, but many jurisdictions have developed clear regulatory frameworks. These markets include the United Kingdom, European Union, United Arab Emirates, Singapore, Hong Kong, South Korea, Thailand, and Japan. While US regulatory clarity and banking access remains cloudy, the stars are potentially aligning for the first US spot Bitcoin exchange-traded fund to be approved by regulators in 2024.

Cryptocurrency usage has also continued to broaden, which we expect will support a spring transition in 2024. One important area involves US dollar–backed “stablecoins” that allow anyone, anywhere to hold US dollars outside of their national banking system using only their cell phone, regardless of what a government might restrict. In late 2023, stablecoins had an aggregate market value of approximately US$130 billion, up from US$3 billion in 2018. Established companies have noticed the promise of stablecoins, with PayPal launching its own stablecoin in 2023. 2 For investors focused on new markets driven by new technology, 2024 may be a good entry point as the next crypto spring commences.

Australian inflation data are quarterly and as of September 30, 2023. Eurozone inflation data are preliminary as of November 30, 2023. All other inflation data are as of October 31, 2023.

Crypto winters are not universally agreed upon. Logarithmic scale chosen to better display the data from a percent change perspective.

Footnotes

- Under yield curve control, a central bank commits to buy whatever quantity of bonds is necessary to keep yields at their target level. In practice, the BOJ operated YCC with an allowance band on either side of its central yield target.

- In November 2023, PayPal received a subpoena from the US Securities and Exchange Commission requesting documents on its stablecoin.

Sean Duffin - Sean Duffin is a Senior Investment Director for the Capital Markets Research Team at Cambridge Associates.

Joseph Marenda - Joe Marenda is the Head of Hedge Fund Research, Head of Digital Assets Investing, and a Partner at Cambridge Associates.

Thomas O’Mahony, CFA - Tom O’Mahony is a Senior Investment Director at Cambridge Associates.

About Cambridge Associates

Cambridge Associates is a global investment firm with 50+ years of institutional investing experience. The firm aims to help pension plans, endowments & foundations, healthcare systems, and private clients achieve their investment goals and maximize their impact on the world. Cambridge Associates delivers a range of services, including outsourced CIO, non-discretionary portfolio management, staff extension and alternative asset class mandates. Contact us today.